Agentic AIs Need Social Interactions Too

The more transactions that take place over Meta’s networks, the more money it makes. So why limit that to...

The direction is clear. Interest rates are coming down.

Managing Editor’s Note: Thank you to everyone who joined us on Wednesday for Jeff’s Hyper Acceleration event.

We had a great time. Jeff did a deep dive into the technological convergence fueling this market hyper acceleration… the technologies most substantially impacted… and how we can make the most of it.

There have only been two other hyper acceleration events in history. And this one is shaping up to be even more impactful. It’s truly an exciting thing to witness.

We also understand that not everyone could attend on Wednesday… But we’d hate for anyone interested to miss out on Jeff’s message. That’s why we’re making a replay available to you, in case you missed it.

You can go here to access it.

It was an exciting morning.

The markets liked what they heard on the back of Fed Chair Powell’s remarks at the Jackson Hole symposium hosted by the Federal Reserve Bank of Kansas City.

It was a neutral speech, leaving a lot of wiggle room for Powell on the timing and degree of when the Fed will reduce the Fed Funds rate. But one thing is for sure…

Rates are coming down.

Powell noted that…

In the near term, risks to inflation are tilted to the upside, and risks to employment to the downside – a challenging situation.

He is overestimating the risks of a rise in inflation, as the numbers have clearly shown a downward trend, and economic and fiscal policy are supporting lower inflation.

The real key will be what happens with the labor markets between now and the next FOMC meeting. Any further weakening in employment will all but guarantee a cut in September.

Not surprisingly, Powell leaned again into following the data:

Monetary policy is not on a preset course. FOMC members will make these decisions based solely on their assessment of the data and its implications for the economic outlook and the balance of risks. We will never deviate from that approach.

But probably his most supportive comment with regard to lowering rates was the following comment…

With policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance.

That’s what got the markets excited this morning, anticipating a September rate cut.

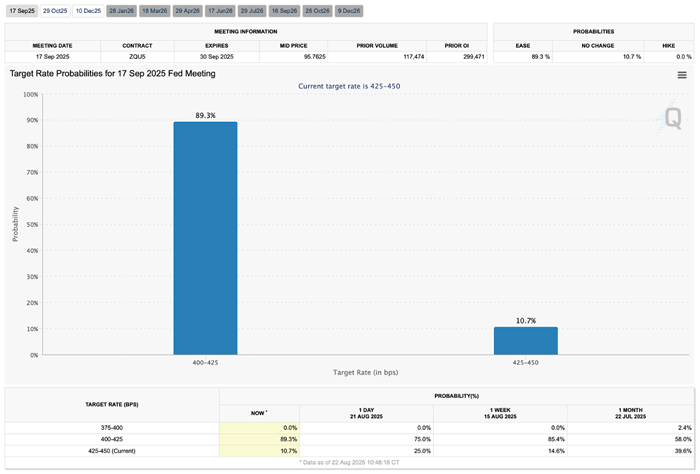

The CME’s FedWatch Tool, which factors in the probabilities for rate cuts in future FOMC meetings, quickly reflected the shift in sentiment, raising the likelihood of a 25-basis-point cut in September from 75% to 89%.

Fed Funds Target Rate Probabilities | Source: CME

Looking out into December, there’s a 50% likelihood that the Fed Funds will decline to the 375–400 basis point range, a full 50 basis points below where we’re at today.

Regardless of the timing, the direction is clear. Rates are coming down.

Jeff

[Regarding Cerebras Systems,] do we really need another chip company?

– Charles M.

Good morning Jeff,

Do you have any updates to share with us on the IPO for CRBS, please?

Thank you so much for your excellent in-depth reports. They are magic.– Darby M.

Hello Charles and Darby,

I’ll tackle the easy question first. Yes, absolutely, we do need another chip company, and we definitely need Cerebras. And we’ll need many more chip companies, given the demands of developing and running artificial intelligence (AI) software.

We need chips optimized for training, we need chips optimized for inference, we need chips for acceleration, and we need chips for memory and storage.

And we can’t forget that semiconductor manufacturing technology advances every year, allowing incremental improvements in semiconductor performance. This enables higher transistor density (transistors are closer together), which results in better performance and lower cost of operation per unit of compute.

Said another way, there are clear economic incentives to continue this incessant drive to innovate with semiconductor technology. It is literally the foundation of all technological advancement.

