An Exciting Moment for the Nuclear Fusion Industry

While I maintain that the “AI Fear Trade” is largely overblown, that doesn’t mean there won’t be market shocks...

This was a surprisingly interesting week…

This was a surprisingly interesting week despite being the first full week of August when so many are enjoying the last few weeks of summer in the Northern hemisphere.

OpenAI just released GPT-5, and it was underwhelming. I plan on writing about this next week. The generative AI company also released some open-weight models, empowering the world to work with its earlier generation of frontier models.

There was a major kerfuffle between the Bureau of Labor Statistics and the executive branch due to the acknowledgement that labor data has been grossly inaccurate for years, resulting in poor policy decision-making. This is a very interesting topic that we covered in this week’s Bleeding Edge – The Fed’s Pivot Point Just Arrived.

Noteworthy was the publishing of the SEC’s policy paper for the crypto/blockchain industry and subsequent presentation from SEC Chair Paul Atkins.

What’s happening with regards to digital assets right now from a regulatory and policy perspective is jaw-dropping. It is what we in the industry could have only dreamed about just a year ago. This topic was covered in The Bleeding Edge – The Financial System Is Going Onchain.

And of course, tariffs and trade negotiations are still ongoing with the U.S. implementing tariffs on Canada, Brazil, and a few others, as well as ongoing negotiations with China.

In this week’s AMA, we dive further into tariffs and what they mean in a couple of the questions below. This is an interesting discussion that’s worth understanding.

And it appears that President Trump will be meeting with Vladimir Putin as early as next week in an effort to put an end to the Russia-Ukraine conflict. Let’s all hope for peace and an end to this ridiculous war, waste, and corruption.

We have so much to look forward to, and far better ways to spend our time and money making the world safer, cleaner, and more productive.

Have a great weekend,

Jeff

Jeff,

When are you thinking of returning to the Biotech Sector? Many exciting things are going on. 2020 was horrible, I get it… I was overweight biotech in general.

Hopefully, lesson learned.

I would love to hear your opinions on the sector.

Love your work

– Gregory W.

Hi Gregory,

You’re absolutely right, there are so many exciting things going on in the biotech industry right now. In fact, from my perspective, I’ve never seen so many exciting developments in the industry as those that I’m seeing right now.

And like you, I also had a lot of personal exposure to biotech as we entered the pandemic/biotech winter.

We’ve never had a biotech winter drag on for this long. It’s even more unbelievable considering the past three or four years have seen an absolutely incredible amount of investment (private capital), innovation, and progress in life sciences and biotechnology.

Earlier this year, Beam Therapeutics announced its base-editing breakthrough for a genetic editing therapy that it has been developing for a disease called Alpha-1 antitrypsin deficiency (AATD), which we covered in The Bleeding Edge – Beam Us Up, Biotech.

AATD is a disease caused by a single-gene mutation in the liver that results in lung disease in about 80% of cases. It often also results in liver diseases like cirrhosis and cancer, which often require a liver transplant.

Severe cases can be life-threatening. There is no known cure. The only existing treatment is limited in its efficacy and doesn’t actually treat the disorder.

And that was the often devastating reality of living with AATD… until Beam released research that detailed the results of a promising new treatment.

The incredible results of its genetic editing therapy demonstrated a marked increase in healthy protein in the lungs and a marked decrease in the mutant protein, both within a month of the initial treatment.

I use this as an example because these are incredible results from Beam, the kind that typically send a stock much, much higher in biotech. And yet, Beam (BEAM) is trading down 47% since its February high this year. It makes no sense at all.

In Another Win for Precision Medicine, we also covered the incredible story of Kyle Patrick “KJ” Muldoon Jr., a baby born last year with a very rare genetic disease – carbamoyl phosphate synthetase 1 (CPS1) deficiency.

A deficiency of CPS1 enzymes in the liver affects the body’s ability to break down protein, which can lead to a buildup of ammonia – a byproduct of protein – in the body.

Ammonia buildup can lead to brain damage, a coma, and, eventually, death. Unless you are old enough and stable enough for a liver transplant. KJ was neither, which left one option – gene editing therapy.

The medical team used a form of CRISPR technology referred to as base editing. The genetics team knew exactly what the mutation was and what a healthy sequence should look like for the CPS1 gene, so they were able to design a genetic therapy for him.

And so far, that therapy has been a success. Over the following two months, KJ received two more infusions of the therapy via IV and was recently allowed to go home with his family. He hasn’t been completely cured… yet. But his disease has been significantly minimized.

We’ve talked about a potentially very strategic acquisition in the genome sequencing industry and the de-extinction of dire wolves and the staggering potential of personalized precision medicine if it only had the room – and capital – to thrive.

