Another Cage Match in D.C.

These situations tend to happen when your back is against the wall…

The banks are trying to stall. But the new crypto-friendly regulators are playing a different game.

The U.S. Congress isn’t known for its efficiency….

But at this rate, the future of crypto will arrive without Congress’ permission.

We’ve been tracking the regulatory progress around digital assets in the United States for years now.

The reason is simple: The United States represents the most robust financial markets in the world. Fully welcoming digital assets into that world with comprehensive regulations will be a boon to the industry and investors.

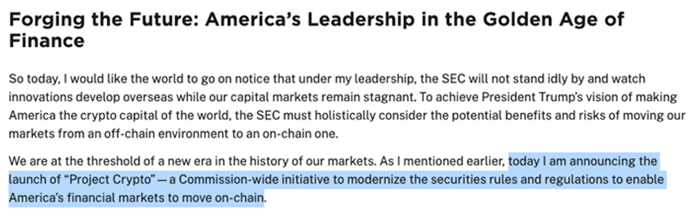

The White House, SEC, and CFTC are pushing an agenda known as Project Crypto. The initiative is incredibly ambitious. It’s not just focused on making assets, protocols, and blockchains part of the financial ecosystem. It wants to bring the financial system itself onchain.

Here’s SEC Chairman Paul Atkins’ speech announcing it last year:

This is part of the President’s plan to make America the crypto capital of the world.

Part of that plan was to get legislation through Congress and signed into law by the President. Specifically, the administration is pushing for the Clarity Act, an extensive bill that acts as the framework for how digital assets are regulated in the United States.

Back in July 2025, this seemed inevitable.

That’s when the Clarity Act passed the House of Representatives with a bipartisan vote of 294 to 134. It was just up to the Senate to do the same.

But here we are nearly a year later, and the Clarity Act is still awaiting a vote in the Senate.

So, what happened?

“GENIUS got past them… They’re back in a hardcore way, and the stakes are high.”

That quote is courtesy of former Republican representative Patrick McHenry of North Carolina. Patrick was the former Chair of the House Financial Services Committee until January 2025.

He was familiar with what was going on in Washington, D.C. and a proponent of the digital asset industry. The “they” he’s referring to is the American banking industry.

GENIUS Act, the legislation tied to regulating stablecoins in the U.S., took the banking industry by surprise. It wasn’t on their radar. And once it passed, it set off all sorts of alarm bells for banks.

Regulated stablecoins have the potential to draw some deposits from traditional banks. And the reason is simple.

The national average savings account interest rate is 0.38% APY. Meanwhile, many stablecoins offer close to a one-month Treasury bill of 3.5%.

It’s not a hard choice.

Banks usually portray depositor flight in apocalyptic terms. It would threaten the stability of the financial system, they say.

