The Bleeding Edge

9 min read

Earnings Season Update: The Untold Winners of the AI Spending Wave

As well as a quick update on earnings season, I want to share one overlooked segment of the AI buildout…

Written by

Published on

Aug 12, 2025

We’re now past the bulk of second-quarter earnings reports. And the results have been impressive.

When evaluating the health of the market, we don’t just glance at stock prices or broad economic headlines. We get as close to the source as possible. And one of the best ways to do that is to tune into company earnings calls and management commentary.

Earnings are hard numbers that show how each business is really doing. Sure, management can finesse some numbers, like earnings per share, to engineer a small beat, but others, like free cash flow, are tougher to manipulate. A company either earned and kept the cash or it didn’t.

Earnings calls are like sitting down in a private meeting with management. They’ll share what they’re seeing with customer demand, the challenges they’re facing, and how they expect the future to unfold.

It’s why earnings season is my favorite time of the year… and my busiest. I’ll comb through transcripts from dozens, sometimes hundreds, of companies. It’s a time-consuming process, but it’s the best way to uncover insights before most other people.

Every company gives us a small piece of the puzzle. If you want to get a clear picture of a particular industry, just listen to the calls of all the major players in that industry. It’s incredible how much you can learn.

And if you want to get a bigger picture perspective, listen to calls from leaders in several key industries. Put them together, and you get a high-definition picture of the economy and the stock market.

And this quarter, that picture was remarkably strong. Of the 497 large-cap companies in the S&P 500, 453 have reported so far. Nearly 70% beat their sales estimates, and 81% beat earnings expectations.

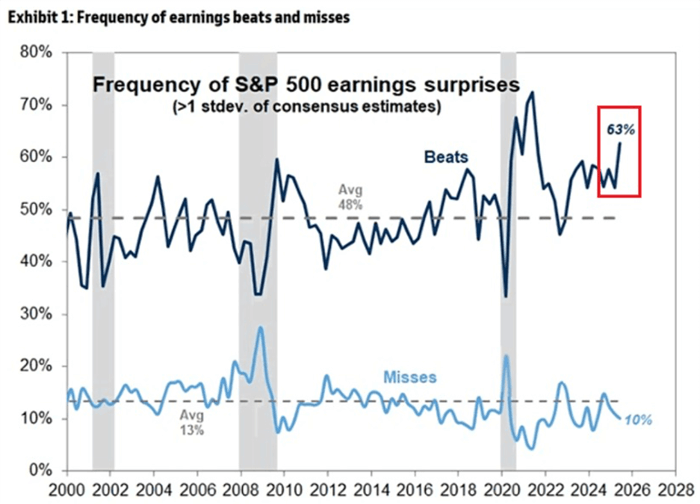

These weren’t penny-by-penny “engineered” beats either. According to Goldman Sachs, 63% of companies topped earnings forecasts by at least one standard deviation. This is a statistically significant surprise. In a typical quarter, only 48% manage to do so. Excluding the immediate post-pandemic recovery, this is the highest level in more than 25 years.

Source: Goldman Sachs Global Investment Research

Even the misses were rare. Only 10% of firms fell short by a standard deviation or more, well below the long-term average of 13%.

This is strong earnings momentum. And we see broad strength at the discretionary and luxury ends of the economy.

Spending Strength at the Top

Outside of rate-sensitive sectors like housing and autos, the rest of the economy is still showing resilience. Visa (V) and Mastercard (MA) both reported healthy consumer spending. But the real story is who is spending.

U.S. Bancorp (USB) said, “Consumer spend remains resilient, especially in nondiscretionary spend.” Marriott (MAR) said its “Revenue per available room was strongest at the high end with luxury.” And Ferrari has already sold out its entire new car lineup through next year.

Money is still moving in the middle and upper classes. We are seeing some cracks in lower-income spending, but at the same time, the rural population is spending more.

But strength isn’t universal. High-ticket industries – where purchases often require financing – are feeling pressure from high interest rates.

Real estate in particular is under a lot of pressure. Credit score issuer Fair Issac (FICO) said, “elevated interest rates and ongoing affordability challenges continue to weigh on the mortgage market, keeping loan originations below historical norms.”

Its competitor Equifax (EFX) concurred, saying that hard mortgage inquiries have declined 9% from this time last year. And digital real estate platform OpenDoor (OPEN) said during its earnings call that “only 12% of consumers expressed that it is a good time to buy a home. And sellers currently outnumber buyers by the widest margin in over a decade.”

On the ground, the story matches the data. A South Florida real estate agent told me last week, “It’s a buyer’s market down here.” Homes are taking longer to sell, and sellers are increasingly making concessions to close deals.

Autos are also showing signs of slowing. Autoliv (ALV), which develops safety systems for vehicles, expects global light vehicle production to decline more than 2% this quarter.

Yes, there are cracks in the economy. But they’re the kind of cracks lower interest rates can repair.

And after last week’s Bureau of Labor Statistics restatement revealed much slower job growth than previously reported, the Federal Reserve finally has the political and economic cover it needs to cut interest rates. We expect the first cut will come in September.