Just this week, I wrote about a company called Profluent that’s behind the world’s first artificial intelligence (AI)-developed genome editor in Monday’s issue, The Bleeding Edge – The World’s First AI Genome Editor.

In that issue, I provided some context for where the publicly traded biotech industry is right now and what’s inhibiting institutional capital from investing in biotech right now.

And that’s all just a highlights reel of what’s been going on in the biotech industry, and just in 2025. This year has already shaped up to be incredible for biotechnology… except you wouldn’t know that looking at how the market is still treating biotech.

I do believe we’re on the cusp of a shift, though, and that we’ll finally be able to provide substantial coverage and research on the biotech industry before the end of this year (I hope!). Private capital is already flowing into biotech again, which is a very good sign.

This high-rate environment has been openly hostile to progress in small caps and the early-stage biotech industry. And as my Near Future Report senior analyst, Nick Rokke, covered earlier this week in The Fed’s Pivot Point Just Arrived, the Fed will have to end its enduring campaign against cutting interest rates soon.

The data strongly supports lowering rates. As I’ve said before, any further stalling at this point is just Powell prolonging this game of political chicken with the U.S. government to the detriment of the entire country.

And that rings truer now in the wake of the Bureau of Labor Statistics’ bombshell reveal that economists and policymakers have been making decisions based on faulty jobs report numbers… for years now.

I want to see the rate cuts begin and the early stages of institutional capital rotating into the biotech sector. Without strong institutional interest, we just won’t see healthy market conditions in biotech.

What we want to see are market conditions whereby when a biotech stock releases great clinical results, the stock moves up significantly higher. This typically leads to a secondary raise for additional capital to support the most promising clinical programs.

This gives investors the confidence that the biotech companies will have the capital to see their research and development through to the next major milestones.

If the publicly traded biotech sector isn’t acting normally in this way, then it is very hard for me to stack the deck in the favor of my subscribers.

From my perspective, the risk-to-reward isn’t strong enough. So, I’d prefer to wait until I have confidence that the great biotech companies producing great results will be rewarded by the markets through a significant increase in share price.

Despite my own excitement – and that of my team – I’ll be patient until that time comes.

That doesn’t mean that we haven’t been working on biotech. Not only do I continue to stay on top of industry developments, but we’ve also been working on enhancing the biotech system I originally built with a wider range of industry data augmented with AI, designed to improve our timing for recommendations.

My Brownstone Unlimited subscribers will be the first to know about this as we get closer to relaunching biotech research. You’ll be the first to know and also get early access to the research before it is launched.

Jeff,

It appears you are not in favor of Chair Powell’s and the Federal Reserve’s decision not to reduce interest rates.

The economy, the national debt, the stock market, and the housing industry are not part of the mandate of the Federal Reserve. If you would look into their main purpose mandate, you would find they focus on controlling inflation, unemployment, and recession.

The economy is not part of their role. Sure, President Trump would like to see the interest on the national debt be reduced. We all would. But he would be better served to lower government spending (which, obviously, he is not a fan of), stop the inflationary practices of tariffs, and stop benefiting the ultra-rich while pretending to only benefit the lower-income families.

Don’t get me wrong. I am a fan of President Trump. Voted for him and like much of the things he is doing. Using tariffs as a negotiating chip is good to a point, and it is important to have a fair trading agreement with foreign countries, but tariffs hurt us at home and are inflationary.

Chair Powell should not reduce the interest rate when higher inflation is possible and the economy is doing well. The Federal Reserve needs the positive interest rates as ammo to use if we start to go into a recession and unemployment returns. Your response is welcome.

– Norm T.

Hi Norm,

I’m definitely not in favor of Chair Powell’s insistence on keeping the Fed Funds rate artificially high. And I agree with you, the mandate of the Fed is to prioritize keeping inflation under control and avoiding periods of high unemployment.

And that has been exactly my point. Inflation is down significantly, CPI is below 3% and dropping, and prices for many goods and services have declined since the start of the year.

And employment is not overheating, quite the opposite. As I mentioned above, we actually covered this interesting topic earlier this week in The Bleeding Edge – The Fed’s Pivot Point Just Arrived. For years, the BLS has been manipulating data to make us believe that the employment numbers are strong, only to turn around and revise downward month after month.

Labor force participation rate has rolled over and is declining quickly:

Source: Federal Reserve Bank of St. Louis

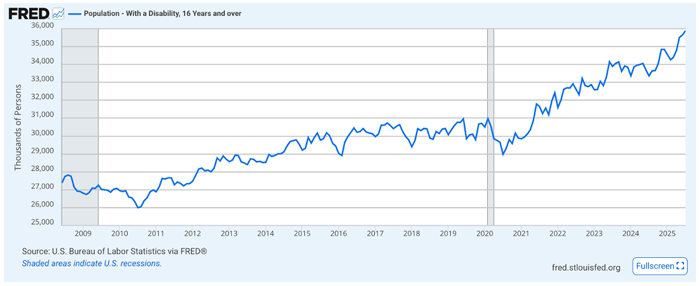

And just look at what has happened to the population old enough to participate in the labor force… disabilities began to skyrocket starting in the spring of 2021:

Source: Federal Reserve Bank of St. Louis

Note that the Y-axis is in thousands of persons, which means that the chart is showing us that almost 36 million labor-aged Americans now have a limited ability, or no ability, to participate in the workforce.

