Labor in the Age of AGI

This crisis will be full of danger and fear, but it will also be full of incredible opportunities…

We’re witnessing the next phase of the AI revolution where the bottleneck isn’t chips anymore… It’s power…

Managing Editor’s Note: Tomorrow at 8 p.m. ET…

Our friend, Market Wizard Larry Benedict, is revealing his strategy for targeting triple- and quadruple-digit wins with ONE ticker over and over again…

All you have to do is place a unique kind of trade when the next “24-Hour Profit Window” opens up. This is the same strategy that made Larry’s former hedge fund clients over $274 million in profits…

In the first quarter of 2025, Larry’s strategy produced an 81% win rate. In Q2, his strategy won 71% of the time… In Q3, it won 89% of the time… And so far in Q4, Larry’s 24-hour profit strategy has won 89.47% of the time.

Larry says he can’t tell you what the market will do in the coming weeks…

But he CAN tell you when the next 24-Hour Profit Window will open.

If you’d like to be ready, join Larry for the details of how it works at his event tomorrow.

Go here to RSVP with a single click.

Yesterday, we unlocked the first part of our October Near Future Report issue and showed how September changed everything.

That was the month when AI spending went vertical. Budgets jumped from billions… to tens of billions… to hundreds of billions.

The global race to build artificial general intelligence (AGI) and, eventually, artificial superintelligence (ASI) is well underway.

We’ve spent the past year and a half positioning for this moment by methodically building a portfolio of the companies that are providing the technology, hardware, and energy infrastructure that make AI possible. And the results speak for themselves.

Our average position that’s more than three months old – long enough for the thesis to play out – is up 60.6%. With an average holding period of 491 days, that works out to an annualized return of 45%.

That’s the power of investing in the right trend before Wall Street catches on.

We’re witnessing the next phase of the AI revolution where the bottleneck isn’t chips anymore… It’s power.

We’ve moved from GPUs to gigawatts.

The companies that can generate, store, and deliver massive amounts of electricity – cleanly and reliably – will be the next wave of winners.

In today’s issue, we’ll pick up where we left off and reveal where the next set of opportunities will come from.

The AI era is entering its energy phase.

And for investors who understand what’s happening, this is where the next fortunes will be made.

The race to ASI isn’t just about who can code the fastest. While software architecture, training data quality, and technique are critically important, the most significant competitive advantage comes from how quickly a company can build, commission, and power AI factories.

That’s why Sam Altman, Elon Musk, and all the other major players are in such a race to beat each other to the largest AI factory clusters and gain access to the most power.

These data centers will likely require over 100 GW of dedicated power supply to eventually achieve a breakthrough like artificial superintelligence (ASI). Power availability and the cost of delivering that power are now the gating factors for data center deployment.

We use gigawatts because it captures the whole scale – compute, cooling, transformers, and all the industrial hardware needed to keep these facilities running around the clock.

We can debate future chip counts or network cabling. We can’t debate physics. And steady grid-scale power is non‑negotiable.

And 100 GW is no small number. It’s enough to supply about 100 million U.S. homes. And this is also how we know that Wall Street is still behind the curve.

Many analysts rely on long‑range research from groups like ICF International. These firms do in-depth research. They are experts in their fields. But, just like with Wall Street analysts, there is a risk when one firm sounds too far out of the consensus. This creates a kind of “groupthink” in the research world.

If a firm releases a report similar to everyone else and it’s wrong, they were all wrong, so no one looks foolish. But if a firm makes a prediction that’s far from the mainstream AND they are wrong, its reputation takes a nose dive.

Most investors follow a similar path. And that’s why they produce average returns.

The best investors are willing to look forward, and see how the world will change… and how that will impact the market. That’s what we strive to do here at Brownstone Research.

I’ve been doing this now for a decade, and I’ve lost count of how many times my forecasts or predictions were considered crazy by “experts” in their fields, and yet, those predictions have been proven correct time and again.

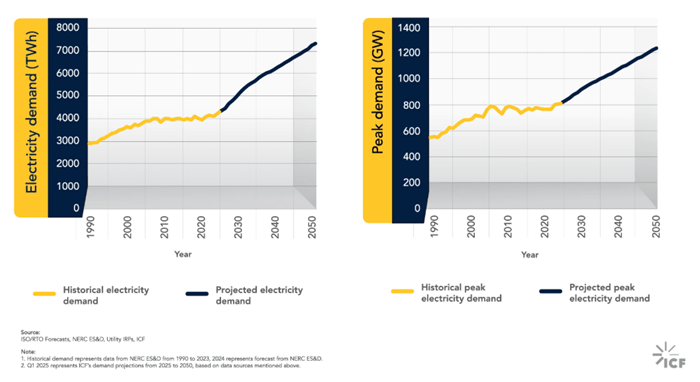

ICF International’s charts show U.S. electricity demand rising steadily over the next 25 years.