But outside of these interest rate-sensitive sectors, economic activity is strong. And businesses are raking in record profits. So if the Fed starts easing while this momentum continues, the stock market will take off.

Between now and mid-September, we expect some volatility. This is a historically weak time of the year for the markets, and the Fed’s unwillingness to cut rates will create some economic uncertainties.

If there are any pullbacks, be prepared to buy the dip. Especially in sectors showing strength. And the strongest sector, of course, is artificial intelligence (AI).

AI Hyperscalers Are Unleashing Historic Spending

The biggest surge in spending isn’t coming from consumers, it’s coming from the AI hyperscalers. This earnings season confirmed that the AI infrastructure buildout is just beginning to accelerate. Last week, Jeff told Near Future Report subscribers:

During last week’s earnings call, Meta CFO Susan Li revealed that the company raised its capex floor from $66 billion to $72 billion, adding that they plan to “ramp our investment significantly” in 2026.

We estimate that Meta is likely to spend more than $100 billion on infrastructure next year alone. Just one company, more than $100 billion on AI infrastructure.

Meta isn’t alone. Musk’s xAI raised $10 billion last month and is seeking another $20 billion from venture capital/private equity to build a 1 million GPU supercluster to accelerate development of his Grok AGI LLM.

During Google’s (GOOGL) latest earnings report on July 23, they raised their planned capex 13% to $85 billion this year.

Last week, Microsoft (MSFT) said it would spend $30 billion on AI infrastructure this quarter alone. That annualizes out to $120 billion in annual spend in its current fiscal year. Here’s a chart of their capex growth.

And not to be outdone, OpenAI and Oracle (ORCL) just agreed to 10x the size of their Stargate data center capacity. This is a move that could add another 5GW of AI data center demand.

We’re not just seeing a short-term boom here. We’re watching the birth of an entirely new industrial sector, what we’re calling AI factories.

The Birth of “AI Factories”

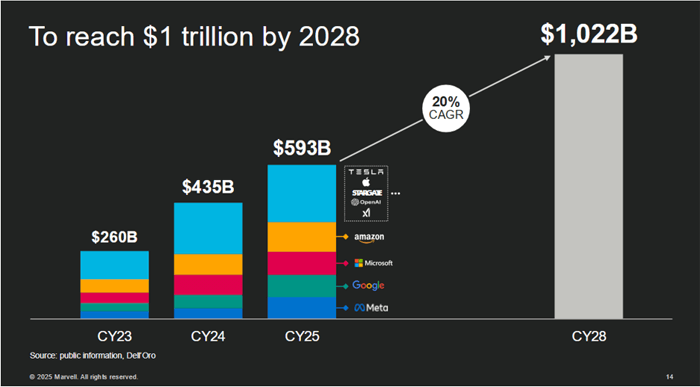

This year, total AI capex among major AI hyperscalers is projected to reach $593 billion in AI spend. And by 2028, hyperscalers will likely spend over $1 trillion building out AI infrastructure. It’s worth noting that six months ago, the forecast was that spend would hit $1 trillion by 2029. That has already been pulled in by a year.

Source: Marvell

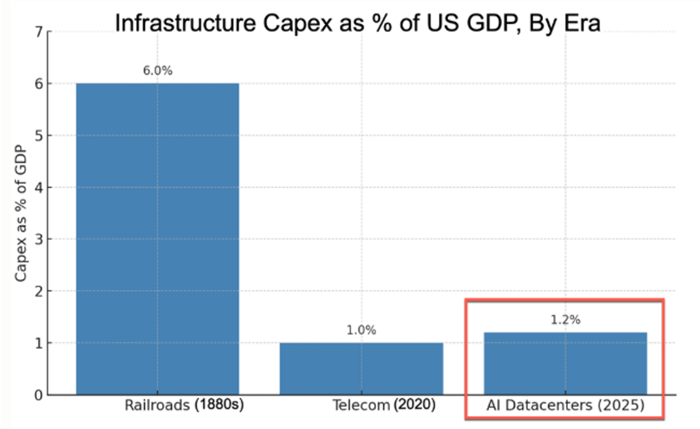

Now, this isn’t completely unprecedented. While this is nominally the largest infrastructure buildout ever, it’s not in terms of spending to the overall economy. To make an apples-to-apples comparison of the magnitude of the spend, we should compare the spend to the country’s economic output. In this case, it will be GDP.

And the chart below shows that AI datacenters currently make up 1.2% of all US GDP. That’s in line with the 1% of Telecom buildout for the 5G rollout in 2020. This was a trend longtime Brownstone Research subscribers were in on early and profited handsomely from.

But we are still well below the 6% of GDP spent on railroads in the 1880s. And I’m sure the electrical buildout in the 1900s, the interstate project, and broadband cables all contributed more towards GDP than AI.

Source: paulkedrosky.com, Jens Nordvig

So spending could still 5x from here and not be as large a part of the economy as the railroad buildout was in the 1880s.