This is why it is so important to lower interest rates. It is a critical component to supporting the re-industrialization of the U.S., improving supply chain security, and, more specifically, supporting the labor markets with new jobs in manufacturing, construction, and industry.

And investment in automation technology, AI, and robotics is necessary to fill those jobs that are difficult to fill. There are labor shortages in trucking, logistics/distribution, and healthcare that have long plagued these industries. This is where technology can help.

As for the tariffs, there are two important points.

First, they are a tool for negotiating more fair and balanced trade agreements. If we think back to April of this year, the mainstream media, economists, and institutions that are just political shills gave us the impression that the sky was going to fall and we’d have runaway inflation. Yet here we are. It’s August, and those dire predictions simply didn’t come true.

Most major trade agreements have already been put in place. China is the one major country that still needs to be resolved. And it will get resolved. The tariff tantrum is temporary. Just a process that the current administration has to work through to rebalance trade agreements around the world.

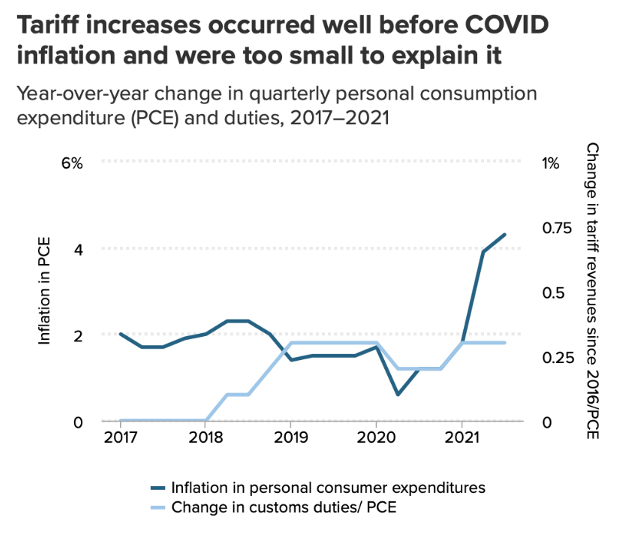

The second point is that tariffs, at large, have not led to large spikes in inflation in the past in the U.S.

A perfect – and very recent – example is the actual impact of President Trump’s first-term tariffs in 2018–2019 on prices. The study shows that removing those tariffs would have only reduced inflation by 0.3 percentage points.

Source: Economic Policy Institute

In addition to the impact only being 0.3 percentage points (30 basis points shown in the light blue line above), the tariffs were designed to assist U.S. industry in steel, aluminum, and other sectors that were suffering from low-cost competition from China.

Economists, academic institutions, and media that continue to parrot that the tariffs will cause significant inflation are very politically driven, as opposed to data-driven. And they ignore the fact that the tariffs are just a tool being used to rebalance trade agreements and rebuild the U.S. manufacturing sector across many industries to improve supply chain resilience.

I hope that these are goals that we can all agree on. After all, if the U.S. no longer has access to semiconductors made in China, or no longer has access to life-saving drugs made in China, I think most will be hoping that these critical products were being made a lot closer to home.

Although I can see the many benefits of blockchain, tokenization, and stablecoins, I have a troubling concern about the stablecoins themselves. They will provide a large and growing demand for US Treasuries (which is a good thing for the US government since foreign governments and others are pulling away from them due to deficits and growing U.S. national debt), but isn’t this a case of the bigger sucker theorem in practice?

It seems to me that if the underlying foundation – i.e., U.S. Treasuries – is becoming less and less trustworthy, just finding another source of demand to shore up the present situation does little to correct the longer-term problem. Although coins may have advantages over dollar bills, are we not just adjusting the deck chairs on the Titanic?

– Ross W.

Hi Ross,

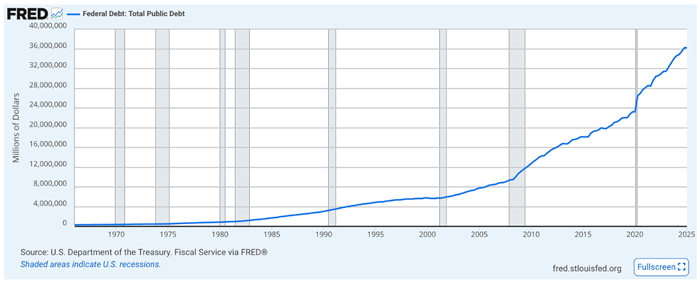

You’re not wrong, with a national debt now exceeding $37.2 trillion, it gives me a pit in my stomach. To your point, how can this end well?

