IPOs Are a Boom for Crypto

The trend of tokenized stocks coming onchain is not some pie-in-the-sky imagining of the future…

Blockchains are undercutting credit card companies. Layer 2 solutions like Base or Arbitrum are settling transactions for tiny fractions of a penny.

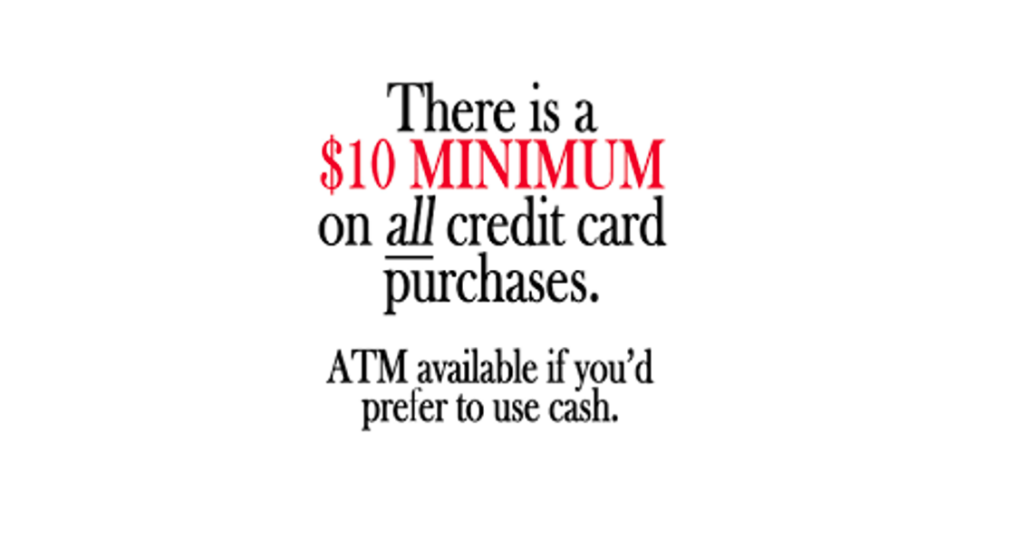

You walk into a convenience store to buy a bottle of water.

At the checkout counter, you take out your credit card without a second thought. Then, the cashier points to the sign:

Source: Facebook.com

We’ve all been there. It feels like a trap since not many people carry cash on hand anymore.

But credit card minimums exist for a simple reason: Merchants are bogged down with fees whenever a credit card gets used. This includes interchange fees, assessment fees, or processor markups. The formula is dizzying — card provider, issuing bank, payment processor, and more.

To simply get over this floor of fees and not eat into the margin on the items in the store, each sale needs to be a certain size. A pack of gum or bottle of water isn’t going to move the needle as the fees will surely eat into the merchant’s profit.

We can call this burden the “card fee floor.”

And as I’ll show you in just a moment, credit card companies are about to be undercut…

x402 is a protocol for seamless payments over the internet.

We wrote about it in The Forgotten Code shortly after its release last year. It’s an open-source release that’ll redefine how we think of payments.

That’s because when we book a flight or pay for something online, we often hand over card details and fill in our personal information.

x402 can handle payments without creating an account. It’s a solution that encourages micropayments since it does instant settlement, has no fees, and is secure. It’s often referred to as the payment rails for AI agents.

It’s also alluding to something bigger. And to understand what, let’s go back to the card fee floor.

