The AI Standards Body That Shouldn’t Exist

Imagine if a small number of elites – with tight coordination with the U.S. government – had a chokehold...

While SpaceX has been building operational Orbital Web Services, Amazon has been resting comfortably, sleeping in every day, on its terrestrial Amazon Web Services (AWS).

As the old saying goes… You snooze, you lose.

Last September, Elon Musk and his team at SpaceX caught the industry off guard when they announced they had acquired the AWS-4 and H-block spectrum from EchoStar (SATS) for $17 billion.

To most onlookers, it came as a surprise.

After all, SpaceX is an aerospace company, most well-known for the success of its reusable rockets and its Starlink space-based satellite internet service. What does it need the spectrum for?

The deal was also unusual as it was structured in both cash and stock, with EchoStar to receive $8.5 billion in cash and $8.5 billion in SpaceX stock. There is even a provision in the deal for SpaceX to pay an additional $2 billion in cash of EchoStar’s future interest payments on its $30 billion plus debt load through November 2027.

Clearly, EchoStar had something that Musk wanted…

And it didn’t end there.

We were on top of SpaceX’s initial move to acquire EchoStar’s spectrum in The Bleeding Edge – The Road to SpaceX Mobile in September 2025…

Then, about two months after the purchase, Musk stepped in again to spend an additional $2.6 billion in SpaceX stock for EchoStar’s unpaired AWS-3 licenses.

AWS-3 and AWS-4 are blocks of spectrum for what the Federal Communications Commission (FCC) calls Advanced Wireless Services (not to be confused with Amazon Web Services).

SpaceX wanted that spectrum, as well as the H-block spectrum, to provision direct-to-cell (D2C) or direct-to-device (DTD) services.

The rub – and the part that no one is talking about – is the spectrum itself.

The spectrum that SpaceX bought is a paired frequency division duplex (FDD) spectrum ideal for two-way communications, and the lower frequencies provide excellent propagation characteristics, which translate directly into large performance advantages.

This acquisition is part of SpaceX’s strategy to dominate an entirely new industry that I’ve been calling Orbital Web Services (OWS).

This includes SpaceX’s Starlink offering, orbital AI data center satellite constellation, orbital internet backbone infrastructure, and direct-to-cell capabilities that are already in operation in 32 countries right now across 35 different wireless operators.

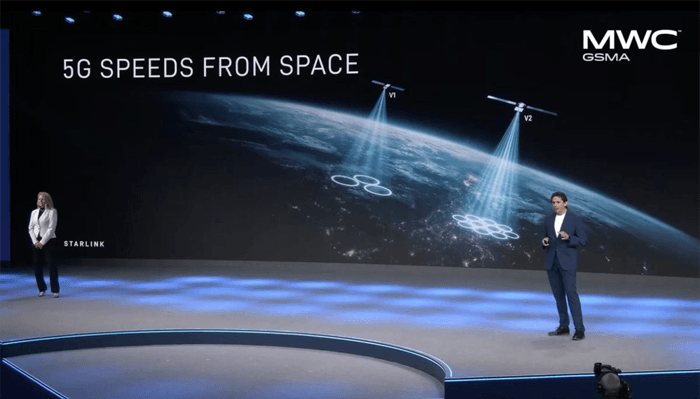

SpaceX Presenting at Mobile World Congress, March 2026 | Source: SpaceX

Early this year, SpaceX rebranded its direct-to-cell service as Starlink Mobile. The new name is telling…

The first generation of its Starlink Mobile service is already deployed with over 650 dedicated satellites launched to support this capability.

During the company’s presentation at Mobile World Congress in Barcelona earlier this year, it announced its second generation of Starlink Mobile, which will be deployed in 2027 and exhibit performance on the low end of 5G capabilities from space, around 150 Mbps.

This wouldn’t have been possible without the acquisition of spectrum from EchoStar.

What SpaceX will build with its second-generation Starlink Mobile is incredible.

It currently positions itself as partnering with mobile network operators around the world, providing emergency coverage for mobile phones that are outside the range of terrestrial mobile networks.

But it’s a bit more than that, actually.

Starlink Mobile won’t work indoors, and the user needs to have a pretty clear line of sight to a satellite outside… but once its second-generation service is deployed in 2027, it is reasonable for SpaceX to become a global mobile network operator. It would be the world’s first of its kind using normal production smartphones like iPhones and Android-based phones.

Users can pair their indoor wireless connectivity over Wi-Fi networks with Starlink Mobile’s outdoor coverage, and they theoretically won’t need to pay exorbitant costs for a terrestrial wireless phone subscription on the major network operators like T-Mobile, Verizon, and AT&T in the U.S.

And it doesn’t take much imagination to envision a tight integration with Tesla’s in-car networking to extend the coverage to in-car mobile service while driving. And if there is one thing I’m sure of, it’s that Musk and SpaceX are designing their master plan in a way to drive costs down and expand the size of the addressable market.

Just imagine what it will be like when you can switch to Starlink Mobile and your monthly wireless phone bill is cut in half.

I’d make the jump in a second.

Noticeably caught snoozing in all of this are Jeff Bezos and the team at Amazon (AMZN). While SpaceX has been building operational Orbital Web Services, Amazon has been resting comfortably, sleeping in every day, on its terrestrial Amazon Web Services.

