The Iran Oil Shock: Why Market Fear May Be Setting Up the Next Rally

Over the past week, the conflict with Iran has escalated dramatically. And the most critical chokepoint in the global...

We’re in for some incredible breakthroughs in just the next six to eight months. What’s coming is just unbelievable…

This was a big week in the world of artificial intelligence (AI).

The industry proxy, NVIDIA (NVDA), held its quarterly earnings announcement. As always, it was closely watched to determine if there is, or isn’t, a slowdown in AI.

And the numbers were clear. It’s full steam ahead:

NVIDIA is now a $4.2 trillion company and the most valuable company in the world. And despite its size, it continues to demonstrate the kind of year-on-year growth numbers that we would typically only see in a smaller capitalization company. That’s how powerful this trend is.

Dell (DELL) also reported earnings this week. It is one of the largest providers of AI servers to the industry, and its numbers echoed the same growth:

This is just crazy growth for companies of this size. We’re living through a hyper-acceleration period right now, and the incredible part is that we’re closer to the beginning than the end of the acceleration. There is so much more ahead of us, and once the impact of artificial general intelligence (AGI) kicks in, it will only accelerate.

We’re going to have to hold on tight for the ride.

Jeff

Hi Jeff,

Some time ago, you provided us with a list of cryptocurrencies we should consider to be well-positioned for the coming [decentralized finance] DeFi future. I bit and moved $12k from my Fidelity IRA to a crypto IRA at iTrust Capital. That account is now up nearly 59% – sweet!

I’ve been hearing about staking, but haven’t looked into it, as I don’t know enough and don’t care to risk my assets without guidance. Do you think you could address this concept with some pros and cons in a future letter? I’d love to get your take on the concept. Thanks!

– Gary D.

Big reader of Jeff Brown, great to hear he is doing better, wish him and Brownstone Research the very best. Thank you, my wife and I are doing great with your recommendations over the years.

We have held Uniswap (UNI) on Coinbase since 2020, up 250% and it is not offering staking. How can I get positioned in the gig of staking UNI? Would love to see those high yields you mentioned. Thank you so much, and please convey our best regards to Jeff.

God Bless you all at Brownstone Research!

– Anthony G.

Hello Gary and Anthony,

Great to hear from you, and I’m glad you asked about staking.

We’ve been thinking a lot about staking recently at Brownstone Research. It’s a very different investment strategy, and with digital assets, not every asset stakes in the same way. And for some assets, you have to perform a multi-step process to stake your asset to earn yield.

Because of these differences, we’ve been thinking about whether or not to launch a research service focused entirely on staking digital assets. If anyone thinks that’s a great idea, we’d love to hear from you.

There are a lot of nuances to staking in the industry, so each digital asset needs to be considered individually.

It’s a powerful strategy for high-quality digital assets or high-growth digital assets. In exchange for staking your digital asset and providing liquidity, you can earn a yield for the service that you’re providing. Sometimes that is a few percent, other times it can be north of 40% annually.

And, of course, if the value of the underlying asset that you are staking increases in value while you are staking that asset, the value of your original staked value and the value of the earned yield experience capital appreciation. These are the pros of staking.

The downside is the opposite, of course. If the value of the asset that is staked drops dramatically, then the value of the staked assets depreciates, and the amount could be greater than the earned yield for staking.

Some staking requires the assets to be locked up for a certain period of time. For example, three months, or even a year… kind of like a certificate of deposit (CD). In this case, there is no liquidity, and an investor is exposed to duration risk.

These are the cons to staking. That’s why dedicated research on each asset and its associated staking opportunity is so important.

As for Uniswap, Ben and I worked on an issue of The Bleeding Edge earlier this month, The Crypto Exchange Leading the Blockchain Onshoring Effort. This provides some important context on Uniswap.

Once Uniswap has established its DUNI, it will become “fee switch” activated, allowing users to stake UNI and earn yield. We fully expect that this will be simple to do and available on Coinbase at a minimum.

There is a way today for self-directed investors to provide liquidity to a pool by staking a pair of tokens. For example, you can stake a USDC/ETH pair and receive liquidity provider tokens for staking the pair. You are “paid” for providing liquidity on Uniswap as a decentralized exchange.

Many of the larger digital assets, like ETH and Solana, are easy to stake, and they earn yield way beyond what we get from our banks in U.S. dollars. An easy way to think about it is that we are staking U.S. dollars at our banks to provide the bank liquidity.

How much is the bank paying us for providing liquidity? Almost nothing. It’s a joke. For example, Citibank offers its savings accounts at a standard rate of 0.03% for savings deposits. Unbelievable.