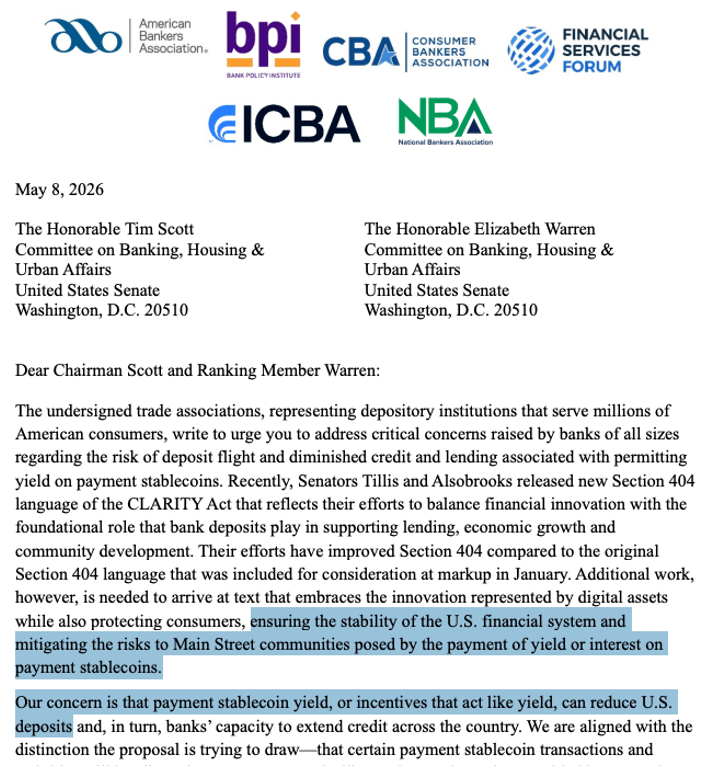

I’m not exaggerating. Here’s the letter that was sent to Senator Tim Scott, Chair of the Committee on Banking, by trade groups who represent the major banks.

Source: Bank Policy Institute

What the letter did not mention is the fact that new credit issuance is already addressed by decentralized finance (DeFi) protocols. These are solutions that extend loans using stablecoin deposits.

There is an entire financial economy that already runs using stablecoins. And if it’s embraced, there won’t be any credit issues.

But customers flocking towards stablecoins does pose another threat…to the banks’ bottom line.

Any depositor withdrawal would impede traditional loan issuance. That means less profit for the banks. And that is what the banks really fear.

As McHenry said, GENIUS got by them. But they won’t make the same mistake with CLARITY, which is a big reason the bill remains stalled in the Senate.

And a recent decision by the SEC reveals how this is playing out in real time…

The SEC, CFTC, and White House aren’t asking for permission anymore.

On June 11, the SEC voted to propose a rule.

A vote here means the SEC commissioners agreed about a proposal that it’s releasing to the public. It’s not just a few lines mentioned by an SEC staffer during a side event.

The proposed rule is actually the removal of a rule from 2005. That was the time when electronic order books were becoming very popular. There was also a greater reliance on computer trading. The SEC wanted to address what was a growing fragmentation.

Trading didn’t just happen at one exchange. Transactions unfolded across many regional exchanges and off-exchange dealers. This caused price discrepancies for the same asset.

The SEC’s solution was Rule 611 and Rule 610(e) among others.

At a high level, these rules help to ensure good pricing for a system that was still living in a hybrid between open trading pits and electronic pricing world. Basically, a dealer couldn’t fill your sell order for less than what exists on the order book.

And these are the two rules that the SEC looks to rescind with its latest proposal. At first glance, this might seem less than ideal. After all, we all want good pricing.

But these rules were created for a different era of trading.

More importantly, it matters for DeFi.

That’s because if tokenized stocks are trading onchain, they go against these rules. Most of DeFi isn’t relaying prices to and from things like the Securities Information Processors. And many times the price you see isn’t based upon the size of the trade. Bigger size means less liquidity in a DeFi pool to fill the order, so the order is filled at a slightly different price.

Not to mention some swap protocols like Uniswap don’t even have an order book. Meaning there is no bid or offer price to relay even if it wanted to.

The SEC rules here are outdated as it relates to onchain finance. And they neglect the fact that arbitrageurs act on price discrepancies in real time, which helps the resiliency of markets.

It’s in part why the SEC’s decision to remove the rules is like saying ‘here you go, you’re not in violation of trading tokenized equities.’

The most interesting part here is this rescission doesn’t require permission from Congress via the Clarity Act.

Clarity Act is still worth passing. And, with any luck, it will be soon.

But financial regulators aren’t waiting around anymore. The goals laid out in Project Crypto are being accomplished by the SEC and CFTC wherever possible.

The banks are trying to stall. But the new crypto-friendly regulators are playing a different game. The removal of the two SEC rules is a boon for tokenized assets and a shot across the bow at legacy incumbents.

We’ll wait to see how they respond…

Your Pulse on Crypto,

Ben Lilly

Editor, Chain of Thought

Read the latest insights from the world of high technology.

These situations tend to happen when your back is against the wall…

Using these two pieces of technology, two agents negotiated scope, price, deadlines and terms for an agreement.

Central authorities already have a tight grip on your finances. Now, they look to be coming for your mind.