NVIDIA’s Blowout Numbers

Even with all of the excitement happening right now with AI, the 2026 hyperscale spending on AI infrastructure still...

Earnings season is in full swing…

Managing Editor’s Note:If you’re struggling with all the ups and downs of the cryptocurrency market this year, you’re not alone.

Digital assets have long been prone to volatility. But there’s a way you can take advantage of these swings before they strike…

Jeff’s getting into the details next Thursday, November 20, at 8 p.m. ET, of his strategy that lets you profit from dramatic shifts in digital assets… often in 60 days or less.

You can go here to sign up to join him next week at his 60-Day Crypto Fortunes strategy session.

Earnings season is the truth serum of Wall Street.

It cuts through speculation, exposes hype, and shows us which companies are thriving… and which are falling behind.

With Washington’s shutdown freezing many government data releases, corporate earnings have become an even more important signal of what’s really happening in the economy. Plus, when doing fundamental research, we like to get as close to the source as possible. One of the best ways to do that is by tuning into company earnings calls.

On these calls, executives reveal what they’re seeing in customer demand, where the supply chains are tight, and how they’re planning for the next quarter and year. Listening closely is like sitting in on a private boardroom briefing with some of the most influential CEOs in the world.

That’s why earnings season is my favorite – and busiest – time of year. I’ll sift through transcripts from dozens, sometimes hundreds, of companies. It’s time-consuming work, but it’s how we uncover signals the mainstream media will only recognize months later.

Each report gives us a fragment of the bigger picture. Piece them together, and you start to see an image of the global economy. And right now, that image is one of a strong economy.

Of the 497 large-cap companies in the S&P 500, 458 have reported so far. Nearly 67% beat sales estimates, and an impressive 82% beat earnings expectations. That’s broad-based strength.

The standouts? Technology and energy. Two themes we’ve been pounding the table on here at Brownstone Research.

The ongoing AI infrastructure buildout is funneling billions into the tech companies that design, manufacture, and install the hardware running artificial intelligence.

And the power companies supplying the electricity for these AI factories are seeing surging demand that’s turning the grid itself into the next great bottleneck.

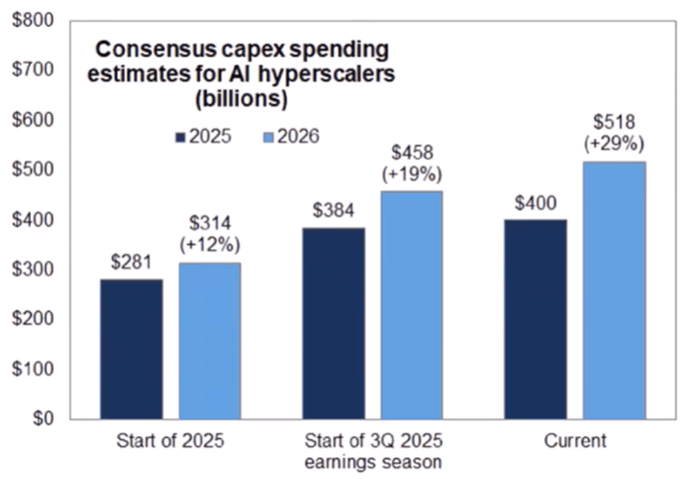

One of the most striking trends this season is the unrelenting capital spending from the hyperscalers – Microsoft, Google, Amazon, Oracle, and Meta.

At the start of this year, their combined capital expenditure (CapEx) plans stood at roughly $281 billion. After this latest round of earnings, that figure has surged to around $400 billion – a jump of more than 40%.

And looking ahead, they’ve already lifted their 2026 projections by nearly 70% since the start of the year.

AI hyperscalers include AMZN, GOOGL, META, MSFT, ORCL

Source: FactSet, Goldman Sachs Global Investment Research

These are staggering numbers. Yet they make perfect sense.

Every one of these companies is racing to build more compute capacity. And aside from Meta’s chaotic earnings call – where management openly admitted they can’t secure enough GPUs – each hyperscaler raised revenue guidance again this quarter.

Wall Street is struggling to make sense of it. Analysts keep asking: How much more can they spend relative to free cash flow?

