Leveraging AI for Personalized Cancer Therapies

Someone with no medical training whatsoever leveraged AI to devise a custom cancer vaccine entirely on their own, in...

We don’t know what conversations are taking place behind closed doors, but this is an interesting breadcrumb…

Jeff’s Note: Jeff here, cheers from Alaska!

After 12 months of sheer intensity after relaunching Brownstone Research a year ago, I’m enjoying a much needed “reset” with my family before we prepare to head into the next leg of intense boots-on-the-ground travel and research with Brownstone Research.

We still have a lot of work to do for our subscribers, both past and present, and I can’t wait to be back at my desk next week.

I wanted to send a big personal WELCOME to all the new readers who’ve joined us in recent weeks.

You’ve come to The Bleeding Edge, my daily e-letter where I peer into both the past and future to connect the dots on the biggest tech trends of our day.

Speaking frankly, as I’ve been told by both colleagues and readers alike – and I know it to be true: You won’t find anything like it on the market.

It’s important you whitelist us so our issues don’t suddenly end up in your spam filter. Instructions here.

I’ve asked one of my senior lead analysts, Joe Withrow, to write for you today, so that he could bring you in on the beginnings of an incredible idea we’ve been working on.

I think you’ll really enjoy this one. See you soon.

– Your Soon-to-Be-Better-Rested Editor, Jeff Brown

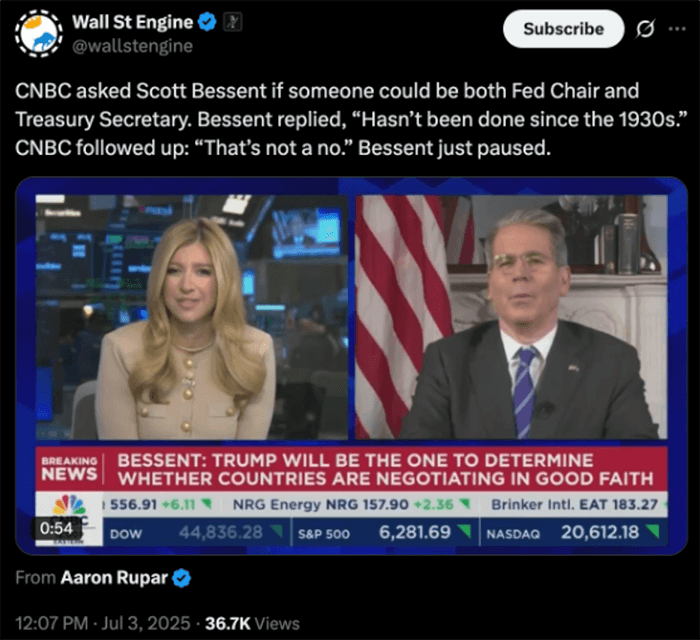

“Hasn’t been done since the 1930s,” said U.S. Treasury Secretary Scott Bessent in a recent live interview with CNBC.

The host had just asked Bessent directly if someone could be both Federal Reserve chair and the Treasury secretary in a live interview.

“That’s not a no,” the reporter quipped back in response.

Bessent paused… and didn’t elaborate further on the matter.

Source: Wall St Engine

You can intuit a lot from watching someone’s body language in conversation… and I think Bessent’s body language was telling in this interview.

Bessent could have easily shot down the idea that he could also serve as Fed chairman…

But he didn’t.

We don’t know what conversations are taking place behind closed doors, but this is an interesting breadcrumb…

The Trump Administration has been pounding the table on its desire for the Fed to cut rates.

In fact, President Trump tripled down on his attacks on Fed independence. He recently said that the Fed should cut its target rate to 1%, which is three times lower than where it is today.

Fed Chair Jerome Powell’s refusal to substantially cut rates has fueled media speculation that Trump might try to fire him.

And that prompted wide-ranging speculation about who Powell’s successor would be… spurring a rumor that it could be Treasury Secretary Scott Bessent.

Now, historically, no president has successfully removed a Fed chair mid-term, and attempting to do so would likely trigger substantial lawsuits and negative press, which would be counterproductive to Trump’s agenda.

But Trump may not need to fire Jerome Powell. Powell’s term ends on May 15, 2026. That’s only 10 months out.

Given Bessent’s comments and body language in the CNBC interview, what if Trump simply doesn’t plan to appoint a replacement for Powell next May?

What if, instead, he’s setting up a frontal assault on the Fed’s very structure?

Now, before you dismiss this idea, consider this…

Modern economists hold up an independent central bank as sacrosanct today. But that wasn’t always the case…

The Banking Act of 1935 infused the Federal Reserve with a range of centralized powers and autonomy that it did not have previously.

However, before that legislation, there was no Fed chairman. The position didn’t exist.