Please excuse the poor labeling – these research firms usually aren’t known for making their information easily digestible. On the left is the total annual electricity demand for the U.S. This is measured in total terawatt hours (TWh) because the demand load for businesses and homes is variable.

But for AI, the key isn’t total annual consumption, it’s peak load. These facilities run close to full capacity and add directly to the grid’s maximum demand.

ICF projects that peak demand will climb from roughly 800 GW today to 1,200 GW in 2050 – a 400 GW increase. On paper, that looks like a lot. But compare it with what the operators themselves are saying.

Sam Altman recently shared in an internal OpenAI Slack channel that he expects OpenAI will require nearly 250 GW of new electrical demand by 2033 alone.

And here’s the thing: If OpenAI does it, xAI will have to add 250 GW. Google will have to add 250 GW. Microsoft will have to add 250 GW. Meta will have to add 250 GW.

Those five companies alone could more than triple the Street’s 25‑year growth forecast… in just eight years. And that doesn’t count Amazon, Alibaba, Oracle, CoreWeave, Nebius, or sovereign programs, all adding material demand of their own.

At Brownstone Research, our conclusion is clear. Wall Street is drastically underestimating the earnings potential of the companies that generate, deliver, and manage dependable electricity. We have our eyes on a select group of names poised to benefit.

We’re watching multiple companies that manufacture the power generation equipment.

First, we have natural gas turbines. Natural gas will remain a vital baseload power source for many of the data centers being built near shale-rich regions, from Texas all the way up to North Dakota. The four largest companies in the world that manufacture natural gas turbines include Siemens Energy, GE Vernova, Mitsubishi Heavy Industries, and Shanghai Electric Group. All four are seeing astronomical demand.

The U.S. has plenty of natural gas, but it’s not unlimited. And while solar power continues to see the most annual capacity additions, it’s intermittent by nature. Some data centers are using solar to charge utility-scale batteries. Batteries are improving, but they still can’t deliver the kind of round-the-clock power these AI data centers require. Solar cannot be the sole provider of electricity for these plants. Not even close.

That’s why our position has long been centered around nuclear power, well before nuclear became popular again.

Eventually, I believe nuclear fusion will become the dominant power source. It’s the real power of the sun, but it will take a couple of decades to build out the grid-scale infrastructure to accomplish that.

Shorter-term, the best answer is nuclear fission using uranium, the most energy-dense fuel on Earth. And there is already a renewed effort to recommission fission reactors, as well as aggressively push ahead to the next generation of nuclear fission technology.

Demand for nuclear is about to go off the charts.

There are a few companies that manufacture equipment for nuclear plants, such as conventional boiling water reactors. And they are still going to see a fair amount of demand. But more exciting is the small modular reactor (SMR) business.

SMRs are next-generation reactors. They’re smaller, safer, and can be built to match the specific power needs of an AI data center. And whereas traditional plants require refueling every year or two, SMRs can operate for up to 30 years without a single refuel.

We are also monitoring other SMR companies, including Oklo (OKLO) and Nuscale (SMR). But these companies are years away from any meaningful revenue. These are not the safe, stable companies we look to invest in at The Near Future Report.

And for those who want direct exposure to the underlying fuel, we continue to favor the Sprott Physical Uranium Trust (SRUUF). Longtime readers may remember we added SRUUF to the portfolio back in 2022. It remains one of the most efficient ways to play the rising uranium demand.

On the operator side, we’re keeping a close eye on Constellation Energy Group (CEG) and Vistra (VST). These two companies operate some of the largest nuclear fleets in the U.S. – and they’re well positioned to renegotiate long-term power purchase agreements as demand soars.

Taken together, these are the companies that will power the AI economy.

We are watching closely for pullbacks in these companies and more. If we see pullbacks or attractive entry points, we won’t hesitate to issue a mid-month alert. Our goal is to help readers establish positions in these next-generation energy companies before the rest of Wall Street wakes up.

Jeff

Read the latest insights from the world of high technology.

This crisis will be full of danger and fear, but it will also be full of incredible opportunities…

NVIDIA’s new licensing deal with Groq may not be a formal acquisition, but in terms of antitrust regulations, it...

When Elon Musk launched his newest company, xAI, in January 2024, most didn’t take him seriously…