How a Banned Chat App Is Beating India’s Internet Shutdown – and What It Means for CLARITY Act

India's internet shutdown couldn't stop the Cockroach protests – thanks to a decentralized chat app with no internet required....

Vitalik’s post on June 1 is worth taking seriously. It’ll likely lead to the next unicorn in DeFi.

Vitalik Buterin is the most influential developer in the digital asset ecosystem.

He’s the co-founder and one of the main developers and architects behind the Ethereum blockchain. When he proposes an idea, an army of developers races to put forward a design.

And history has shown this is well worth the effort.

The most noteworthy example of this was ten years ago, tucked away in a Reddit forum. He proposed an onchain decentralized exchange (DEX) where users can easily swap between two tokens.

Source: Reddit.com

A recently laid off 24-year-old mechanical engineer from Siemens with no formal programming background stumbled across Vitalik’s post in the summer of 2017.

On November 2, 2018, Uniswap v1 launched. And soon after, a Cambrian explosion of decentralized finance (DeFi) protocols emerged thanks to Uniswap.

Many often credit Uniswap as being the birth of DeFi even though other protocols such as Aave (formerly known as EthLend) and Sky (formerly known as MakerDAO) were already operational in 2017.

But Uniswap’s success was almost guaranteed given the idea was born via Vitalik’s post.

In fact, Buterin reviewed the codebase himself while the project was in development. And then advised him to apply for an Ethereum Foundation grant for funding.

The project is now home to nearly $3 billion in assets with current monthly volume at $43 billion. It spans 46 chains and even has its own layer-two chain, Unichain. The entire market has been playing catch up to Uniswap ever since.

The story shows that when Vitalik pitches a new idea, it’s worth taking seriously.

And that’s why Vitalik’s post on June 1 is worth taking seriously. It’ll likely lead to the next unicorn in DeFi.

The title of his post was “Building index-tracking assets on top of options instead of debt”.

If you want to read it yourself, you can find it on the ethresear.ch site here. But allow me to give you the highlights.

The short version is, without explicitly saying it, he’s advocating for a way to build synthetic assets that don’t rely on liquidations. We can think of these assets like stablecoins that already exist such as DAI and USDS.

Instead of relying on loans and liquidations to remain solvent, the system relies on an options market.

The result…

A system that is no longer dependent on real-time oracles – a piece of infrastructure that tells a smart contract the price of an asset at any given time.

The reason this is important is that real-time oracles are a central point of failure. If the oracle reports an incorrect price or fails to update during fast markets, positions get liquidated automatically, often during the moments when liquidity is thinnest and prices are least reliable.

Buterin’s proposal sidesteps the problem by splitting 1 ETH into two complementary tokens, which he calls P and N.

P is structurally equivalent to a cash-secured short put: it pays out a fixed dollar amount up to a chosen strike price. N is the call side: it captures any upside above the strike. The two always sum to exactly 1 ETH of collateral.

Which is to say, the system can never become undercollateralized. There is nothing to liquidate, ever.

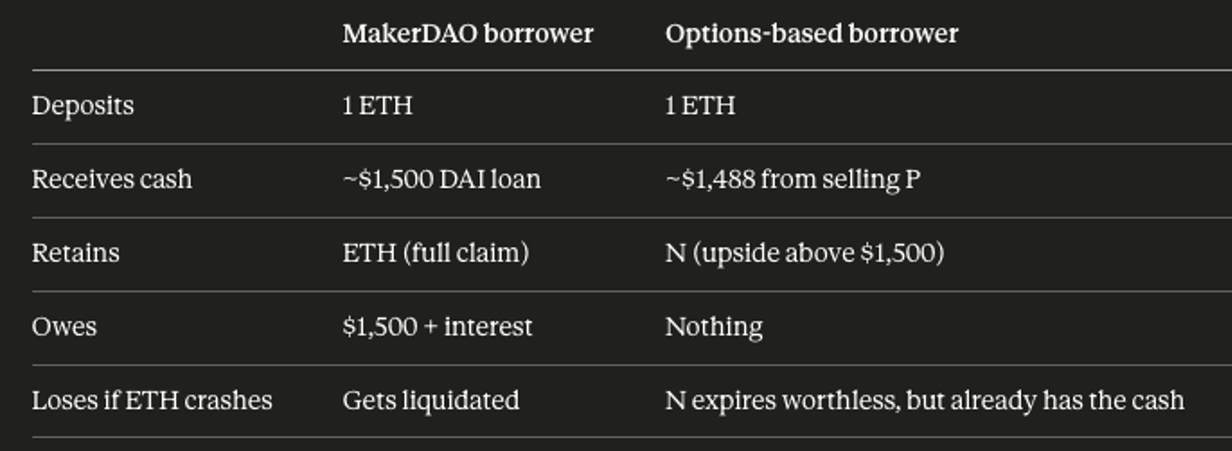

If a user wants to extract cash against their ETH similar to the way a borrower would on Sky (formerly MakerDAO), they split their ETH into P and N and sell the P side for stablecoins. Here’s a helpful diagram that compares the two methods.

Source: Claude.ai

There’s no debt, no interest rate, and no margin call. Compensation to the buyer of P is baked into a one-time discount on the purchase price rather than collected as interest over time.

The main idea here is that this P/N split is a prediction market. One that resolves to a binary yes-or-no outcome like we see with Polymarket.

It’s absolutely an innovative idea.

And it’s 100% an idea worth exploring. We can be sure there will be plenty in the industry that will go ahead and build protocols around this and we should expect to see usage…

That’s because the financial structure isn’t new.

