Leveraging AI for Personalized Cancer Therapies

Someone with no medical training whatsoever leveraged AI to devise a custom cancer vaccine entirely on their own, in...

Understanding the current dynamic helps self-directed investors make better decisions…

Jeff’s Note: Back in 2017, I invested in Coinbase. It went on to have one of the biggest IPOs ever – $112 billion.

But when I spotted it, it was worth a tiny fraction of that.

What drew me to it? I saw that Wall Street was starting to get into crypto. And after analyzing Coinbase, I knew it was the perfect investment. Since then, my stake has risen as much as 74x. That turns $10,000 into nearly $750,000.

Now I believe Wall Street could send a new group of coins soaring. You see, a new bill is working its way through Congress. It’s expected to provide the regulatory framework Wall Street needs to plow trillions into a corner of the crypto market.

When that happens, I believe it could trigger massive gains… just like it did back in 2017. As long as you act quickly, you could get ahead of it.

I explain everything in my recent briefing – watch here now.

Today, we’ll step away from artificial intelligence, robotics, and all the incredible happenings in high tech to discuss an important – and very much related – topic.

Interest rates.

Interest rates may seem dull and boring, but stick with me… Their moves impact our investments. So understanding the current dynamic helps self-directed investors make better decisions regarding portfolio construction.

Interest rates can be thought of as the price of money. It’s how much people, businesses, and governments must pay to borrow money.

This makes interest rates the most important price in the world. Higher interest rates mean borrowers will have to pay more for debt. And for the U.S. government, which projects that it will pay $952 billion in interest this fiscal year, interest rates matter.

That is why both President Trump and Treasury Secretary Scott Bessent are pressuring the Federal Reserve Chairman Jerome Powell to get the Fed to cut interest rates dramatically.

Should Powell cut rates or not? And is he stupid, like Trump says?

Of course, the media oversimplifies the narrative. But there may be more to this story than meets the eye.

I think we’ll find there’s a far more nuanced dynamic here than the financial media lets on.

But before we dive straight into the scuffle, let’s cover the fundamentals…

How might Jerome Powell’s actions regarding interest rates have ripple effects throughout the U.S. economy?

There are several key interest rate benchmarks that influence rates throughout the U.S. economy. They are:

The Fed Funds Rate is the rate at which U.S. banks lend reserve balances to each other overnight. Here’s how it works at a high level…

At the close of business on any given day, some banks find themselves short on their reserve requirements, while others have a surplus. Banks with a deficit must borrow reserves from banks with a surplus. The Fed Funds Rate is the interest rate they pay on those loans.

When we talk about the Fed hiking or cutting rates, we’re talking about the Fed Funds Rate. That’s the only interest rate benchmark fully within the Fed’s control.

However, the Fed Funds Rate directly influences other short-term rates throughout the economy. They are:

If we look at this list, short-term Treasury rates are probably the most important in the current climate. The higher those rates are, the higher the U.S. government’s debt service cost will be on new short-term debt issued.

This is a big reason why President Trump and Treasury Secretary Bessent are pounding the table for the Fed to cut rates.

With $9.2 trillion of debt coming due in 2025, it is in the nation’s best interest to refinance this debt at much lower rates.

We believe President Trump will get his way and the Fed will begin cutting its benchmark rate in September. This will push down short-term interest for all the listed rates.

For our purposes, it’s important to understand what happens when interest rates fall.

When rates fall, people can comfortably borrow more to fund large purchases or vacations. Businesses have more expansion plans that meet their internal return on investment requirements. And the government doesn’t have to tighten its belt.

All this new borrowing pulls economic activity forward to the present… and will likely lead to a surge in profits for many businesses.

That will lead to higher stock prices. And institutional investors will magnify the move. They used to park their capital in money market funds that yielded 4-5%, but now they will need to look for other sources to chase yield. This will inevitably pull them into the stock market.

This is why the Fed’s decisions matter to monetary policy.

But it’s important for investors to understand that the Fed Funds Rate only influences short-term interest rates in the economy.

Long-term interest rates (e.g., those on 10-year or 30-year Treasury notes) are historically driven by market dynamics such as supply and demand, investor expectations, and economic conditions, rather than direct Fed control (barring extreme Fed intervention, like what we saw with quantitative easing post-2008 and during COVID-19).

Long-term rates can affect the broader economy, including borrowing costs for mortgages, corporate bonds, and long-term government debt…

And believe it or not, after over 17 years, the market – not the Fed’s influence – is back in control of long-term rates.

But before I show you how we know this, we must understand what happened back in 2022…

There are two other major interest benchmarks in the U.S.: The Secured Overnight Financing Rate (SOFR) and the 10-Year Treasury.

SOFR is the primary benchmark for trillions of dollars in corporate loans, adjustable-rate mortgages, floating-rate loans, interest rate swaps, futures contracts, options, derivatives, and other structured financial products. It reflects pure borrowing costs without bank credit risk, since it’s tied to overnight lending.

It wasn’t always the primary benchmark, and that’s an important nuance I’ll return to momentarily.