So a double in the next few years, historically, would not be anomalous to the current economy. And if spending on AI infrastructure reaches $1 trillion, they will need a lot of semiconductors, networking equipment, and electrical supplies.

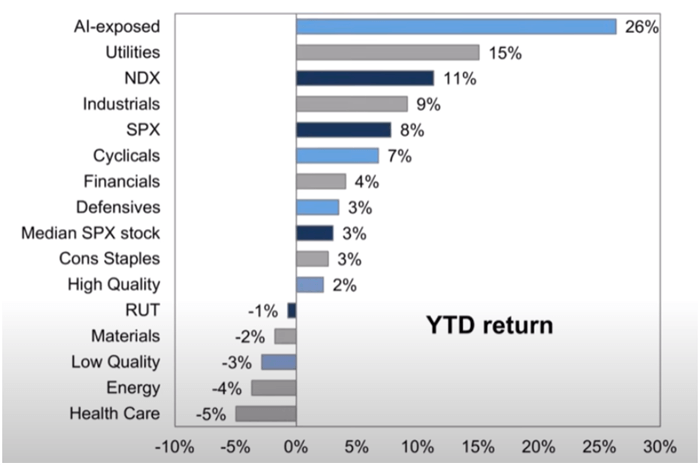

This spending has lit a fire under AI stocks. If we look at the year-to-date return of AI-exposed companies, we can see they’re up an average of 26% on the year.

Source: Goldman Sachs

Big money is moving towards this sector. And with capital pouring in, a pullback could give us the opportunity to own the foundational players at a discount before the next leg higher.

Now we could just say to buy AI-related stocks and leave it at that, and, for Near Future Report and Exponential Tech Investor subscribers, to continue holding the companies in the portfolios.

But I want to share one overlooked segment of the AI buildout with everyone.

The Builders of the AI Infrastructure Boom

When investors think about AI, they usually picture chipmakers like NVIDIA (NVDA) or software leaders like Google (GOOGL) or data center providers like Amazon (AMZN). But there’s another group of companies quietly riding the same wave… and they’re growing just as fast.

These are the infrastructure specialists. The mechanical, electrical, and cooling experts. The firms that pour the foundations, wire the power, and install the systems that keep AI data centers running 24/7.

Once considered boring and predictable, they’ve now become some of the fastest-growing companies in the market. This has sent their prices soaring in recent months. But a pullback could provide attractive entry points.

One of the most prominent examples is EMCOR Group (EME). EMCOR provides mechanical and electrical construction, facilities services, and HVAC systems.

On July 31, EMCOR reported a beat and raise quarter that sent its stock surging 10%. A large reason for that was that its AI offerings grew 119% year-over-year inside its Network & Communications division.

That division is now EMCOR’s largest, accounting for 32% of its remaining performance obligations (RPO). And despite nearly doubling from April lows, the stock still trades at a reasonable 17x EV/EBITDA (enterprise value to earnings before interest, taxes, depreciation, and amortization).

Cooling the AI Factories

AI data centers consume enormous amounts of power… And that power generates enormous amounts of heat. That’s why HVAC is so important. And why cooling companies like Carrier (CARR) and Trane (TT) are also seeing major growth.

Carrier reported that its AI-related revenue doubled from the second quarter of 2024. Trane echoed the trend, noting broad growth in sectors with large capital investments like data centers.

But they also hinted at the bigger opportunity ahead: services revenue. Its applied solutions division (which houses its AI offerings) often generates 8 to 10 times the initial equipment sale in long-term service revenue.

In other words, every installation today creates a recurring cash flow stream for years to come.

But before the servers get installed and cooling units turned on, companies like Sterling Infrastructure (STRL) have quite literally paved the way. Sterling handles the foundational phase of construction: clearing land, grading, paving, and installing underground utilities. This is the groundwork for AI factories.

And in its latest quarter, Sterling also said data center revenue doubled. For a company in such a traditional, steady industry, that’s remarkable.

The Foundations of a Multi-Year Boom

Earnings season confirmed that AI infrastructure spending is in the early stages of a multi-year expansion. The hyperscalers are committing hundreds of billions of dollars to build the data centers of the future.

But they can’t do it alone. They need the EMCORs, the Carriers, the Tranes, and the Sterlings of the world to design, build, and maintain the physical backbone of AI computing.

These companies are no longer just “steady Eddies.” They’re growth stories in disguise. And some even have the added benefit of recurring service revenue that can compound for years.

If the market pulls back before the Fed’s September meeting, these foundational players could be among the best opportunities to position ahead of the next leg higher in the AI buildout.

Because when the AI factories of tomorrow come online, it will be these companies that will have laid the groundwork from the very start.

Nick Rokke

Senior Analyst, The Bleeding Edge

Nick Rokke

Senior Analyst

More stories like this

Read the latest insights from the world of high technology.

-

-

The Iran Oil Shock: Why Market Fear May Be Setting Up the Next Rally

Over the past week, the conflict with Iran has escalated dramatically. And the most critical chokepoint in the global...

-

A Sign of What’s to Come

Private investment rounds like this are illiquid. It’s not trading, it’s an investment. This is a sign of what’s...