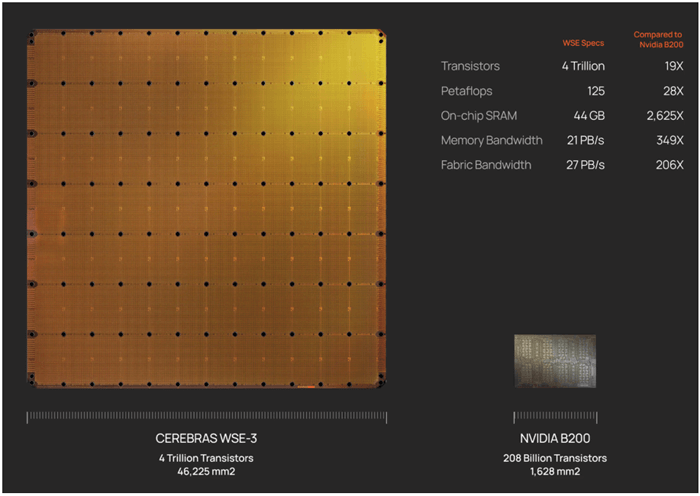

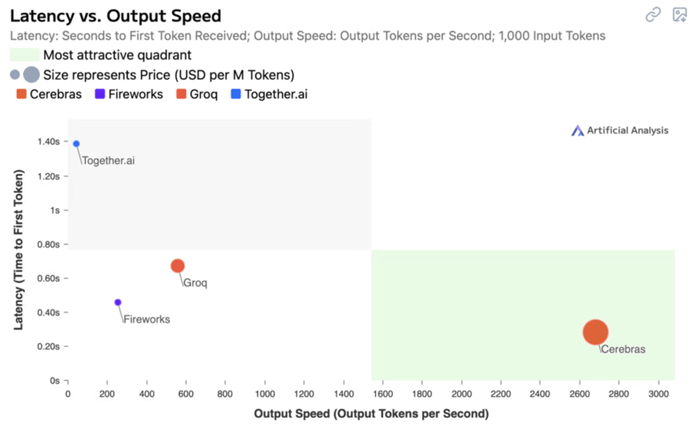

Cerebras is in a unique spot in the industry as it pursued a radically different design, something it calls a wafer-scale engine (WSE), utilizing the entire silicon wafer to produce one massive semiconductor.

Cerebras WSE-3 | Source: Cerebras

The result is incredible performance in inference. Below is a simple chart that analyzes inference performance, as measured by latency (Y-axis) versus output speed (X-axis), running OpenAI’s open-weight model GPT OSS 120B. We can see clearly that Cerebras demonstrates the lowest latency and the highest overall output speed by a large margin.

Inference Performance Running GPT OSS 120B | Source: Artificial Analysis

So yes, the industry definitely needs Cerebras, particularly for running AI applications.

As for Cerebras’ IPO, there have been some recent developments.

Cerebras filed for its IPO in September last year. Its initial delay was driven by regulatory requirements. Specifically, Cerebras had to undergo a review by the Committee on Foreign Investment in the United States (CFIUS).

This was required due to the major of its current business flowing to G42, an Abu Dhabi-based AI and cloud computing-focused firm, which has also invested in Cerebras.

The regulatory hurdles were cleared in March of this year with CFIUS, opening the way for the IPO. However, the market conditions in the spring/summer of this year were not optimal for IPOs, given the economic uncertainties of the trade negotiations and the delays in getting to an agreement between the U.S. and China.

It made sense for Cerebras to wait. I would have done the same had I been running the company. And August is a terrible month to go public, as most of Wall Street is checked out and enjoying vacation.

The latest development is that Fidelity is in talks with Cerebras to lead a $1 billion private funding round. Fidelity is likely to take $500 million of the round. The way to look at this round is like a bridge round to the IPO.

I doubt it will go public in August/September, but I do expect the IPO market to heat up in October through early December. Interest rates are coming down, and the IPO market is showing some strong signs of coming to life.

The Coreweave (CRWV) IPO was strong in March this year, as was Figma (FIG), and there have been a number of other smaller issuances that went very well.

When the IPO wave begins, it will feel like a flood. There are hundreds of great tech companies that have been waiting years for a great window to access the public markets. I’m very excited about what’s coming.

Hullo,

… [It] was recommended that I buy the shares of TSM and ON, which, as I understand, produce their semiconductors in Taiwan.What concerns me is what is projected to happen to the shares if China takes control of Taiwan? I don’t think that China would allow any further trade between these two companies and the USA.

Have I missed something?

All the best.

– Sandy M.

Hullo Sandy,

Your intuition on this subject is correct, as this is definitely a risk for Taiwan Semiconductor Manufacturing (TSM). The company and a large chunk of its manufacturing are in Taiwan.

On Semiconductor (ON), however, is a different story.

While ON does outsource some of its production, one of its competitive advantages is that it has its own manufacturing facilities. Its largest U.S. facility is actually in East Fishkill, New York, which surprises most people.

ON has several other U.S.-based manufacturing facilities as well. This greatly improves its supply chain resilience.

The risk related to China is not something that was overlooked by TSM. I remember years ago when TSM announced it would invest $12 billion in Arizona to build a semiconductor manufacturing plant.

At the time, it was a huge deal, but the rub was that TSM would not be producing the most advanced semiconductors in the U.S.

The plan was to manufacture semiconductors using more mature semiconductor manufacturing processes, leaving the most advanced chipmaking to the plants in Taiwan.

This would have meant that U.S. electronics companies would continue to be entirely dependent upon Taiwan-based manufacturing.