Source: Federal Reserve Bank of St. Louis

Just look at the explosion in debt from Q1 of 2020 at $23 trillion to $37.2 trillion now. That’s a $14.2 trillion increase in just five years. How is that even possible?

Well, we found out, didn’t we? $2 trillion annual deficits year after year, largely corrupt pandemic spending, and – as has been discovered by DOGE – the funneling of hundreds of billions of taxpayer dollars to fraud, waste, and politically driven abuse through non-governmental organizations (NGOs).

Sadly, this fiscal year’s budget in the U.S. was already in place last year (fiscal year runs October 1, 2024 – September 31, 2025). And while a lot of progress is being made in cutting this wasteful spending, it will still take a couple of years for those cuts to dramatically reduce the deficit.

I lean toward optimism based on what we’re seeing today, but I still want to see that deficit shrink dramatically. And if it were up to me, I’d prefer a balanced budget just like any business or household has to do to stay solvent.

But to get to your question about stablecoins, no, it’s not just another kind of shell game.

Yes, it will create trillions of dollars of demand for U.S. Treasuries, which will offset any short-term decline in demand for U.S. Treasuries… mainly from China. But that oversimplifies the importance of stablecoins.

The reality is that the large-scale purchases of U.S. Treasuries will just be an effect of recent stablecoin legislation that was just signed into law (GENIUS Act).

The purpose of stablecoins, however, is foundational to the process of upgrading the global financial infrastructure to take advantage of blockchain technology.

Traditional finance is migrating to digital assets (primarily stablecoins) to take advantage of the capabilities of blockchain tech, resulting in near-instantaneous settlement times, dramatically lower costs (as in, more than 90%), and automation (think smart contracts and oracles).

If you haven’t done so already, yesterday’s Bleeding Edge – The Financial System Is Going Onchain is a great read related directly to this topic.

But as for the bigger issue that you brought up, are U.S. Treasuries becoming less and less trustworthy? I’m sure opinions would vary on this point, but the caveat to that question is compared to what? Compared to the EU/euro, China, Russia, Japan, etc.?

A couple of years ago, the euro had overtaken the U.S. dollar as the currency in which global trade was being conducted. Today, it’s the complete opposite with 58% of global trade conducted in U.S. dollars.

And we should ask, is the U.S. economy getting stronger or weaker right now with the current economic, fiscal, and regulatory policy?

What we see happening right now is regulatory policy that is strongly supportive of technological innovation (blockchain, AI, and automation), pro-energy (natural gas, fission, and fusion), and laser-focused on rebuilding the U.S. manufacturing base. Trillions of dollars in foreign direct investment have been announced this year.

Will these things be good for the U.S. economy and the U.S. dollar? Absolutely. And will they result in more or less demand for U.S. Treasuries? The answer is more.

There are two ways to dig out of a debt problem. One is radical austerity, and the other is economic growth, thus reducing debt and deficits as a percent of GDP.

It appears that the Trump administration is leaning heavily into economic growth as a pillar and is taking steps towards dramatic reductions in the fiscal deficit over a number of years (though not so radical that it will negatively impact economic growth).

While personally, I’d prefer to see more aggressive steps to reduce the fiscal deficit quickly, the current policies will result in strong economic growth.

And if I’m right about my predictions regarding artificial general intelligence (AGI) and the incredible impact it will have on productivity and economic growth, we’re in for an incredible ride.

And both U.S. dollars and U.S. Treasuries will be in high demand.

The U.S. economy is now a gravity well for technological innovation in every sector that matters.

We’ve now entered a period of hyper-acceleration.

Jeff

Read the latest insights from the world of high technology.

While I maintain that the “AI Fear Trade” is largely overblown, that doesn’t mean there won’t be market shocks...

The more transactions that take place over Meta’s networks, the more money it makes. So why limit that to...

Cortical Labs has been developing a biological computing system based on human brain cells…

Thanks for signing up for The Bleeding Edge — we’re glad you’re here!

Want updates sent straight to your phone too? Sign up for SMS alerts to get the latest delivered via text.

Brownstone Research: By submitting your phone number, you agree to our SMS Terms & Conditions, Terms of Use, & Privacy Policy, and give express written consent to receive marketing text messages from BSR. Messages are recurring & frequency may vary. Reply STOP to 94703 to opt out. Reply HELP to 94703 for info. Consent is not a condition of purchase. Message and data rates may apply. For additional information, you may contact Customer Service at 888-512-0726 or smssupport@brownstoneresearch.com.