NVIDIA’s Tesla-Killer?

NVIDIA has just released its Alpamayo open-source AI models for autonomous driving. But here’s why Tesla isn’t nervous…

Silver is no longer trading like a typical commodity…

Managing Editor’s Note: Before we get to today’s Bleeding Edge issue from senior analyst Nick Rokke, we’ve got a special opportunity to share with you from our colleagues over at The Opportunistic Trader…

Next Thursday, January 15, Larry Benedict is revealing his strategy for profiting from the increasingly wild swings that have been cropping up in the stock market.

Whether it’s stocks that are soaring one day and crashing the next, crypto volatility, or the drastic moves happening in gold and silver – more on that today from Nick – Larry has discovered a way for folks to collect double-digit gains, over and over again, off these moves.

You can go here to automatically sign up to join him next Thursday, January 15, at 8 p.m. ET to hear more about it.

Now, on to today’s Bleeding Edge…

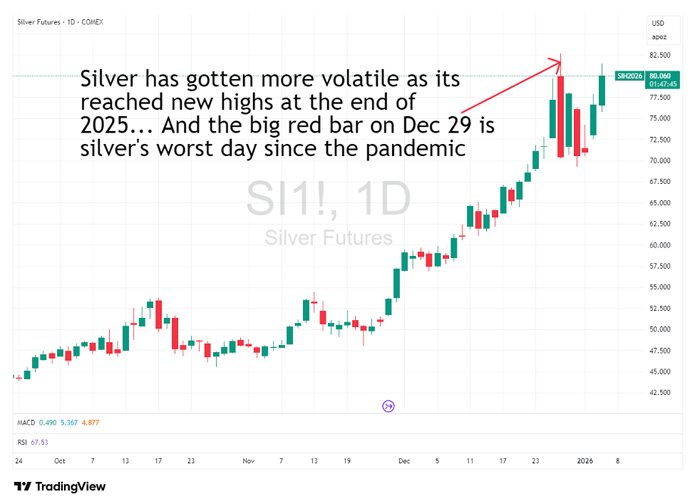

Silver just hit an all-time high after an incredible near-150% run last year.

And yet, if we only look at the price chart, we’ll miss what’s really happening.

Silver is no longer trading like a typical commodity.

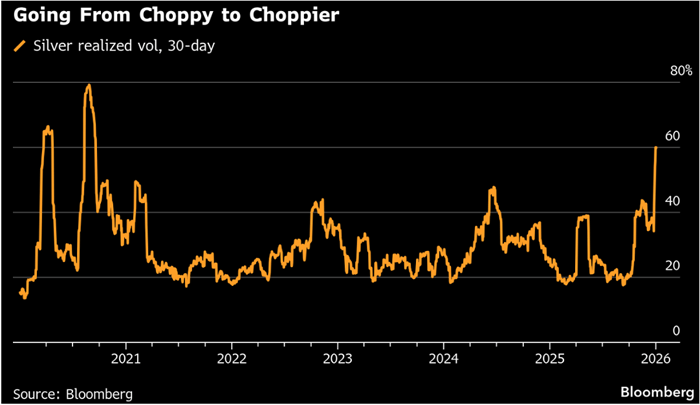

Over the past few weeks, silver market volatility has surged to levels we haven’t seen since the pandemic. On December 29, silver suffered its worst single-day decline since 2020. Large, violent swings have become the norm rather than the exception.

Many observers have pointed to geopolitics as the explanation. Headlines blamed everything from military tensions involving the attack on Russian President Vladimir Putin’s personal residence to the arrest of Venezuelan President Nicolás Maduro. But the instability in silver began well before these recent events.

The real forces driving this market are structural and not based on these one-off events.

We’re witnessing the collision of three powerful trends: a technology-driven surge in industrial demand, a tightening physical supply chain, and growing stress between the paper and physical silver markets. When those forces converge, prices don’t move smoothly. They gap, snap, and overshoot.