Today, SOFR is a critical benchmark for large corporate and institutional borrowing and hedging activity, and that extends into longer-term financing. Often, borrowing and hedging activity occurs when a company is undertaking larger-scale projects.

I’ll explain…

Borrowing: When a company undertakes a large-scale project—such as building new infrastructure, expanding operations, or acquiring assets—it often needs to borrow substantial sums of money. These loans frequently have variable interest rates linked to a benchmark like SOFR. For example, a company might issue floating-rate bonds or secure revolving credit facilities where the interest payments adjust based on SOFR.

Hedging: To protect themselves from the risk of rising interest rates (which would increase their borrowing costs), companies use interest rate derivatives such as SOFR interest rate swaps. In a typical swap, the company agrees to exchange its variable (SOFR-based) interest payments for fixed payments, stabilizing its future cash flows and making project budgeting more predictable.

These borrowing and hedging strategies are fundamental for large-scale corporate finance and are especially common during major capital-intensive projects.

That makes SOFR arguably more important than the Fed Funds Rate when it comes to spurring larger projects that could generate outsized economic growth.

And here’s a key feature to know about it…

SOFR is based on actual transactions in the Treasury repo market – the financial market where participants engage in repurchase agreements (repos), typically overnight, using U.S. Treasury securities as collateral. The rate is derived from market activity.

The Treasury repo market is similar to the Fed’s overnight window for banks, except it’s open to many other financial institutions like securities dealers, investment firms, asset managers, money market funds, mutual funds, hedge funds, pension funds, sovereign wealth funds, insurance companies, and other institutional investors.

When one of these institutions needs short-term funding, it can go into the repo market to essentially borrow money from another institution that’s willing to lend. The interest rate for that loan is determined by the two parties involved.

Just to be clear, these aren’t standard loans.

In a repo transaction, the borrowing institution sells U.S. Treasury securities to the lending institution and agrees to buy them back on a specified future date at a higher price. That price difference represents the interest on the loan.

Again, the key here is that these are market-based transactions in which self-interested parties determine the interest rate that they are willing to accept. The aggregation of all the daily transactions in the repo market is what establishes the SOFR rate.

The takeaway here is that SOFR cannot be “set,” nor is it tied to the Fed Funds Rate. SOFR is determined by market forces.

And here’s where the story gets interesting…

SOFR has only been the primary benchmark for short-term borrowing and lending in the U.S. financial system for the last three years.

In 2022, something changed.

Before 2022, the London Interbank Offered Rate (LIBOR) was our benchmark. If it sounds odd that we were using a benchmark based in London, that’s because it was.

I would argue that SOFR fully replacing LIBOR in 2022 was a revolutionary act. It liberated U.S. interest rates from global manipulation. Here’s why…

LIBOR was calculated based on daily estimates submitted by a panel of 16 of the world’s largest banks. That panel consisted of 11 banks headquartered in Europe… three American banks… one Japanese bank… and one Canadian bank.

However you slice it, European interests dominated the benchmark.

When LIBOR was the dominant benchmark, that banking consortium could and did manipulate it at will. We learned this when the “LIBOR scandal” broke in 2012.

This is why the world came to believe that the Fed completely controls interest rates throughout the economy. For the better part of the last two decades, interest rates were heavily manipulated.

If we remember, former Fed Chair Ben Bernanke initiated the era of globally coordinated monetary policy in 2008 in response to the financial crisis. Bernanke announced that the Fed would collaborate with other central banks with the stated goal of pushing interest rates to zero and keeping them there.

During that era, the LIBOR consortium could manipulate LIBOR lower whenever the Fed cut interest rates. That made it look like the Fed had the power to move all interest rates down at will… but it was really a coordinated effort to snuff out market forces.

And that brings us to the 10-Year Treasury…

The yield on the 10-year Treasury note is a critical benchmark, as well. It is considered the global “risk-free” rate for longer-term investments.

The U.S. Treasury sells 10-year Treasury notes to raise money to finance government spending. Investors pay a lump sum payment upfront to buy it, and then the U.S. Treasury agrees to pay the investor coupon payments at a specified interest rate for 10 years.

Obviously, the U.S. Treasury wants to sell these securities at the lowest rate possible, whereas investors want to get the highest rate possible. They have to meet in the middle somewhere to get the deal done.

For this reason, the 10-year Treasury rate is seen as a gauge of economic growth and inflation expectations in the United States. If investors expect high inflation in the U.S., they require higher interest rates to mitigate their risk.

That makes the 10-year Treasury a benchmark for corporate bond rates, municipal bond rates, and mortgage rates. Specifically, the 30-year fixed mortgage rate in the U.S. closely tracks the 10-year Treasury rate.

So the 10-year Treasury rate is also arguably more important than the Fed Funds Rate when it comes to corporate and municipal credit, as well as the U.S. housing market.

During the era of global central bank coordination, the 10-year Treasury rate fell alongside the other primary benchmarks. But again, that was due to intense Fed intervention and manipulation.

Remember Bernanke’s quantitative easing (QE) programs that his successor, Janet Yellen, continued? They printed trillions of dollars from nothing to buy the 10-year and other long-dated Treasurys specifically to manipulate long-term interest rates lower.

