The Beginning of an Entirely New Industry

OWS is an entirely new industry that will experience explosive growth in the next few years, and one that...

It’s easy to be negative about things we don’t completely understand.

Managing Editor’s Note: Don’t forget to add your name to Jeff’s guest list with one click for Thursday, November 20, at 8 p.m. ET.

He’ll reveal the details on a little-known pattern in the crypto market he calls “60-day profit windows”… as well as the neural network he developed to help spot them and identify the digital assets most impacted.

If you’re searching for a strategy to take advantage of volatility in the crypto market, just go here to automatically sign up to join Jeff this Thursday at 8 p.m. ET.

Michael Burry became famous for a single, and seemingly impossible, trade…

Betting against the U.S. housing market.

His investment thesis was simple.

Mortgage lending practices were out of control, credit quality was much lower than what was commonly believed, and the massive amounts of subprime loans would see their interest rates reset in 2007, which would bring down the house of cards.

Burry was painfully early.

He began establishing his short positions on the U.S. housing markets using credit default swaps (CDS) against subprime mortgage bonds more than two years before the crash.

Every month, his hedge fund, Scion Asset Management, was paying millions of dollars in premiums to maintain those positions.

The situation was untenable for many of his limited partners in the fund.

It got so bad that Burry did something highly unconventional: He restricted the ability of the limited partners to withdraw their funds.

Threats of lawsuits against Burry and his fund mounted. It was a disaster.

If he returned the funds to his limited partners, he would have been forced to close his positions at a massive loss. His fund would have collapsed.

Steadfast in his belief of what would happen with subprime mortgage bonds, he risked everything to see out his trade.

In the end, he was right, and he made the fund about $800 million in profit – $100 million of which was his.

His call on the mortgage market is now legendary. It has been memorialized in the book The Big Short (a must-read) and the movie under the same name (entertaining, but not as good as the book).

Which is why his most recent trades have been taken so seriously by those in the financial media.

In the last couple of weeks, the financial media was spun up into a tizzy over Burry’s posts on X…

He was suggesting that we are in an AI bubble… and a crash is imminent.

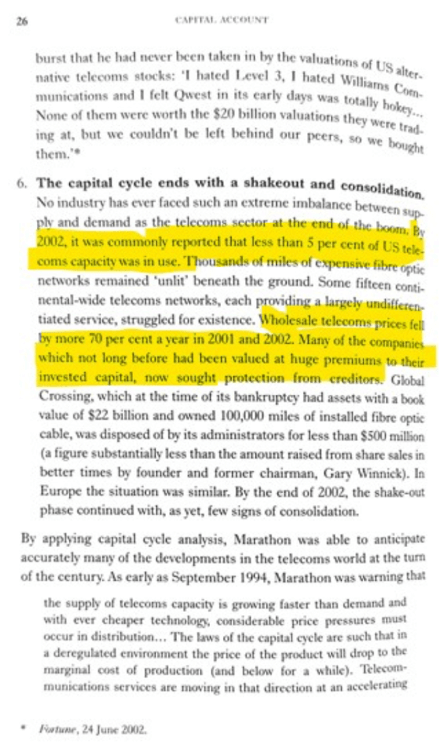

On November 3, it started with a post referencing the utilization of telecommunications networks immediately after the dot-com bubble…

By 2002, it was commonly reported that less than 5 per cent of U.S. telecoms capacity was in use.

Michael Burry on X, November 3, 2025 | Source: X @michaeljburry

That was followed by the economic implications of having a glut of capacity over the newly built telecoms networks at the time…

Wholesale telecoms prices fell by more than 70 per cent a year in 2001 and 2002. Many of the companies which not long before had been valued at huge premiums to their invested capital, now sought protection from creditors.

Burry’s mission was clear: To draw an analogy between the AI-related capital expenditures taking place right now to the dot-com bubble and bust.

That was just the first salvo.