That’s what silver is doing today. And it’s why this metal suddenly matters far more than it has in the past.

In The Bleeding Edge, we normally focus on breakthrough technologies shaping the future of investing. Artificial intelligence (AI). Advanced semiconductors. Energy infrastructure. Robotics.

So why talk about silver? Because silver sits underneath all these technological trends.

Silver is the most electrically conductive metal on Earth. That single physical property makes it important to modern technology. Whenever electricity needs to move faster, with less resistance and less heat loss, silver is the preferred material.

That’s why it shows up in high-performance applications.

In AI data centers, silver is used in advanced semiconductors, power management systems, and high-speed interconnects. As artificial intelligence scales, compute density rises sharply.

That drives exponential growth in power demand and with it, heat.

Managing that heat is just as important as supplying the power. Silver plays a role not only in electrical conduction, but also in thermal materials that keep high-density systems operating within safe temperature ranges.

And as data centers increasingly supplement grid power with on-site solar generation, silver becomes part of the energy supply chain as well.

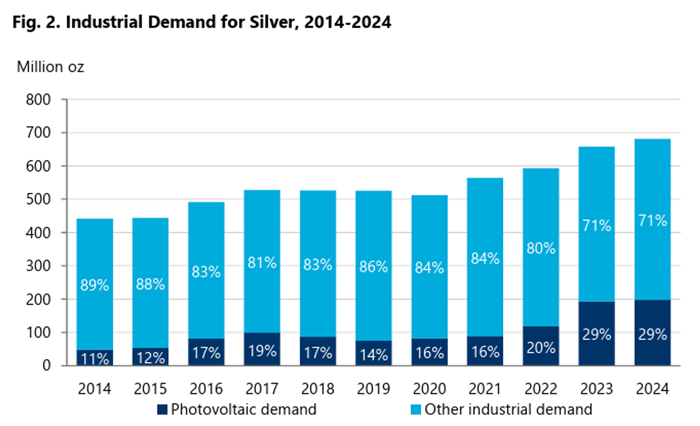

The single largest source of industrial silver demand today is solar energy.

Silver is the primary conductive material used in photovoltaic cells – devices that convert light into electricity. For years, manufacturers worked to reduce silver content per panel to cut costs. That trend is now reversing.

Next-generation, high-efficiency solar cells require thicker, more robust conductive silver films to achieve higher power output and reliability. As efficiency standards rise, silver intensity per panel is increasing again.

The data makes this clear.

Over the past decade, solar power technology’s share of total industrial silver demand has grown from roughly 11% to nearly 29%. Over that same period, total silver demand has risen by about 50%.

Source: World Silver Survey and Oxford Economics

And as global electrification accelerates – driven by AI data centers, EV adoption, and grid upgrades – solar installations are set to grow alongside them.

And industrial demand isn’t the only force at work.

As gold prices have risen sharply over the past year, many buyers have traded down to silver in the jewelry market. At the same time, silver continues to attract interest as a monetary metal.

Historically, silver tends to perform well when interest rates fall. We expect the Federal Reserve to continue cutting short-term rates, with longer-term yields likely following. Large and persistent fiscal deficits have added to concerns about long-term dollar purchasing power.

Gold has already reflected those concerns. Silver is beginning to catch up.

Put it all together, and the picture becomes clear.

Industrial demand from AI, EVs, and solar is rising. Jewelry demand is increasing as relative prices shift. And monetary demand is re-emerging as investors look to hedge currency risk.

These three distinct forces are now moving in the same direction, driving demand higher. And it’s why this market is behaving differently than it has in the past.

The silver market isn’t tight because of a temporary disruption. It’s tight because supply has been structurally insufficient for years.