Instead, the Treasury Secretary led the Fed’s board and had a strong say in its monetary policy directives.

Is this what Bessent was referencing in his response to CNBC?

To understand the full context here, it’s important to understand some forgotten history…

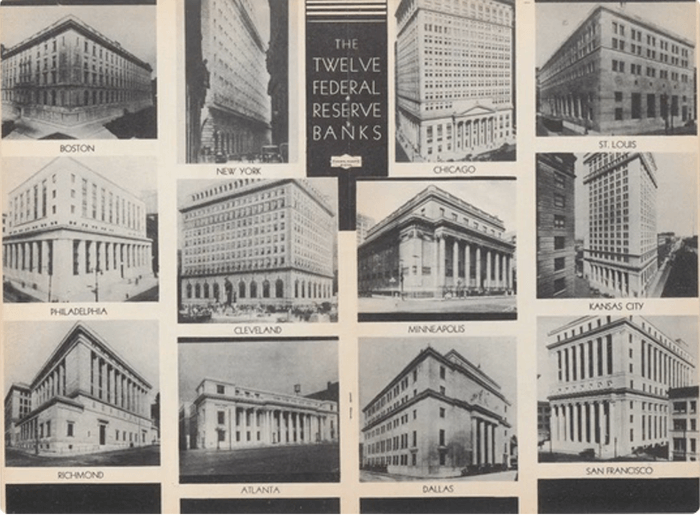

The original Fed, as originally constructed in December 1913, featured 12 regional banks – each with its own board of directors and localized autonomy.

Each of the regional boards was elected by private member banks that “owned” stock in their local Federal Reserve Bank.

These regional Fed banks set discount rates independently from one another, based on their view of the local economy in their region. This enabled them each to make credit more or less accessible to local businesses through the regional banking system.

The regional Fed banks also paid a 6% annual dividend back to the member banks that owned their stock.

Source: Newspaper clippings of the 12 regional Federal Reserve banks

The regional nature of the system created an interesting dynamic. The Federal Reserve Bank of New York might ease credit to fuel a boom on Wall Street, while the Federal Reserve Bank of Atlanta tightened monetary policy to cool cotton speculation.

Open market operations – buying bonds to inject cash into the system – were a fledgling tool and completely voluntary. Each regional bank could choose to engage in that activity – or not participate.

Meanwhile, a centralized Federal Reserve Board in Washington, D.C., was chartered with the oversight of the 12 regional banks. The Treasury secretary served as chairman of that board, which gave the administration a strong voice in how the Federal Reserve Banks conducted monetary policy at the regional level.

To be clear, the Federal Reserve Board of D.C. could not issue binding orders. It simply offered guidance and suggestions. So the regional banks maintained an element of independence. But suggestions from the Treasury Secretary often carried heavy weight.

Banking tycoon Marriner Eccles came to see this as a fatal flaw in the early 1930s. If his name sounds familiar, it’s because the Federal Reserve Board Building in Washington, D.C., is named the Eccles Building after him.

Marriner Eccles | Public Domain, Library of Congress

Historical accounts depict Eccles as a wiry man with sharp eyes and a sharper mind. He used his significant influence to lobby President Franklin Delano Roosevelt (FDR) to push legislation that would create a stronger Federal Reserve System.

The records suggest that Eccles convinced President FDR that he could solve the problems stemming from the Great Depression if only he had independent control over the country’s monetary policy.

Back in 1934, America was immersed in the Great Depression. Over 9,000 banks had shuttered over the previous few years, wiping out the savings and the hope of many American families. Unemployment hovered at 25% as economic activity slowed to a snail’s pace

This was the climate in which FDR was elected president by a landslide over Herbert Hoover. Hoover had gained a reputation as a callous proponent of laissez-faire, while FDR promised swift and bold action… and he meant it.

FDR’s “New Deal” fundamentally altered the nature of America by drastically expanding the role of the federal government in financial and economic affairs.

Overhauling the nation’s central bank was not originally part of the New Deal, but Marriner Eccles and FDR’s Treasury Secretary Henry Morgenthau made the Federal Reserve a centerpiece of reform in 1934.

By February 1935, Eccles’ plan – Title II of the Banking Act – hit Congress like a thunderclap.

In the Senate Banking Committee’s marble chamber, Senator Carter Glass fumed. Glass was a Virginia senator who had played a crucial role in shaping the Federal Reserve Act of 1913. He saw Eccles’ lobbying as a power grab that would undermine the Federal Reserve System he helped create.

As such, Glass forced weeks of haggling in the Senate over the bill. They reached a compromise in July 1935.

