How “Clean” Is Nuclear Energy?

Before we get into today’s AMA, we want to acknowledge how incredibly special this weekend is in the U.S…...

This is an extremely leveraged play on the AI data center boom… Any company growing this quickly and using this much debt can only survive in an environment expanding as quickly as the AI infrastructure buildout is.

Founded by three commodity traders in 2017, Atlantic Crypto was early in the industry to attempt to build a company around cryptocurrency mining.

It didn’t focus on mining Bitcoin, which required discrete application-specific integrated circuits (ASICs).

Those are semiconductors designed and optimized for mining Bitcoin and were, at the time, very difficult to acquire. Supply couldn’t keep up with demand.

The team at Atlantic Crypto focused instead on using more widely available GPUs to mine cryptocurrencies other than Bitcoin. So much so that it became a major customer of NVIDIA. Atlantic Crypto focused primarily on mining Ethereum, which was experiencing exponential growth due to the broad utility provided by its smart contract technology.

It was an incredible time in the digital assets industry. That surge in 2017 and 2018 felt unbelievable at the time. Cryptocurrencies were soaring. Opportunity was everywhere.

And then it crashed.

Chart of Ethereum |Source: Messari

By the second half of 2018, Ethereum had given back almost all its gains falling more than 90% from its January 2018 highs.

In hindsight, that rise and fall was nothing. Just a blip on the road to far greater heights in cryptocurrencies in 2021 and early 2022. But it was enough to shake up Atlantic Crypto.

The team decided to pivot to using its GPUs in a different way. Instead of focusing so heavily on Ethereum mining, it shifted focus to renting out its GPUs for cloud-based services, primarily for companies that required GPU-intensive computations like high-resolution video processing and early forms of artificial intelligence (AI).

It even changed its name. In 2019, Atlantic Crypto became CoreWeave.

And while CoreWeave continued to generate some revenue from Ethereum mining, by 2021, it had largely completed the shift towards focusing on non-crypto-related GPU-intensive workloads.

This set the company up well as a cloud services provider for what was coming – namely, generative AI and the training of new AI models.

As CoreWeave had been a major buyer of NVIDIA GPUs since its founding, it had strong access to NVIDIA’s high-demand GPUs. And once OpenAI launched its first commercial version of ChatGPT in November 2022, demand for GPU-based cloud services went through the roof.

CoreWeave was in an enviable position…

It discontinued the use of its GPUs for Ethereum mining earlier that year and went all in on artificial intelligence. That switch generated a far better return than mining cryptocurrencies. And because of its strong ties to NVIDIA, NVIDIA stepped up to invest $100 million into CoreWeave, as a private company, in May 2023 during its Series B funding round.

This was a big deal. NVIDIA is very selective in where it writes large checks. For comparison, before the Series B round, CoreWeave had only raised around $68 million. Its Series B round was a $421 million raise, $100 million of which was from NVIDIA.

With that investment, NVIDIA legitimized CoreWeave as a major player in AI-specific, GPU-based cloud services. Its involvement attracted additional capital, primarily from hedge fund Magnetar Capital.

And what did CoreWeave do with the capital it received from NVIDIA and Magnetar?

It bought more NVIDIA GPUs of course.

This is where things get interesting. Red flags started popping up.

NVIDIA invests a lot of money in a private company that then turns around and buys NVIDIA products. If that wasn’t bad enough, around the time of that investment, NVIDIA also agreed to a four-year deal to rent $1.3 billion of GPU-based cloud services from CoreWeave.

Why in the heck would a semiconductor company spend $1.3 billion renting its own GPUs from another company? After all, NVIDIA just designs and sells its GPUs, right?

Wrong.

And yet, the media and the press missed it completely. They were screaming about red flags everywhere. The words “circular transactions”, “fraud,” and “scam” were being thrown around about CoreWeave. Some comments even suggested that the company wasn’t even real.

It was crazy. With only a small amount of effort, journalists could have confirmed that the business was legitimate. And while NVIDIA was its second largest cloud services customer in 2023 due to the $1.3 billion deal mentioned above, CoreWeave’s largest customer was – and still is – none other than Microsoft.

That’s not just any name, but one of the biggest names in high tech and cloud services. Even with its own Azure cloud services division, Microsoft still needed additional computational resources to handle extra GPU workloads.

And as for NVIDIA, most people don’t know that its software and AI models are just as strategic and important to its business as its GPUs are.

One of the smartest strategies employed by NVIDIA is to develop reference AI models for robotics, autonomous driving, digital twinning, and simulation that it provides to its customers. This removes obstacles to the adoption of NVIDIA hardware and accelerates the development of applications that run on NVIDIA GPUs.

NVIDIA doesn’t specialize in spinning up GPU-based data centers, so renting GPU capacity from CoreWeave made sense.

Now, I’ll be the first to admit that the combination of commodity traders, cryptocurrency mining, fast-moving hedge funds, pivots to AI, and “circular transactions” have the makings of a horrible ending. This is a very odd mix for a cloud service provider.

But CoreWeave (CRWV) and its IPO are real and being priced today. The company is expected to start trading tomorrow (Friday) on the NASDAQ.