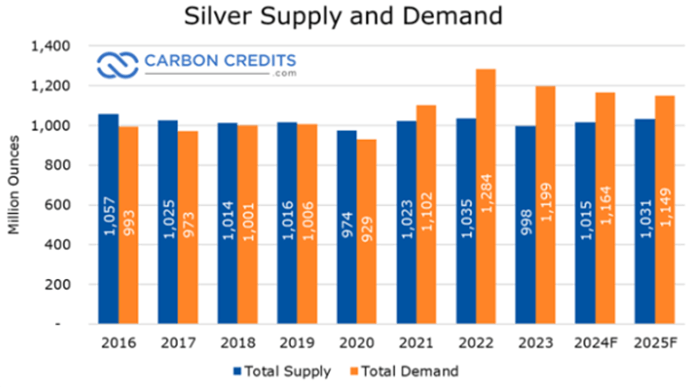

In the following chart, we can see the orange bars on the right, showing that demand has outpaced new supply.

Source: World Silver Survey 2025, The Silver Institute

And in 2024, the market had a deficit of 149 million ounces. That’s about 15% of the total annual global supply.

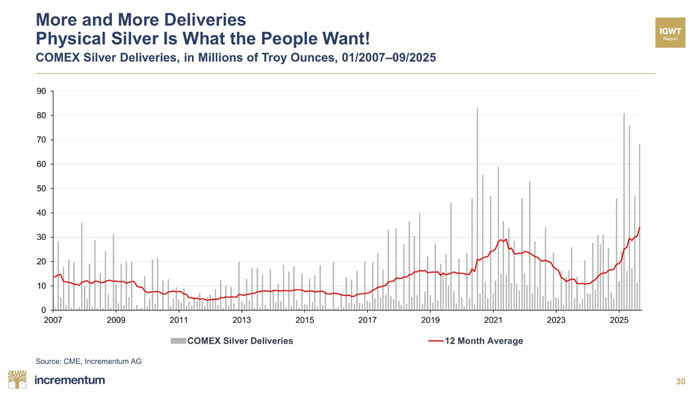

This continued deficit has seen market participants demand delivery of silver. This has been especially pronounced in the United States, where the 12-month average of deliveries has reached an all-time high.

The same pattern is playing out globally. As physical deliveries rise, stockpiles are shrinking.

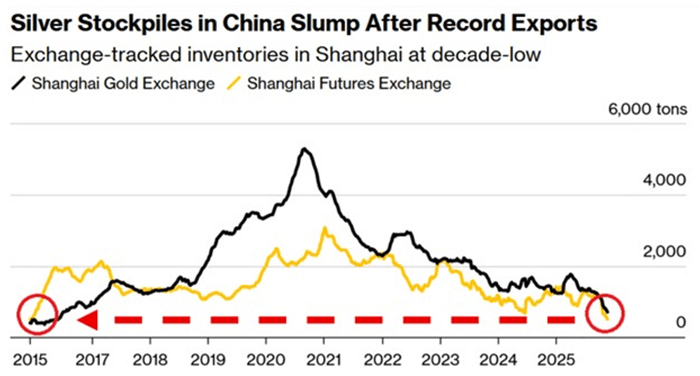

Inventories in Shanghai have been steadily declining as metal is pulled out of storage and put to use.

Sources: Shanghai Futures Exchange, Shanghai Gold Exchange, Galaxy Futures

Note: Date is up to Friday, Nov. 21

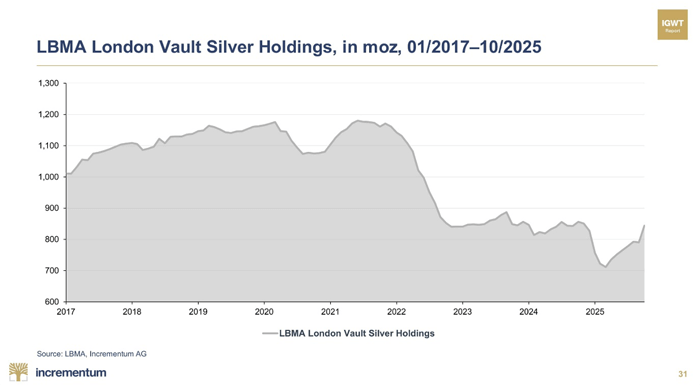

Supplies in London – one of the most important hubs in the global precious metals market – have also fallen. In fact, London inventories would have dropped much further had silver not been shipped in from Shanghai to stabilize the system late last year.