Glass won some concessions. The Fed would have no direct economic mandates beyond banking stability. But Eccles got the core of his plan: the creation of a Federal Open Market Committee (FOMC) to unify monetary policy and a retooled board of governors, headed by an independent chairman with final say over interest rates and operations.

The bill sailed through Congress a month later. It passed by a landslide in both the House and the Senate. Then FDR signed it into law on August 23, 1935.

FDR signs the Banking Act of 1935 – Source: Wikipedia

The Banking Act of 1935 infused the Federal Reserve with a range of independent powers that it did not originally have.

The FOMC, headed by the chairman, became the centralized governing body with full authority over discount rates and open market operations nationwide.

This marked a sharp break from the Fed system’s original structure. And it imbued the Fed with new powers and capabilities. They included:

If the Trump administration wanted to have direct influence over the Fed’s monetary policy decisions – as Trump has indicated – then rolling back the Fed to its pre-1935 structure would be a legitimate way to do so.

It would be simple to repeal the Banking Act of 1935.

My understanding is that it would take a simple majority in Congress to pass.

And Vice President J.D. Vance has already cast the tie-breaking vote in the Senate on seven separate occasions since the current administration has been in office. The political will is likely there.

So there is a clear legislative path toward removing the Fed’s independence. The question is – would it be practical?

We know that the current administration plans to institute major economic changes. And the fact that Treasury Secretary Scott Bessent played coy about the possibility of also running the Federal Reserve suggests that these kinds of conversations are happening.

Then, if we look at the recently passed GENIUS Act and the nature of stablecoins, it’s clear that they will shift a large degree of oversight and regulatory power away from the Fed and to the Treasury.

As a reminder, stablecoins are blockchain-based digital assets that are 100% backed by liquid assets like U.S. Treasury bills.

Stablecoins are held outside of traditional bank deposits, which takes them out of the Federal Reserve’s purview. This will reduce the impact of the Fed’s conventional monetary tools over time, as more cash moves out of deposits and into stablecoins.

What’s more, the GENIUS Act empowers the Treasury to grant exemptions, coordinate enforcement, and respond rapidly to emergencies – often with minimal Fed involvement. This will facilitate faster, more direct Treasury influence over digital money markets.

So the rise of stablecoins will gradually reduce the Fed’s structural place within the U.S. economy.

And we should note that stablecoin issuers will almost certainly become the largest holders of U.S. Treasury bills worldwide. In fact, Tether (USDT) already holds more Treasurys than Germany.

(Everything I’m discussing here has to do with a project Jeff is calling “Project MAFA,” and it’s coming quickly. Just last week, President Trump signed the GENIUS Act into law, and this is huge news. It’s the green light “Big Money” has been waiting for, since it paves the way for up to $3.7 trillion to hit the stablecoin market. If you have not yet watched Jeff’s presentation on this fast-moving story, I highly encourage you to do so here.)

Given that the Treasury needs to roll over $9.2 trillion in debt this year and trillions more a year in 2026 and 2027, there’s no question that the Trump administration will encourage the rapid adoption and integration of stablecoins.

Putting it all together, we have to ask – what if President Trump’s public attack on Jerome Powell is sowing the seeds for a bigger play?

What if the true goal isn’t simply to cut short-term rates aggressively… but to set the stage for rolling back the Fed’s independence – so that the Treasury can reassert influence over monetary policy for the first time since 1935?

Watching this story unfold will be interesting to say the least. And my takeaway is this…

The Trump administration sees lower interest rates as critical to its economic plan. So one way or another, short-term rates are going to fall dramatically within the next 12-18 months.

When that happens, we’ll likely see institutional money flow into the equity markets – driving valuation multiples up in the process.

Our readers at Brownstone Research will be ready.

So let’s buckle up. We’re in for a wild ride…

– Joe Withrow, Senior Analyst, Exponential Tech Investor, Brownstone Research

Read the latest insights from the world of high technology.

Someone with no medical training whatsoever leveraged AI to devise a custom cancer vaccine entirely on their own, in...

If NVIDIA hits the scale Jensen Huang is signaling, we’re no longer talking about incremental growth in data center...

When Elon Musk stated he wanted to build his own semiconductor manufacturing plant, many assumed he was just bluffing…

Thanks for signing up for The Bleeding Edge — we’re glad you’re here!

Want updates sent straight to your phone too? Sign up for SMS alerts to get the latest delivered via text.

Brownstone Research: By submitting your phone number, you agree to our SMS Terms & Conditions, Terms of Use, & Privacy Policy, and give express written consent to receive marketing text messages from BSR. Messages are recurring & frequency may vary. Reply STOP to 94703 to opt out. Reply HELP to 94703 for info. Consent is not a condition of purchase. Message and data rates may apply. For additional information, you may contact Customer Service at 888-512-0726 or smssupport@brownstoneresearch.com.