And it is earning 4.33% from the Federal Reserve’s overnight rate. The banks take our money, earn 4.33%, and give us 0.03%. It’s just not right.

Compare this to Coinbase, which is currently offering a 1.86% yield for staking Ethereum. Coinbase’s offering is 62 times better than what an average bank is providing for “staking” U.S. dollars.

Hopefully, this provides some useful context about staking. This is a very exciting investment strategy, especially in a high-growth asset class like digital assets.

To whom this may concern:

I heard that Starlink (Elon Musk) is about to go public. When? What\’s the ticker symbol? How can I invest before they go public? I understand that there\’s a way to get in before IPO.

Thanks so much.– Perfecto B.

Ciao Perfecto,

I remember back in 2022 when SpaceX CEO Elon Musk suggested that an IPO of Starlink wouldn’t happen until 2025 or later. His remarks were made at an all-hands meeting at SpaceX.

It was those comments, combined with the incredible success that Starlink has achieved during the last three years, that resulted in rumors and speculation that a Starlink IPO is imminent.

For perspective, it’s worth understanding SpaceX’s entire business and how important Starlink is to its success. While SpaceX is still a private company, Musk has been public about projected company revenues for 2025 of around $15.5 billion.

I think most of us will be surprised to learn that only about $1.1 billion of that projected revenue comes from contracted services that SpaceX is delivering for NASA.

Contrary to what some of the media have said, SpaceX is not being “funded” by NASA, nor is it receiving grants or subsidies from NASA. The reality is that because SpaceX’s launch costs are so low, SpaceX is saving NASA billions in costs, and in some cases is literally the only company capable of providing certain services to NASA.

The most ironic part is that SpaceX could charge significantly more for its services and still be the cheapest, safest, most efficient launch provider in the world. What most don’t understand is that SpaceX’s guiding mission is to make the human race a multiplanetary species, and to do so, it needs to achieve incredible scale.

We explored this concept in Wednesday’s Bleeding Edge – The Answer to Life – 42. Musk’s target is to manufacture more than 1,000 Starships a year, a mindboggling number, and also practical if the goal is to build a self-sustaining civilization on Mars.

With great scale comes dramatically lower costs per launch. That’s why SpaceX isn’t charging higher prices. Lower prices drive higher utilization, which allows SpaceX to scale more quickly.

This context is quite important to address your question. We have to think with the mindset of how Musk is looking at his overall business.

Starlink’s revenues for this year will likely fall into the range of $12.3 billion–12.8 billion, which will be roughly 80% of SpaceX’s total revenues. Arguably more important than the top-line revenue number is that Starlink, as a standalone business, reached free cash flow breakeven in the fourth quarter of 2023 and is expected to generate more than $2 billion of free cash flow this year.

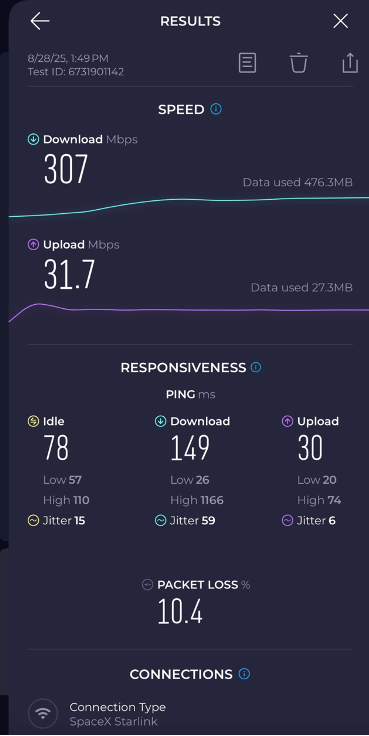

This July, Starlink announced that it had reached 7 million subscribers in about 150 countries/territories. Starlink currently has almost 8,100 operational satellites in orbit right now delivering unbelievable performance. Below is a screenshot of a speed test on a United flight delivering speeds above 300 Mbps.

I’ve experienced the service myself on several flights. The performance is just incredible. Basically indiscernible from a broadband service to the home, all from an altitude of 550 kilometers.

This is a long way of saying that Musk and SpaceX have an incredibly valuable asset that is growing like crazy, and it’s throwing off billions in free cash flow. Cash flow that is necessary to fund the aggressive development of the Starship.

While SpaceX would generate a lot of capital by spinning out Starlink in an IPO, my guess is that in the short term, Musk would prefer to keep Starlink in-house as the cash cow for SpaceX to fund Starship development. Therefore, I don’t believe that Starlink will have an IPO this year.