The theory these analysts are working on is that the companies will only spend as much on CapEx as they bring in in free cash flow. We’ll bust that myth in a moment. But it’s important to know what Wall Street is looking at to know how they will judge good investments for their clients.

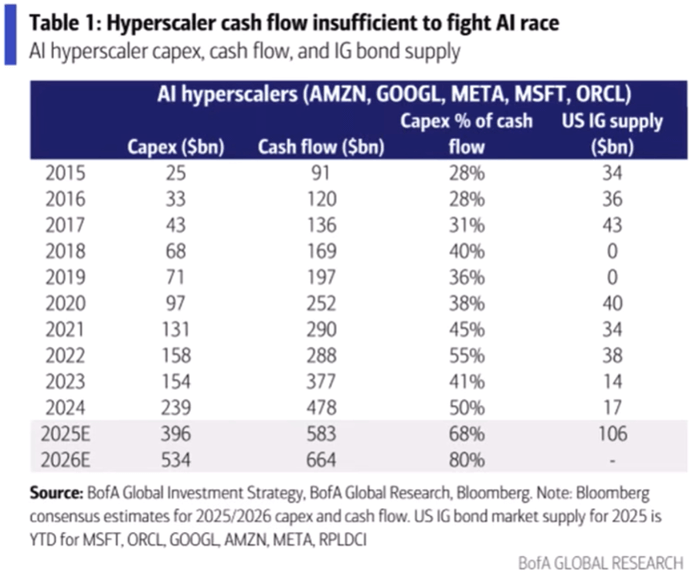

As the table below shows, the hyperscalers’ annual capital expenditures are rising rapidly as a percentage of free cash flow. By next year, they’re expected to reinvest nearly 80% of cash flow into new infrastructure.

Conventional analysts look at that figure and reach a predictable conclusion: CapEx growth must slow.

They reason that if spending is already consuming most of free cash flow, it can only rise at the same rate as cash flow, about 14%, instead of 35%+ we’ve seen over the past years.

And if that happens, they argue, the growth engine driving the semiconductor and infrastructure sectors will sputter.

But that view completely misses the bigger picture.

The hyperscalers are not cash-constrained startups. They’re among the most profitable companies in human history. And they are sitting on fortress balance sheets and almost no debt.

When lenders issue corporate bonds, they typically cap a company’s leverage using a ratio known as debt-to-EBITDA. Mature, stable businesses can safely operate around 4x EBITDA.

That’s where Oracle sits today. But the other “Big Four” hyperscalers average a ratio of just 0.6x. Collectively, they’re projected to generate more than $750 billion in EBITDA next year.

If they merely levered up to the same conservative 4x standard, they could increase their debt by 3.4x EBITDA (a target of 4x minus the current 0.6). That means these companies could borrow an additional $2.5 trillion. And they could borrow that money without straining their balance sheets or jeopardizing their credit ratings.

That’s enough dry powder to fund years of accelerated AI infrastructure growth.

And lenders are eager to provide it. As Apollo Global Management CEO Marc Rowan put it…

Our business is financing the global industrial revolution, whether it’s infrastructure, energy, energy transition, data centers, defense, new manufacturing, or robotics. The demand for capital has never been stronger […] it is a worldwide phenomenon.

That statement captures the scale of what’s unfolding. Credit markets aren’t tightening – they’re expanding to meet the capital needs of a new industrial age.

Many investors still view hyperscalers through the old software lens where businesses scaled with code, not concrete. But the reality is that we’ve entered a capital-intensive era for compute. The new industrial complex isn’t made of steel mills or oil refineries…

It’s built from AI data centers.

And that means the CapEx growth rate can continue at a much higher clip than most expect.

The biggest surprise of this earnings season didn’t come from the GPU giants. It came from the oft-overlooked memory makers. These are the companies that manufacture HDDs (hard disk drives), NAND (solid state hard drives), and high-bandwidth memory (HBM). These store data used and generated by the AI models.

The four key players are Western Digital (WDC), Sandisk (SNDK), Seagate (STX), and Micron (MU). Near Future Report subscribers will recognize Micron – we’re sitting on gains of 138% there.

And the tailwinds are strengthening. Across the industry, supply is tightening. HDDs, NAND, and HBM are all in short supply. The result is the strongest pricing power the memory industry has seen in over a decade.

One company in particular shocked Wall Street.