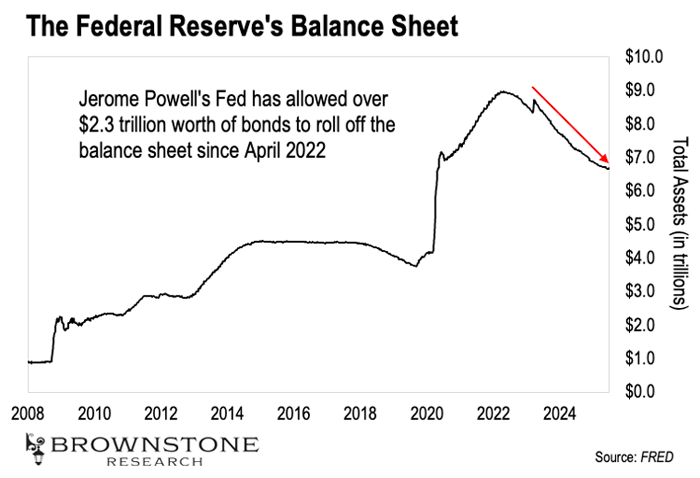

Powell’s Fed initially ended QE in 2018, restarted it in late 2019 and throughout the Covid mania, and then ended it again in 2022. The Fed has engaged in quantitative tightening (QT) since then to allow interest rates to normalize. This chart tells that story:

This is a chart showing the total dollar amount of assets held on the Fed’s balance sheet. When we see the line going up, that’s the Fed printing money to buy U.S. Treasurys. It also bought mortgage-backed securities in the wake of the 2008 crisis.

The act of printing money to buy Treasurys pushed long-term interest rates down. We can see that this was going on for most of the 2008-2022 time period.

But the line’s been going down since 2022. That’s quantitative tightening. It shows that the Fed stopped buying Treasurys on net… which allowed interest rates to normalize.

The reality is that the 10-year Treasury rate is largely determined by self-interested market actors in the absence of QE. If the rate is too low compared to economic and inflation expectations, investors aren’t going to buy the securities… so the U.S. Treasury has to offer attractive rates given the state of the market.

So even if Powell and the rest of the Federal Reserve members lower the FOMC rate, it may not impact longer-term yields. In fact, it could even spur inflation fears, which would send long-term rates higher.

The only way the Fed can directly impact long-term interest rates is to increase its balance sheet again – which is not being discussed. Restarting QE would risk spooking the market. It would signal fiscal weakness that would undermine the dollar and drive inflation higher. That would blunt the program’s ability to push long-term rates down.

It all comes down to this…

We’re back to an age where long-term interest rates are largely set by market forces once again. The bond vigilantes – a term coined to describe how the bond market can force fiscal responsibilities – are shying away from long-term bonds. What’s more important, in their opinion, is to have responsible fiscal policy – not $1 trillion+ deficits in peacetime.

And that’s not theoretical – we’ve already seen it.

Powell cut the Fed Funds Rate by one percent in the fourth quarter of last year… but long-term rates didn’t go down. To the contrary, they went up. The 10-year Treasury rate steadily moved one percent higher after the Fed’s cuts.

The key takeaway for us as self-directed investors is this: The interest rate market is far more nuanced than the financial media implies. They still see the world through the lens of the previous era from 2008 to 2022, which was highly manipulated. But that era is over.

We’ll want to make the distinction between short-term and long-term interest rates.

And we need to watch how the 10-year market responds to the coming short-term interest rate cuts. If the 10-year yield goes down along with short-term yields, it’s risk on. And we will see a huge rally in both bonds and equities… and every other risk asset.

But if the 10-year yield continues to rise, even as short-term yields lower, that will be a warning sign. And we will need a more cautious approach.

This is how we can gauge the impact on our portfolio and the financial decisions we make going forward.

– Joe Withrow

P.S. If the Fed’s actions matter less today for long-term interest rates, why does Trump care so much about what Powell is doing? Tomorrow, we’ll look at the Trump vs. Powell faceoff… and how there may be more to this story than meets the eye.

Read the latest insights from the world of high technology.

Someone with no medical training whatsoever leveraged AI to devise a custom cancer vaccine entirely on their own, in...

If NVIDIA hits the scale Jensen Huang is signaling, we’re no longer talking about incremental growth in data center...

When Elon Musk stated he wanted to build his own semiconductor manufacturing plant, many assumed he was just bluffing…

Thanks for signing up for The Bleeding Edge — we’re glad you’re here!

Want updates sent straight to your phone too? Sign up for SMS alerts to get the latest delivered via text.

Brownstone Research: By submitting your phone number, you agree to our SMS Terms & Conditions, Terms of Use, & Privacy Policy, and give express written consent to receive marketing text messages from BSR. Messages are recurring & frequency may vary. Reply STOP to 94703 to opt out. Reply HELP to 94703 for info. Consent is not a condition of purchase. Message and data rates may apply. For additional information, you may contact Customer Service at 888-512-0726 or smssupport@brownstoneresearch.com.