And yet, Amazon is precisely the company that we’d think would have been a first mover into orbital web services, especially given its founder’s heavy investment in Blue Origin.

One thing is for sure… Bezos and Amazon are awake now.

Amazon just announced an $11 billion deal to acquire satellite services company Globalstar outright.

Unlike SpaceX, which simply carved out the spectrum from EchoStar, Amazon bought the whole thing. The spectrum, the satellites, the terrestrial infrastructure, and Globalstar’s deal with Apple for direct-to-cell services. All of it.

Globalstar (GSAT) was an ugly business. It hadn’t seen a profit since 2006, and it struggled to generate any meaningful free cash flow in most years. Worse, it just didn’t have the capital to invest and pursue any grand ambition.

In 2023, Globalstar brought in Paul Jacobs to become the CEO to turn the company around.

I worked with Paul at Qualcomm. He became the CEO of Qualcomm shortly after I joined the company in early 2005. When he took over at Globalstar, all I could think of was that he was brought in to sell the company.

EchoStar was an even more heavily indebted and messy company before the SpaceX spectrum acquisition, so it was no surprise that SpaceX had no interest in acquiring the entire company.

Both companies held one extremely valuable asset, and the boards of both companies knew it… spectrum. All they had to do was keep the businesses alive long enough to receive a big offer for the spectrum, and that’s exactly what happened to both.

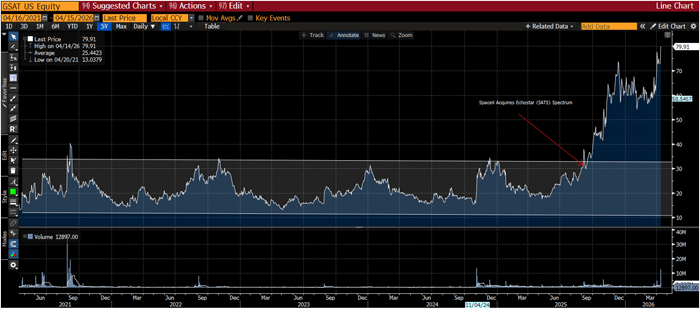

Just look at what happened to Globalstar’s share price after SpaceX announced its spectrum acquisition from EchoStar…

5-Year Chart of Globalstar (GSAT)

Amazon’s acquisition of Globalstar is a scrambling effort to catch up to SpaceX’s orbital web services. It basically had no choice if it wanted any shot at competing with SpaceX.

The media is proclaiming that the acquisition is a bold move and will put Amazon on a competitive level with SpaceX, but they just don’t understand what Amazon bought and how far behind it is compared to SpaceX.

As a reminder, SpaceX acquired 50 MHz of paired FDD spectrum, which is ideal for two-way communications.

Amazon, on the other hand, ended up purchasing much higher-frequency spectrum in the 2,483.5–2,495 MHz S-band spectrum. It’s only 11.5 MHz of spectrum that operates using time division duplex (TDD) – technology where uplink and downlink share the same frequencies over time – which is unlike SpaceX’s FDD spectrum that allows simultaneous two-way communications akin to terrestrial mobile networks.

Put simply, Amazon’s TDD spectrum has significantly limited data rates and spectral efficiency compared to SpaceX’s spectrum.

Put even more simply, there is no way that Amazon can deliver anywhere near the performance of SpaceX with the spectrum it purchased. It comes down to the laws of physics. Amazon’s hands are tied.

But Amazon didn’t have a choice. It had been snoozing, and it missed out on the opportunity to acquire EchoStar’s spectrum last year. It should have moved first.

Globalstar was the next best option. But SpaceX’s spectrum is like the prime spectrum real estate. Amazon is left with the scraps.

The worst part is that Amazon ended up paying more than SpaceX on a per MHz basis. SpaceX paid about $340 million per MHz on its initial deal. Amazon ended up paying about $1 billion per MHz because it snoozed.

Ouch.

Paul Jacobs, due to his past experience at Qualcomm, knows the value of spectrum. As CEO of Globalstar, he knew that Amazon didn’t have a choice. And he negotiated an incredible price for Globalstar. Big win.

Small space-tech companies like AST SpaceMobile (ASTS) and private company Lynk are now going to have a difficult time competing with Amazon and SpaceX, given their respective financial resources. They are both acquisition targets now as a result.

Just as Amazon beat Google to the punch with its cloud services business, SpaceX is doing the same to Amazon with its orbital web services.

This is the most technologically driven, disruptive time in history. Disruption is happening faster and at a much greater scale than we’ve ever seen before.

Which means we have to understand the stocks to avoid, as much as we need to understand the ones to invest in… and that’s exactly what we’re here for.

Jeff

P.S. Hi, Brownstone’s managing editor here.

If you want to know more about where Jeff has his eyes trained for the SpaceX orbital data center buildout, he’s put together an important briefing where he discusses the movers behind the buildout… as well as the companies Elon needs to get his AI data centers into space.

You can go here to learn more.

Read the latest insights from the world of high technology.

Imagine if a small number of elites – with tight coordination with the U.S. government – had a chokehold...

We have spent the last two years focused on the obvious AI constraints: semiconductors, high-bandwidth memory, networking equipment, and...