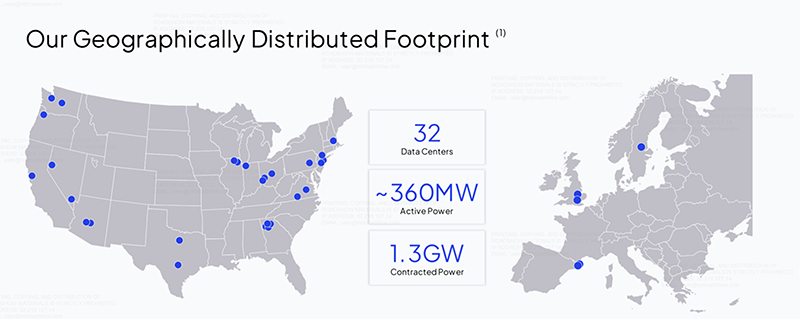

CoreWeave’s Data Center Footprint | Source: CoreWeave

In an incredibly short period, CoreWeave has spun up 32 data centers, primarily in the U.S., with a few in Europe, and contracted 1.3 gigawatts of power. After all, if you don’t have the juice, you can’t run your data centers.

Power and GPUs are the two most critical factors in AI, and that’s what CoreWeave solved for.

What is concerning – and what CoreWeave is “guilty” of – is leverage. The company has leaned in and accelerated its data center footprint and GPU acquisition with $8 billion in debt.

$8 billion in debt based on $1.92 billion in revenue in 2024, and a forecasted $4.6 billion in 2025. Worse yet, CoreWeave’s free cash flow was a negative $5.95 billion last year and could burn through $15 billion this year.

And this is where the risk is with CoreWeave. Too much leverage.

If the AI boom were to slow down, or GPU-based cloud services suddenly fell from such high demand, CoreWeave would find itself in a very sticky situation – unable to raise additional capital.

But for Bleeding Edge subscribers, we know that demand for GPUs and AI factory buildouts has continued to increase. All available capacity continues to get taken up, and anyone with access to NVIDIA GPUs has no problem monetizing them.

And NVIDIA has already signaled it’s not walking away. In fact, it has stepped up and is buying $250 million worth of CoreWeave’s IPO. To keep things in perspective, we’ve estimated the IPO valuation of CoreWeave around $23 billion.

It’s worth remembering that NVIDIA first invested its $100 million at a $2.1 billion valuation. That investment will be up more than 10X based on a $23 billion valuation. NVIDIA will likely be up about $1 billion in profit on that original investment post-IPO. It is using a faction of that to invest more in CoreWeave – one of those “circular transactions.”

NVIDIA benefits from having smaller cloud service providers in the market. If the entire market were controlled by Alphabet, Microsoft, Meta, xAI, and Oracle, all hyperscalers, it would have weaker pricing power. And as some of the hyperscalers design their own AI-specific semiconductors, NVIDIA is smart to help develop the next tier of gigawatt-plus AI factories.

CoreWeave had intended to raise $2.7 billion at roughly a $35 billion valuation earlier this week. As of this afternoon, aspirations appear to have been lowered and what we’ve heard is a raise of $1.5 billion at $40 a share at a $23 billion valuation fully diluted.

Is that good or bad?

Well, it’s significantly lower than what the team had been working towards. The target pricing range was between $47 and $55 a share, and now CoreWeave is looking at around $40 a share and raising significantly less capital.

This is indicative of the current volatility and tariff-related concerns in the market. If there’s one thing I don’t understand about this deal, it’s why the CoreWeave team didn’t simply delay the IPO for a month or two when conditions will most certainly be better.

But I’m pretty sure we know why it decided to push on… it needs the money.

CoreWeave’s burn rate is high and it needs capital to fuel its growth. And even post-IPO, it will have to raise additional capital later this year.

Despite OpenAI agreeing to a five-year, $11.9 billion deal with CoreWeave, that money won’t be paid upfront. It will need a lot of cash, no matter how I look at CoreWeave’s business model.

We’ve calculated that CoreWeave’s valuation at $40 a share will be about five times the forecasted 2025 sales of around $4.6 billion. That’s not unreasonable at all for a company growing like CoreWeave.

But that doesn’t account for the risk associated with how much additional capital it will have to raise, either through debt or new stock issuance which will dilute the share price.

CoreWeave is a very leveraged, literally, play on the AI data center boom. Any company growing this quickly and using this much debt can only survive in an environment expanding as quickly as the AI infrastructure buildout is.

I’m confident this trend will continue for several years into the future. CoreWeave’s share price and valuation, however, will be more a reflection of its capital structure in the short-term rather than the AI boom that is well underway.

It’s a big IPO nonetheless, something the industry has been waiting for. A flood of IPOs will begin soon as interest rates decline and economic growth kicks in.

Someone has to go first.

Jeff

Read the latest insights from the world of high technology.

Before we get into today’s AMA, we want to acknowledge how incredibly special this weekend is in the U.S…...

“Restoring supersonic flight over land isn’t just about speed. It’s about unleashing American innovation and ushering in a Golden...

This will be looked back on as the most significant breakthrough in medical imaging in more than 50 years.