I’m speculating here, but I believe Musk will wait until Starship reaches certain milestones and SpaceX itself is generating free cash flow from launch operations and other contracts outside of Starlink. That means that the earliest window would likely be the fall of 2026 for a possible IPO.

There is currently no way for self-directed investors to invest in Starlink directly ahead of an IPO. And only accredited investors or qualified purchasers can acquire shares in SpaceX directly in the secondary markets. I expect that those who own shares in SpaceX directly would receive shares in Starlink in the event of an IPO.

I wish I had better news, but we’re going to have to be patient.

Good Evening, Jeff and Team,

Thank you for all the incredible research you do! Your ability to explain complex tech subjects to “non-engineers” is truly amazing.

I read your recent answer about powering AI data centers, and I am wondering: why exactly do AI data centers require so much energy?

A light bulb creates light, a microwave heats my food, a water pump pushes water to shower me, but what specifically makes the AI data center so “power hungry,” and what does all that power actually do?

I am sure that the answer is complex, but (assuming that the above questions make any sense), how do the AI data center’s power needs and performance compare to that of the human brain, which is estimated to operate on just about 20-30 watts?

And what will happen to all that power (and data centers themselves) when AI models become small enough to run on cell phones?

I would greatly appreciate your thoughts on these questions.

Thank you again for your research, and have a great weekend!

– Anton L.

Hello Anton,

Your question is a bit paradoxical, and definitely one that conceptually is hard to grasp because of the scale involved.

If we listen to most semiconductor companies or consumer electronics companies that release new products every year, like Apple, we’ll always hear about improvements in power efficiency or battery consumption. The stats are always positioned in a way to make us think that improved power efficiency will result in less power consumption.

Yet exactly the opposite is true.

What they are really referring to is that each successive generation of semiconductor technology provides for reduced power consumption per unit of compute. What they intentionally leave out is that the software becomes more complex and computationally more intensive, requiring higher levels of power consumption.

And with regards to semiconductors, as power consumption declines per unit of compute, operational costs per unit of compute decline. This is precisely why there is such an incessant need to develop the most advanced artificial intelligence technology on the most advanced semiconductors.

Developing frontier AI models is the most computationally intense task that has ever been performed by industry. That’s why the scale of these data centers is so massive. Below is a recent photo of just the first phase of the Stargate AI data center in Abilene, Texas.

Stargate in Abilene, TX

The Abilene site above is 875 acres, which is the size of almost 500 football fields. These AI factories will house millions of GPUs that run around the clock. It’s the sheer scale of these facilities that is driving the energy consumption. This is why gigawatt-scale energy production is needed.

And the power requirements only increase as we climb higher towards general intelligence. Achieving artificial general intelligence will require at least 1 million GPUs and 1 gigawatt of electricity. And achieving artificial super intelligence (ASI) will probably require 100 million GPUs and 100 gigawatts of electricity. The numbers are mindboggling.

But your instincts are not wrong. Once these models are trained and optimized, they will become “lighter” and require less electricity to run – that’s the inference. And that’s also the paradox, specifically Jevons’ Paradox.

As the cost per unit of inference continues to decline and the utility of AI continues to increase, adoption will accelerate on a continued exponential growth curve.

Said another way, while cost per query declines, the total number of queries using AI will grow exponentially, which will require even more electricity production.

This is why energy production is the bottleneck. It must scale as quickly as possible. And AI can actually help solve the problem, as it is critical to the development of limitless clean energy sources like nuclear fusion – the power of the sun.

We’re in for some incredible breakthroughs in just the next six to eight months. What’s coming is just unbelievable.

That’s all for today’s AMA. Thank you to everyone for writing in. As always, you can reach my team and me right here if you have a question for a future AMA issue.

Have a great weekend.

Jeff

Read the latest insights from the world of high technology.

Over the past week, the conflict with Iran has escalated dramatically. And the most critical chokepoint in the global...

Private investment rounds like this are illiquid. It’s not trading, it’s an investment. This is a sign of what’s...

If you know what to look for, it’s actually pretty easy to find the fakers.

Thanks for signing up for The Bleeding Edge — we’re glad you’re here!

Want updates sent straight to your phone too? Sign up for SMS alerts to get the latest delivered via text.

Brownstone Research: By submitting your phone number, you agree to our SMS Terms & Conditions, Terms of Use, & Privacy Policy, and give express written consent to receive marketing text messages from BSR. Messages are recurring & frequency may vary. Reply STOP to 94703 to opt out. Reply HELP to 94703 for info. Consent is not a condition of purchase. Message and data rates may apply. For additional information, you may contact Customer Service at 888-512-0726 or smssupport@brownstoneresearch.com.