Luddites vs. Effective Acceleration

Warning for anyone who has anxiety over the impact of AI on work, this is bound to cause convulsions....

Both thought pieces considered impacts in isolation without considering policy responses to these technological changes…

On February 24, Citadel – one of the largest and most successful hedge funds – put out its own thought piece as a retort to the Citrini Research Substack post we covered in yesterday’s Bleeding issue – Luddites vs. Effective Acceleration.

We left off discussing Citrini Research’s motivations for publishing the piece, which gave a somewhat dismal outlook on artificial intelligence’s impact on the economy and labor market. And now, we turn to Citadel’s response.

Now, we have to understand that Citadel was certainly talking its own book.

Its post was aligned with its own long/short holdings, which is why it rushed to put out a counter-piece to Citrini.

But like Citrini, Citadel made some good points as well.

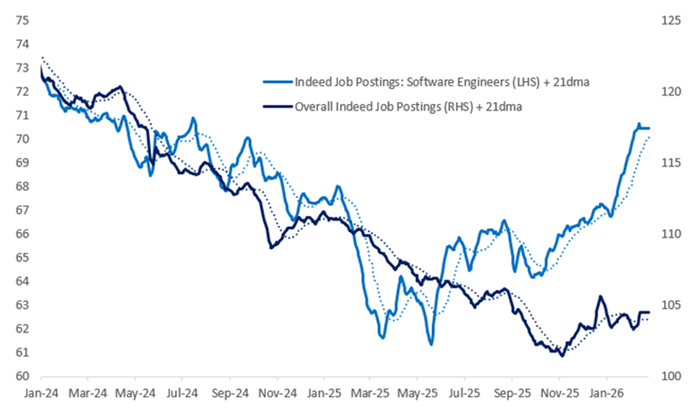

One notable point was that the number of postings for software engineers has significantly increased over the last six months, the opposite of what we might expect from the employment of AI and the expectation of layoffs of software engineers.

Job Postings for Software Engineers

Source: Citadel

Citadel went on to suggest that large-scale disruption of white-collar workers would require orders of magnitude more computational infrastructure than what is currently available today.

It went further by suggesting that as demand for more computational infrastructure increases, it will push up the marginal cost of computational infrastructure.

And by extension, if marginal costs increase above the marginal cost of human labor, then the disruption to white-collar labor won’t be as fast as Citrini theorized in its fictional piece.

But Citadel missed the mark completely on a fundamental truth of semiconductor technology.

Each successive generation of semiconductor technology, which tends to release new semiconductor platforms annually, delivers material improvements in terms of performance per unit of compute. This has also resulted in an exponential decline in the cost per unit of compute.

That means we are unlikely to reach this threshold where AI costs are above human costs.

Where Citadel got it right is where it pointed out that “productivity shocks are positive supply shocks.” Exponentially declining cost per unit of compute is a force multiplier for human adoption and human productivity. It enables us to accomplish more. And there is no shortage of goods and services to improve upon and invent.

This is a critically important point. Large productivity gains result in lower marginal costs, increase total production of goods and services, and expand discretionary income.

The productivity gains from artificial general intelligence will be so significant that they will make previously unavailable products and services available to a much larger percentage of the population.

These advancements are deflationary and will improve the quality of life across the board.

This has been proven time and again through history with inventions like the textile loom, electricity, the steam engine, the internal combustion engine, internet infrastructure, smartphones, etc.

These technological advances, these productivity improvement enablers, have empowered the economy to grow at higher rates and enabled the human workforce to accomplish more.