This has led to concerns about a lack of liquidity in London, where much of the silver is stored for the silver ETFs.

And when liquidity tightens in a market dominated by paper claims on physical metal, volatility follows.

We’re now seeing early signs of that strain spilling into the retail market as well. Major bullion dealers such as APMEX and JM Bullion have reported extended shipping times along with periodic stockouts of sovereign coinage.

In most commodity markets, rising prices eventually attract new supply. Silver is different.

Only about 30% of global silver production comes from primary silver mines, where silver is the main commodity being extracted. The remaining 70% is produced as a byproduct of mining other metals, primarily copper, lead, and zinc.

That makes silver supply inherently inelastic.

Even if silver prices rise sharply, production can’t respond unless mining activity for those other metals increases as well. Silver miners don’t simply turn on the taps when prices rise. Supply growth is dictated by decisions made in entirely different markets.

And even for primary silver mines, the timeline is long. New projects require years of exploration, permitting, financing, and construction before producing a single ounce.

The result is a market where demand can accelerate quickly, but supply cannot.

That’s what creates stress. And when a market is already running persistent deficits, it doesn’t take much to push it over the edge.

By the end of last year, the silver market had very little slack left. Inventories were thinner. Physical demand was rising quickly. And then a catalyst hit that turned tightness into volatility.

That’s when things started to move fast.

As of January 1, China has restricted the export of refined silver.

The country implemented new restrictions on refined silver exports. Going forward, any company looking to export silver must obtain government approval for each individual shipment. This isn’t an outright ban. It’s just China ensuring that it maintains enough silver for its own economy. And that has become a meaningful friction point in a market that was already operating with little margin for error.

The implications are significant.

China refines roughly 65% of the world’s silver. That makes it the most important node in the global silver supply chain. If even a small fraction of that refined metal remains inside China rather than flowing into international markets, it tightens supply everywhere else.

And that’s exactly how market participants interpreted the move.

At the same time, the United States formally designated silver as a critical material. This is a recognition of its importance to advanced manufacturing, energy infrastructure, and national security. Taken together, these policy signals that silver is a strategic input.

Producers, manufacturers, and investors responded rationally. They began securing physical silver rather than relying on future availability.

Stockpiling accelerated. And prices moved higher.

As silver prices climbed, exchanges moved to slow the advance.

The CME Group raised the initial margin requirement for silver futures from $20,000 to $22,000 per contract. In a deep, liquid market, a modest increase like that might have been enough to cool activity.

But this wasn’t a normal market. It was the thinly traded holiday period. Liquidity was already limited. And underlying physical conditions were tight.

Buyers absorbed the move. So the CME acted again.

By December 30, the exchange announced a second margin hike. This time to $32,500 per contract. That represented roughly a 60% increase in the cost of carry in less than a week.

A trader or fund holding 100 silver contracts suddenly needed to post more than $1 million in additional collateral, almost overnight. Many speculative funds operate with highly optimized capital structures. They don’t keep excess cash sitting idle.

Faced with sudden margin calls, they had only one viable option: sell.

Liquidation followed. Prices dropped sharply. Not because the underlying fundamentals had changed, but because leveraged positions were forced out of the market.

And just as quickly as prices fell, they stabilized. Because the selling wasn’t coming from long-term holders or industrial buyers. It was simply due to cleaning some speculative leverage out of the silver market. Once the forced liquidation ran its course, demand reasserted itself.

Silver rebounded. And it’s now trading around new all-time highs. That sequence tells us something important. This wasn’t a speculative blow-off top. It was a stress test. And the market passed it. It suggests silver prices can continue higher.

Readers who have followed this closely may have noticed a recurring theme: physical silver matters more than paper exposure right now.