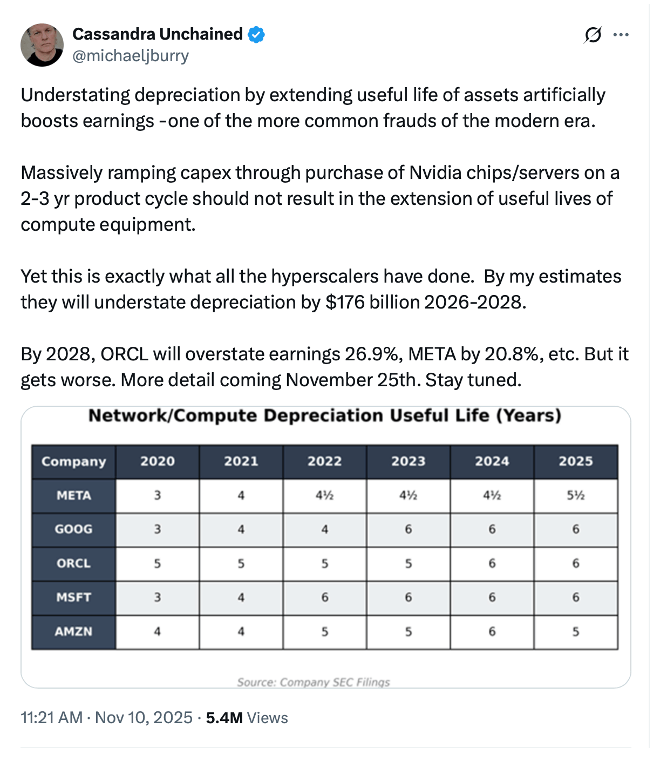

On November 10, Burry got to his main investment thesis for being short AI…

The key point of his investment thesis centers around how hyperscalers account for depreciation, which is usually spread over five or six years. (Depreciation is the accounting process of gradually writing off the cost of assets like GPUs, switches, servers, and data center infrastructure over time.)

As a reminder, a hyperscaler is a large-scale cloud computing provider or data center operator that delivers massive amounts of computing power, storage, and infrastructure services on an elastic, scalable basis to handle enormous workloads for organizations and users.

Common examples of hyperscalers include Amazon Web Services (AWS), Microsoft Azure, and Google Cloud.

Burry claims that GPUs are only used for two or three years, as hyperscalers upgrade quickly to the latest models from NVIDIA.

Doing so, in Burry’s eyes, inflates the earnings of related AI companies because big tech companies write off depreciation costs over five or six years, instead of two or three.

Is Burry right or wrong? Are AI earnings drastically overstated? How can we make sense of it all?

And is this really just like the dot-com boom or the subprime mortgage crisis?

In short, no, not at all.

And the first thing for us to understand is that Burry is talking his own book.

Burry hadn’t posted on X since April 2023, more than two and a half years ago.

Even more importantly, he built large short positions in NVIDIA (NVDA) and Palantir (PLTR) in advance of his series of posts this month.

He purchased:

This was revealed in a recent SEC filing for his Scion Asset Management fund, which you can see here.

This is classic Wall Street antics.

Quietly build your large position, then go public in an effort to influence the market in the desired direction… and hopefully close out the position at a large profit at others’ expense.

This is why it is always important to understand whether or not any talking head has a financial incentive related to the subject matter on which they are speaking (or posting).

This is precisely why we have a clear no conflict of interest policy at Brownstone Research. I never own stock in something that I recommend and never recommend anything that I have a financial position in. It’s the only way to ensure objectivity.

Burry’s positions will profit if he is successful in stoking fear in the markets about an AI bubble, which is exactly what he is trying to do.

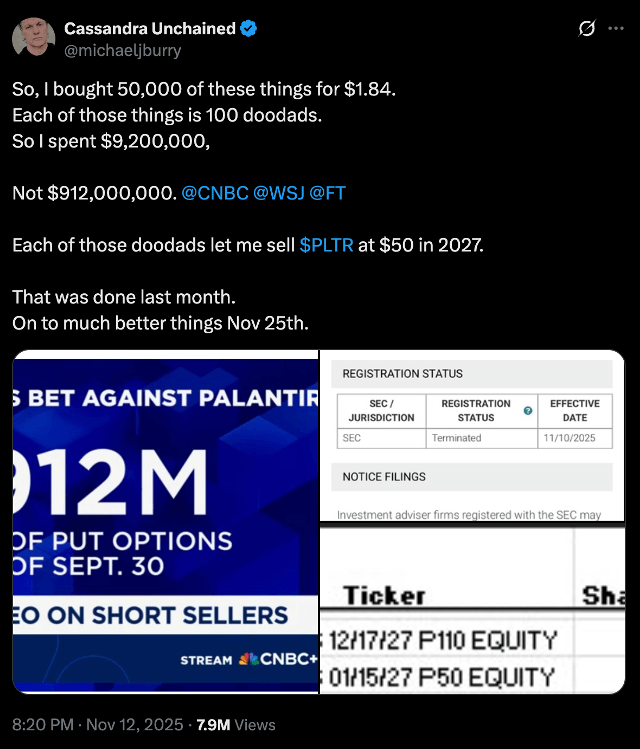

Financial media outlets quickly implied that Burry had taken out a $912 million short position on Palantir and a $187 million short position on NVIDIA.