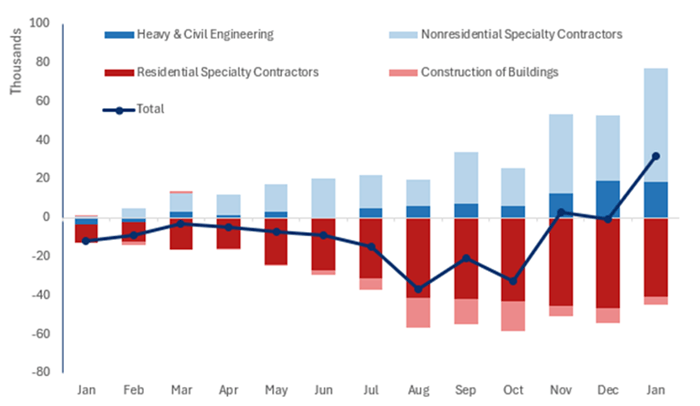

Another important point that Citadel made can be seen in the chart below. It shows the shift that has taken place in the construction labor market.

Data Center Construction Shift (U.S. Payroll)

Source: Citadel

The above chart shows us how data center construction jobs have now more than offset declines in construction in residential and commercial real estate.

The volume of technology-driven jobs being created exceeds the declines in more traditional labor markets. This is a major trend we can expect to continue across most sectors.

At an even higher level, both of these thought pieces considered these impacts in isolation without considering policy responses to these technological changes.

The Federal Reserve, with its pending removal of Powell, will finally be able to take proactive action to address the absence of inflation and the deflationary impact of AI on goods and services by lowering interest rates accordingly.

The cost of automotive loans and home mortgages will decline as a result, increasing worker mobility (workers can now sell their house and finance a new purchase at reasonable rates), as well as increasing discretionary income.

And because AI-related companies are real companies generating revenue and are, in many cases, profitable, there will be continued record levels of investment in both infrastructure and AI companies to employ this incredible technology.

Pro-energy, pro-technology, and pro-business regulations will accelerate growth, creating opportunity everywhere for those willing to take it. With GDP growth above 5% annually, tax revenues will increase. And technology will be used to reduce the size of the U.S. fiscal deficit starting next fiscal year (beginning October 1, 2026).

Programs and incentives will be put in place for re-training of the displaced workforce for those willing to do so, and I expect that some level of basic income program will be put in place for those unable or unwilling to go to work.

In short, there will be incredible opportunities for just about everyone, and this will be especially true for investors. This is not the time to be on the sidelines as an investor.

Just imagine the economic growth with the employment of AGI. Where there is accelerated economic growth, there is accelerated appreciation in asset prices.

It’s also a reminder about the importance of thinking about the motivations for anything we read online or see on TV. If it comes from Wall Street, hedge funds, or others managing capital, my working assumption is always that they are talking their book and trying to profit.

This is precisely why we have no conflicts of interest at Brownstone Research. Our business is 100% subscription based, and we only work for our subscribers.

I am not permitted to invest in something I recommend in my model portfolios, and I cannot recommend something in my model portfolios that I am already invested in. It is critical that my senior analysts and I maintain complete objectivity with no conflicts of interest.

That is our commitment to our subscribers.

So no, the world is not coming to an end, and we’re not all going to be out of jobs. Quite the opposite, and the opportunities to increase our wealth will be everywhere.

We have so much to look forward to,

Jeff

Read the latest insights from the world of high technology.

Warning for anyone who has anxiety over the impact of AI on work, this is bound to cause convulsions....

Last week, Block CEO Jack Dorsey announced that the company would be cutting its organization almost in half…

We can’t provide any personal investment advice, but we can use a question as an example of how to...

Thanks for signing up for The Bleeding Edge — we’re glad you’re here!

Want updates sent straight to your phone too? Sign up for SMS alerts to get the latest delivered via text.

Brownstone Research: By submitting your phone number, you agree to our SMS Terms & Conditions, Terms of Use, & Privacy Policy, and give express written consent to receive marketing text messages from BSR. Messages are recurring & frequency may vary. Reply STOP to 94703 to opt out. Reply HELP to 94703 for info. Consent is not a condition of purchase. Message and data rates may apply. For additional information, you may contact Customer Service at 888-512-0726 or smssupport@brownstoneresearch.com.