The TSM investment number then jumped to $65 billion, and then the Trump administration proactively engaged with TSM early this year, resulting in an increase of $100 billion in TSM’s manufacturing plants in the U.S.

That brings the total to $165 billion, but the most important part of the deal is that TSM will be using its most advanced manufacturing technologies in the U.S., which protects against the risk of a China takeover of Taiwan.

Not only have I worked extensively in the semiconductor industry for years, but I’ve also been to Taiwan at least 60–70 times. I’ve long maintained that a China takeover of Taiwan won’t be an all-out military conflict. It will look like an administrative takeover.

Most people don’t realize this, but China’s agents have been infiltrating Taiwan for the last two decades or more. They are already there and well established.

And Taiwan is an economic engine that will benefit mainland China greatly. While semiconductor production will likely be used in trade negotiations for leverage, China won’t want to bite the hand that feeds it.

Additionally, the U.S. and China are clearly engaged in trade negotiations, working towards a more balanced agreement. The world didn’t come to an end, and prices haven’t gone through the roof as so many predicted would happen.

The U.S. and China now have until early November to put a new trade agreement in place. And whatever trade agreement is finalized, I’m confident that semiconductors will definitely be part of the deal.

It doesn’t seem like enough real generation power can be produced in the time frame it will be needed. Wind farms and solar won’t do it.

– Willie S.

Hi Willie,

You’re absolutely correct, renewable resources like wind and solar aren’t going to cut it, especially when it comes to powering the energy-hungry AI data centers needed to fuel the rise and advancement of artificial intelligence.

It’s a topic our senior analyst at The Near Future Report, Nick Rokke, wrote about recently in The Bleeding Edge – Meta Goes Nuclear…

We are building the foundation for artificial general intelligence (AGI) and eventually artificial superintelligence (ASI).

These systems won’t just assist researchers and engineers… They’ll become the researchers. They’ll be embedded in government, defense, industry, and consumer applications alike.

And these systems are power-hungry.

AI training runs already rely on clusters of tens of thousands of GPUs operating 24/7. Inference demand – when AI models respond to user inputs – never sleeps. And as AI permeates every aspect of life, power demand will surge.

[…]

And here’s the hard truth: The U.S. energy grid is not ready.

As Nick points out, despite being at the forefront of AI innovation, U.S. power infrastructure, as it stands today, is not equipped to handle the demand surge that will come as AI continues to scale.

And it will continue to scale. We’re already seeing relatively early versions of agentic AI that I expect will quickly become extremely popular once they scale in utility. Of course, every day brings us closer to the first artificial general intelligence (we’re still calling xAI as first to achieve it, and my firm prediction is that it happens no later than March/April next year).

The hyperscalers aren’t slowing down… Morgan Stanley is projecting a spend of $2.9 trillion on data centers from 2025–2028. Most of that is on projects already in progress. It’s locked in. And the government is paving the way for AI innovators and key infrastructure companies to pursue the buildout with more ease.

Which, to your point, means we need the energy to power it.

Short term, the clear answer has proven to be natural gas, which is why the executive orders from the White House have opened the path for the natural gas industry to produce more natural gas to close the gap in energy needs.

Longer term, the best carbon-free source of electricity will come from nuclear energy, but fission and fusion. Where possible, the industry is looking to re-commission old reactors like Three Mile Island and the Palisades owned by Holtec, but that process takes years.

And if you didn’t have a chance to read Monday’s Bleeding Edge – One-Year to Self-Sustaining Reaction… GO!, I recommend doing so. The Department of Energy has selected 11 projects for small modular reactor pilots, the fourth generation of nuclear fission technology, with the goal of having three of those pilots achieve a self-sustaining reaction no later than July 4, 2026.

The industry and the U.S. government are moving as quickly as they can to close this gap and solve the problem with carbon-free energy sources. Wind and solar simply won’t meet the demand.

Nuclear fission and fusion will, so the faster we get there, the better off we’ll be. An abundance of clean energy will obviously be good for the environment, and it will also bring about accelerated growth in the economy.

That’s all for this week’s AMA. I hope everyone has a great weekend.

Jeff

Read the latest insights from the world of high technology.

The more transactions that take place over Meta’s networks, the more money it makes. So why limit that to...

Cortical Labs has been developing a biological computing system based on human brain cells…

Thanks for signing up for The Bleeding Edge — we’re glad you’re here!

Want updates sent straight to your phone too? Sign up for SMS alerts to get the latest delivered via text.

Brownstone Research: By submitting your phone number, you agree to our SMS Terms & Conditions, Terms of Use, & Privacy Policy, and give express written consent to receive marketing text messages from BSR. Messages are recurring & frequency may vary. Reply STOP to 94703 to opt out. Reply HELP to 94703 for info. Consent is not a condition of purchase. Message and data rates may apply. For additional information, you may contact Customer Service at 888-512-0726 or smssupport@brownstoneresearch.com.