Sandisk just posted one of the biggest earnings surprises we’ve ever seen from a $10-billion-plus firm. Revenue beat expectations by 7%. Earnings per share beat by 22%.

But the real fireworks came from forward guidance. Sandisk raised next quarter’s adjusted EPS forecast from $1.75 to $3–$3.40. Nearly doubling expectations.

For a mature, profitable hardware company, that kind of revision is extraordinary.

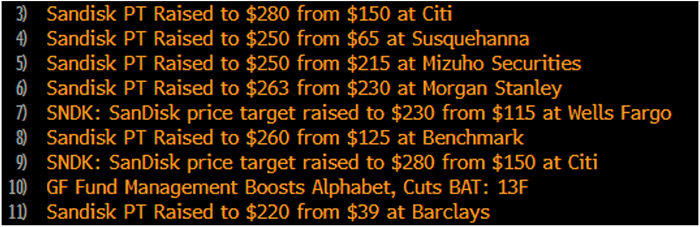

Analysts were caught flat-footed. Barclays led the scramble, lifting its price target from $39 to $220 – a 460% increase overnight. Others quickly followed suit, as Wall Street realized it had underestimated both demand and profitability across the memory sector.

Here’s a list of a few others.

The reason for the beat is relentless demand from AI data centers. Sandisk CEO David Goeckeler said…

In the first quarter, demand for our NAND products continued to outpace supply, a dynamic we expect to persist through the end of calendar year 2026 and beyond. In response, we are making strategic allocation decisions to maximize long-term value creation.

That’s corporate speak for saying customers want more than Sandisk can deliver. And the company will prioritize its best long-term clients in the coming years. Not everyone will get all they want.

For a company, that’s a good position to be in. The whole memory industry will have pricing power for the coming years. For an investor, that means expanding margins, stronger earnings, and a multiyear growth runway.

The broader message from this earnings season is unmistakable. The AI infrastructure boom is not slowing down.

Even smaller semiconductor firm Lattice Semiconductor (LSCC) reported it is “starting to work closer with some of the neo-Cloud and enterprise vendors.” That’s code for a flood of new AI-driven customers entering the ecosystem.

And the giants continue to double down.

At an analyst day earlier this week, AMD CEO Lisa Su forecast 35% annual revenue growth for the next three to five years… and 80% average annual growth in AI data-center sales alone.

Su said the hyperscalers that once expected a spending plateau are now accelerating investment. “It’s not going to level off,” she said.

Meanwhile, Cisco Systems (CSCO) just beat estimates and raised guidance. It cited surging demand for secure networking “as customers move quickly to unlock the potential of AI.”

Every signal points in the same direction. AI spending is accelerating.

We’re witnessing the strongest earnings momentum of the AI era. From hyperscalers to semiconductor suppliers, the data shows the same pattern – rising revenue, expanding guidance, and growing capital commitments.

Yes, the Nasdaq 100 is up nearly 50% in the past seven months. That pace won’t last forever. But the underlying trend is durable. The AI buildout will span years, not quarters.

AI isn’t a bubble. It’s the backbone of the next industrial expansion. And every earnings season confirms it.

For investors able to look a few years ahead, this remains the most predictable growth wave of the decade. The companies providing the compute, memory, power, and connectivity for AI factories are entering a multiyear supercycle of demand.

Stay patient. Stay invested. The AI factory age is just beginning.

Regards,

Nick Rokke

Senior Analyst, The Bleeding Edge

Read the latest insights from the world of high technology.

Even with all of the excitement happening right now with AI, the 2026 hyperscale spending on AI infrastructure still...

The permissionless agentic economy is coming to life…

The breakup needed to be public and raw so that it was believable.

Thanks for signing up for The Bleeding Edge — we’re glad you’re here!

Want updates sent straight to your phone too? Sign up for SMS alerts to get the latest delivered via text.

Brownstone Research: By submitting your phone number, you agree to our SMS Terms & Conditions, Terms of Use, & Privacy Policy, and give express written consent to receive marketing text messages from BSR. Messages are recurring & frequency may vary. Reply STOP to 94703 to opt out. Reply HELP to 94703 for info. Consent is not a condition of purchase. Message and data rates may apply. For additional information, you may contact Customer Service at 888-512-0726 or smssupport@brownstoneresearch.com.