Banks already run multibillion-dollar books on the same payoff. Again, the novelty isn’t the instrument. It’s the prediction market and the removal of oracles from the design.

And history has proven that if a developer pushes a Vitalik idea to market, they are likely to gain his support, the Ethereum Foundation’s support, and support from the wider community.

Some are already giving it a shot…in a way.

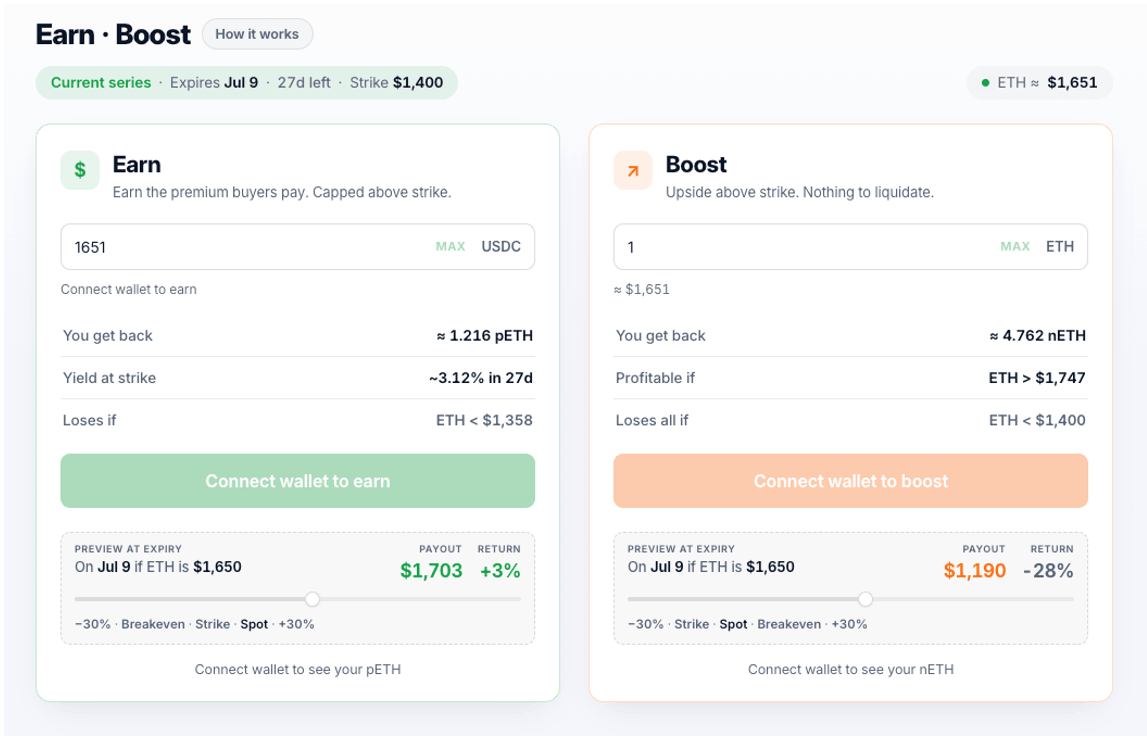

The first one I’ve seen thus far is Cleave market. It’s merely in testnet, but you can see the setup here.

Source: Cleave.market

The user interface looks like a simplified options market order.

Not a solution for a borrower.

Which is why I don’t think this is the end state Vitalik is thinking about, even though he recently shared this specific project in a tweet posted on June 11.

The end goal likely needs to abstract away the need to understand how options work. And I think that’s the biggest design hurdle for any developer to overcome— How to make the experience feel as simple as pledging collateral or assets and borrowing a stablecoin.

Which is where we can almost expect this design space to go towards – a stablecoin.

This is where this idea will likely lead.

But without getting too off track, I’d like to be honest about what will happen to lending and borrowing markets…

The idea behind Vitalik’s post was to bring a better lending and borrowing solution to market. One that avoids cascading liquidations and dependency on oracles.

Which is to say, a more resilient ecosystem.

And the knee-jerk reaction is that lending and borrowing protocols such as Aave, Compound, Morpho, Euler, and others might be under the gun to innovate with this new design.

But I don’t think so…

One of the biggest draws of borrowing against collateral is the collateral can rise in value while you unlock value from the asset for however long you need it for. And then slowly repay the interest using the base asset.

This is already common among high-net-worth individuals with large stock holdings. They borrow against those positions. Then, as the stock rises, they have the ability to sell smaller and smaller chunks of stock to service and ultimately repay the loan.

The options idea proposed by Vitalik does not maintain this. Instead, it has a maturity date. The borrower must roll into a fresh contract every cycle, which means slippage and no set-it-and-forget-it mode.

The main users of these loans are not looking to manage option strikes, expirations, and rolls. They simply want a button that gives them dollars and another button that gives them their collateral back once their loan is finished.

Which is to say, a lot more work needs to be done before we need to worry about the state of lending protocols.

But from what I’ve seen so far, it’s an intriguing idea…with one serious drawback that needs addressing.

More to come.

Your Pulse on Crypto,

Ben Lilly

Editor, Chain of Thought

Read the latest insights from the world of high technology.

India's internet shutdown couldn't stop the Cockroach protests – thanks to a decentralized chat app with no internet required....

The endorsements for the CLARITY Act are building. The plan of action is forming. We’re getting closer to a...

There’s a lot on the Senate’s plate right now. Thune will decide if the CLARITY Act gets priority…