But even Burry had to correct CNBC’s math.

He spent $9,200,000 (a little over $9 million, not $912 million) on puts on Palantir at a strike price of $50 in 2027.

That suggests that he believes that Palantir’s stock will collapse by more than 70% by 2027.

What do I think?

Here’s where Burry’s underlying assumptions about the AI infrastructure capital expenditure (CapEx) spend are fundamentally wrong:

Burry is conflating technology issues.

It is true that when training a large frontier AI model, you would typically use a version of leading-edge GPUs for just a couple of years, but that doesn’t mean you stop using them for other purposes.

Training is extremely compute-intensive, which is why it makes sense to train on the most advanced GPUs available at any given time.

But once that switch is made, older GPUs are simply used for inference (i.e., the running of AI applications). GPUs will continue to be used as long as the cost of maintaining them and powering them per unit of compute economically makes sense.

And yes, that timeframe tends to be five or six years in general, hence the current five- or six-year depreciation cycle.

When he refers to earnings, he is referring to earnings per share and income, which are accounting numbers. No serious analyst relies on earnings numbers because they can be manipulated so easily.

What is important is EBITDA, which is before interest, taxes, depreciation, and amortization. And also, free cash flow is king. It tells us exactly how much cash a business has in hand to fund the business and invest, as well as to service any debt.

He didn’t get it all wrong, though.

Here’s where Burry is right:

Even if we look forward to 2027, which is when Burry’s Palantir puts expire, Palantir’s forward-valuation multiples are 46 EV/Sales and 91 EV/EBITDA.

These valuations are ridiculous, even for a company with 83% gross margins and growing sales at 53% year on year. It wouldn’t take much for Palantir to collapse back to more reasonable levels.

But when it comes to Burry’s NVIDIA position, he is going to lose his shorts – literally and figuratively.

Unlike Palantir, NVIDIA is trading at a 21 EV/Sales and a 34 EV/EBITDA on 70%+ gross margins and revenue growth of 59% year-over-year.

And when we look at forward-valuation multiples, NVIDIA is trading at an EV/Sales of 12.5 based on fiscal year 2028 (ending January 31, 2028 – basically calendar year 2027) and 18.5 EV/EBITDA.

This is more than reasonable for NVIDIA’s current free cash flow generation and revenue growth.

About a decade ago, I predicted that Apple (AAPL) would become the world’s first $1 trillion company. That happened in 2018.

NVIDIA will become the world’s first $10 trillion company, and AMD will become a trillion-dollar company.

This will happen within the next three years.

It’s easy to be negative about things we don’t completely understand.

Understanding semiconductor design and utilization, data center infrastructure design and utilization, training vs. inference, and timing to reach AGI are a whole lot different than understanding the risk associated with no income, no job mortgage loans, and giving AAA ratings to a bunch of subprime loans.

We’ll see who’s right: Brown or Burry.

While the financial media doesn’t talk about it, Burry has a history of bad calls:

You know where I stand.

And I’m not going to lose my shorts, nor will my subscribers.

We’ll be buying a few new pairs, in fact.

Jeff

P.S. Who’s right, Brown or Burry? Let us know what you think right here, or you can always reach us through our feedback file at brownstonefeedback@brownstoneresearch.com…

Read the latest insights from the world of high technology.

OWS is an entirely new industry that will experience explosive growth in the next few years, and one that...

One of the most exciting topics of the Fusion Industry Association’s Annual Policy Conference is the proximity of not...

Someone with no medical training whatsoever leveraged AI to devise a custom cancer vaccine entirely on their own, in...

Thanks for signing up for The Bleeding Edge — we’re glad you’re here!

Want updates sent straight to your phone too? Sign up for SMS alerts to get the latest delivered via text.

Brownstone Research: By submitting your phone number, you agree to our SMS Terms & Conditions, Terms of Use, & Privacy Policy, and give express written consent to receive marketing text messages from BSR. Messages are recurring & frequency may vary. Reply STOP to 94703 to opt out. Reply HELP to 94703 for info. Consent is not a condition of purchase. Message and data rates may apply. For additional information, you may contact Customer Service at 888-512-0726 or smssupport@brownstoneresearch.com.