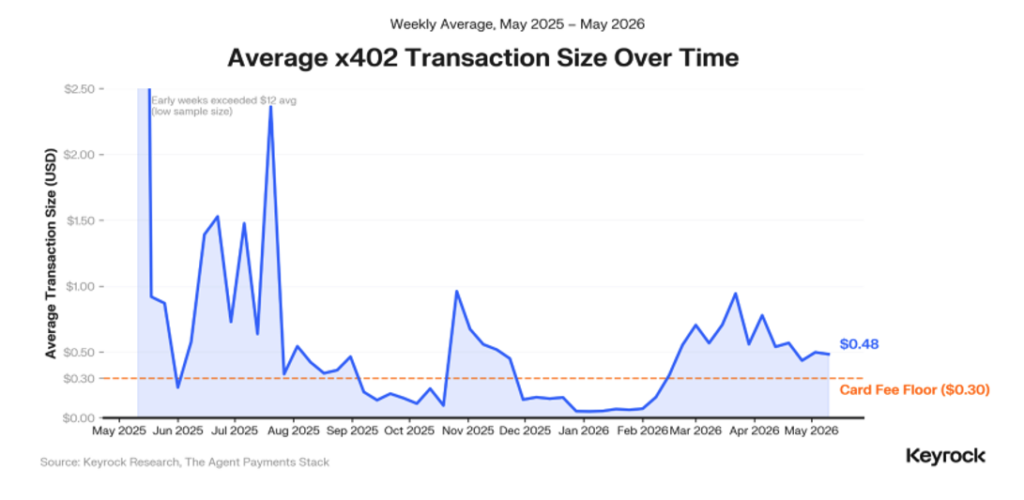

A report published last week by Keyrock titled “Who Pays the Agent? The Race for Frictionless Machine Payments” pegged the card fee floor at $0.30.

Anything priced below that amount—or a product with a profit margin less than that—is a no-go for merchants to accept a credit card. They’d lose money.

But the report did something else important. It tracked payment activity over the x402 protocol since May 2025.

And what they discovered was the median payment by agents using x402 was between $0.01 and $0.10.

Said differently, 76% of agent transactions were below the card fee floor.

This was based upon 176 million transactions with $73 million settled.

That alone is remarkable…

Just over a year ago, these figures were essentially zero. x402 was just being deployed. And the idea of AI agents making economic transactions felt more theoretical than practical.

But here we are…

Agents are conducting microtransactions. And what’s more interesting…

They’re not using traditional credit cards. The agents prefer using stablecoins on public blockchains.

Circle is the company behind the U.S. stablecoin, USDC. The CEO, Jeremy Allaire, has been predicting billions of agents will operate with stablecoins on users’ behalf within three to five years.

Jeremy seems to know something most don’t.

That’s because AI agent payments were almost entirely done in stablecoins. And of those, 98.6% of payments were using Jeremy’s USDC stablecoin.

USDC is becoming the default settlement asset of the agentic economy.

That’s important when we consider this quote from the Keyrock report:

Stablecoins won the settlement layer for machine commerce almost by default; they were the only instrument that could handle sub-dollar transactions without the economics collapsing.

Which gets us to the most important part of this trend…

Blockchains are undercutting credit card companies. Layer 2 solutions like Base or Arbitrum are settling transactions for tiny fractions of a penny.

That’s why the more than 104,000 agents registered across various directories and registries in the digital asset ecosystem are using blockchains and stablecoins.

The trend is early, but credit card companies are not sitting idle.

Stripe is one of the most successful payment providers for the internet.

Its success comes from a developer-friendly platform that lets anyone integrate secure payments with just a few lines of code.

That puts x402 squarely in Stripe’s path. If agents adopt it, Stripe loses meaningful share of internet payments.

Management understands that.

With the help of venture capital firm Paradigm and Visa, Stripe developed a payments-focused blockchain called Tempo.

And one of the first announcements they made after launching mainnet was a new open standard for AI agent payments – Machine Payments Protocol (MPP). It’s a solution like x402.

But each has its specific use cases.

MPP is best for usage-based billing — ongoing services like compute or data streams.

x402, on the other hand, is best for per-API-call or small data payments — true micropayments.

Which means there’s not likely to be just one winner.

In fact, even Google is building in this space with its Agent Payments Protocol (AP2). It too is an open-source standard. Google collaborated with PayPal and Mastercard on the project.

The ideal use case for AP2 is agents that can act with delegated budgets. It’s a solution that would allow an agent to make transactions on a human’s behalf…but with guardrails.

Some of these solutions can be mixed and matched. That means there likely won’t just be one winner. Instead, expect a future of varied combinations.

But no matter what…

Expect the winner to offer the least friction. And right now, that looks to be permissionless, public blockchain solutions. One of those solutions happens to be our most recent recommendation in Permissionless Investor this month.

More on the permissionless agentic economy soon…

Your Pulse on Crypto,

Ben Lilly

Editor, Chain of Thought

Read the latest insights from the world of high technology.

The trend of tokenized stocks coming onchain is not some pie-in-the-sky imagining of the future…

Whoever controls the information controls the market. Here’s how the CLARITY Act could upend Wall Street’s control…