I have seen reports that in Korea, an ounce of physical silver is going for as much as $130 an ounce. That’s roughly 70% higher than today’s paper price of just over $75 an ounce listed on the futures market.

When physical premiums diverge meaningfully from paper prices, it tells us that demand for immediate delivery is rising and that availability is constrained. Futures contracts, after all, are financial instruments. They’re promises. Most are never settled with actual metal.

In normal conditions, that works fine. But in tight markets, it becomes a vulnerability.

As demand for physical silver increases, arbitrage opportunities emerge. Buying futures, standing for delivery, and redirecting metal to higher-priced markets suddenly makes economic sense. When enough participants attempt that simultaneously, paper markets feel the strain.

This is how stress shows up first, not as collapse, but as friction.

That’s why I personally avoid silver futures. They’re highly leveraged, sensitive to margin changes, and exposed to forced liquidation even when fundamentals are improving. We saw that play out recently.

Exchange-traded products tied to silver are a different case. But they aren’t risk-free either.

Take the largest silver-backed ETF – the iShares Physical Silver Trust (SLV) – as an example. The structure itself is sound. The sponsor is reputable. But the metal is held in third-party vaults. And in some cases, those vaults may engage in lending activity to enhance returns.

Under normal conditions, this isn’t a problem. But under extreme physical stress, it introduces a layer of counterparty risk. The odds of a failure are low, but they’re not zero. Investors should understand that distinction before assuming all “physical” exposure is the same.

For investors who want to avoid leverage and counterparty complexity, the most straightforward approach is owning physical silver outright.

Holding coins or bars removes reliance on exchanges, margin rules, or intermediaries. It’s not the most convenient option, and it requires thoughtful storage and dealer selection. But it does eliminate structural risk.

For those looking for reputable precious metals dealers, a couple we know and trust are Miles Franklin and JM Bullion. It’s important to know the dealer before buying large amounts of coins. And while we don’t receive any compensation from these dealers, we know many people have used them and have been happy with their services.

For those who prefer not to hold physical metal, silver mining companies offer another path.

Miners are operational businesses. They produce silver. And when prices rise, their revenues and margins tend to rise faster. That’s why mining equities often outperform the metal itself during sustained uptrends.

We saw this dynamic last year as the SLV ETF rose 145%, and the Global X Silver Miners ETF (SIL) rose 166%. That relationship isn’t guaranteed in the short term, but over full cycles, it has held repeatedly.

Silver is being pulled into the center of the next industrial cycle defined by artificial intelligence, electrification, and energy-intensive infrastructure. These systems don’t function without reliable electrical conduction. And silver remains one of the most efficient materials for the job.

At the same time, the supply side is constrained. Production can’t respond quickly. Inventories are being drawn down. And policy decisions are adding friction to an already fragile physical market.

That’s why volatility is elevated. And it’s why price pullbacks are being met with real demand.

The recent price fluctuations weren’t a warning sign. When forced selling hit, the market absorbed it. When leverage cleared, buyers stepped back in. That’s how markets behave when fundamentals are doing the heavy lifting.

This doesn’t mean silver will rise in a straight line. It won’t. In fact, TD Securities says $7.7 billion, or 13% of aggregate open interest in COMEX silver markets, will need to be sold in the next two weeks.

This will be another test, and if silver holds its price or bounces back quickly, it will show us it is ready for another leg higher.

Silver has become a strategic input. It’s not just a store of value, but a necessity for the technologies driving the next phase of global growth.

Markets eventually price that reality in. And when they do, it rarely happens quietly.

Regards,

Nick Rokke

Senior Analyst, The Bleeding Edge

Read the latest insights from the world of high technology.

NVIDIA has just released its Alpamayo open-source AI models for autonomous driving. But here’s why Tesla isn’t nervous…

It has taken more than 30 years to accomplish fully autonomous driving, where the passenger no longer has to...

Consumers will soon begin flocking to products and services that are intelligent… and it’s going to shake up the...