CLARITY Text Just Dropped… Here’s Where Everybody Sits

The CLARITY Act text went public Wednesday afternoon, and responses have roughly fallen into three camps…

This is a credit system that is not walled off to the 1% or only limited to certain assets like your home.

In January 1848, James Marshall discovered gold flakes in the tailrace of Sutter’s Mill in Coloma, California.

Word spread fast. And by 1849, California had itself a gold rush.

But those early ‘forty-niners’ were in such a hurry to get out West that a problem emerged soon after. There simply wasn’t enough coinage to support the commerce of the tens of thousands of new arrivals.

Desperate times called for desperate measures.

So, for a brief period in the summer of 1849, much of California’s economy ran on prospected gold dust.

In a saloon, it was common for a bartender to charge a “pinch” per drink. This led to an obvious problem—a pinch of gold is relative. As a result, it was in your best interest to only order from bartenders with small hands.

It’s an interesting bit of history and a good reminder of something we often forget.

For literally millennia, gold was not an asset. It was money.

Gold coinage dates to at least the ancient Greeks. But in the mid-1600s, something important began to happen with gold.

Around this time, English banks began to accept gold deposits. These bankers would issue receipts that depositors could use to pay for everyday items.

This wasn’t a novel solution. The practice of using notes for exchange was already being used elsewhere in the world. What was different with these Goldsmith Bankers was the financial system that began to develop. The banks began issuing loans against the gold deposits.

In other words, gold wasn’t just a day-to-day currency. It was now an accepted form of collateral that could be borrowed against.

This was a pivotal moment for the yellow metal. It gave the asset convertibility. Said differently, gold could now be exchanged for other assets or currencies. In this specific example, that other currency was an IOU or debt.

It sounds small, but it had a big impact: citizens could secure credit with greater ease.

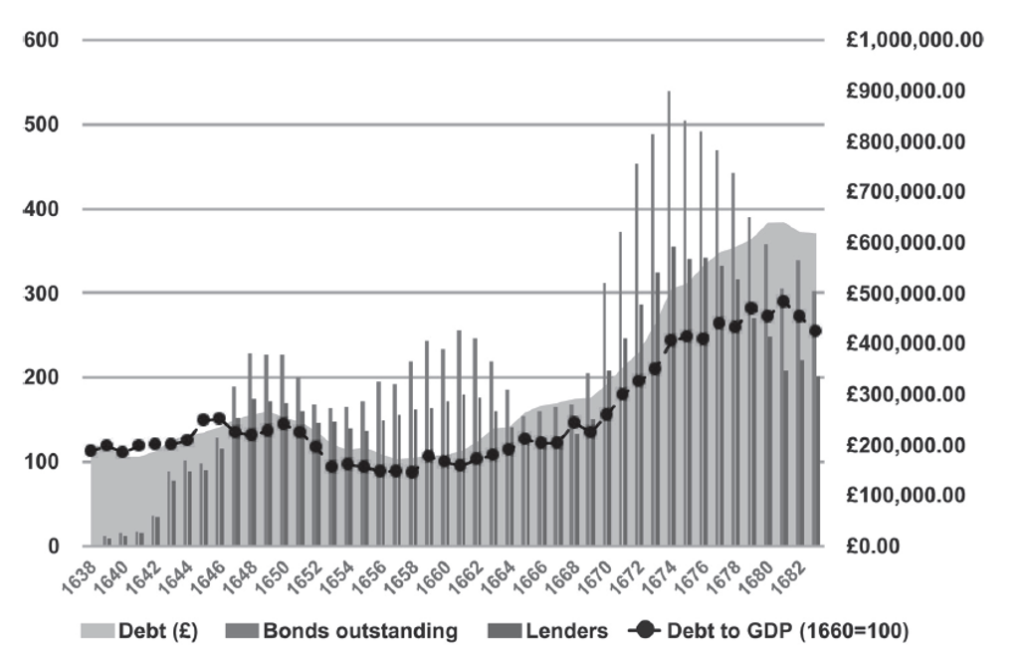

The chart shows debt growing in the 1640s to 1670s, right when the Goldsmith Banking era began.

Source: Oxford University

The impact…

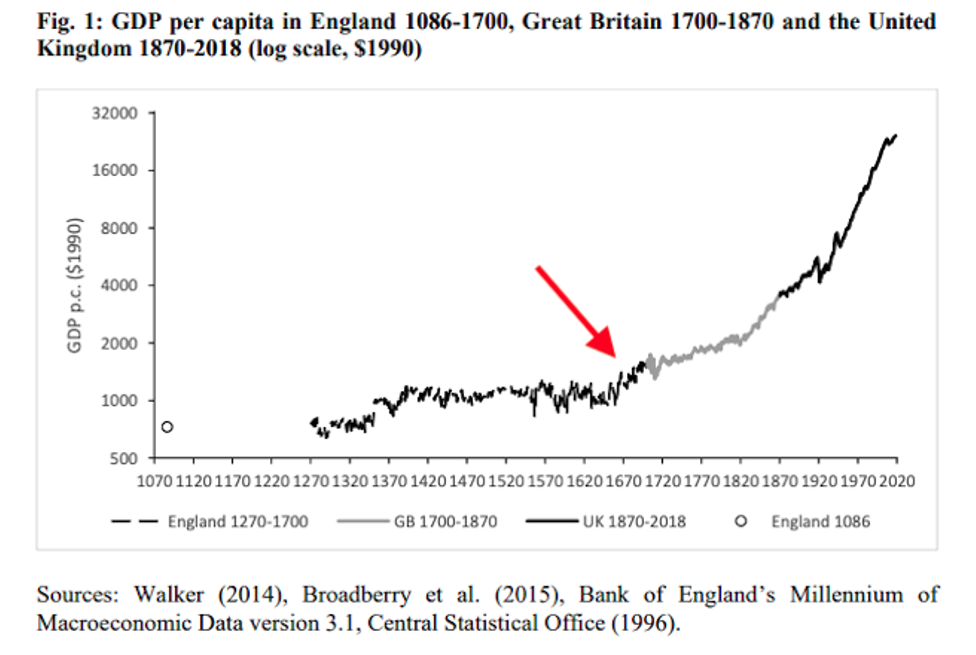

The economic output per person in England grew significantly for the first time in three centuries.

Source: Oxford University

Unlocking gold was a transformational moment for the UK economy. Gold went from being a currency to an asset backing a new credit system. That sparked an economic boom.

So far so interesting.

But what does this have to do with digital assets?

Well…

A fresh wave of assets is about to hit the market via IPOs from SpaceX, OpenAI, Anthropic, and others. It will generate trillions in value that the market is not pricing in.

And just as gold’s value was unlocked in the 17th century, these new assets can now be unlocked via innovative blockchain solutions.

The lending and borrowing platform Morpho announced yesterday it raised $175 million from backers like Paradigm, Apollo Global Management, VanEck, a16z Crypto, SBI Holdings, and others.

Their stated goal: To build the open credit network for the world.

It’s a big claim. But not an unrealistic one.

After all, Morpho is a permissionless lending protocol that sits on a public blockchain. Anybody can access it. Anybody across the globe can build atop it. And virtually any asset in the world can be used on it.

That makes Morpho’s addressable market truly global.

What’s more, Morpho can unlock the value of nearly any asset. It’s reminiscent of Goldsmith Bankers unlocking fresh credit in the 1670s in the UK.

Only this time, it’s not just gold, gold dust, or gold notes. It’s conceivably any asset, or about $775 trillion worth.

This is where any asset becomes money, just like what happened to gold.

Morpho is already onboarding assets beyond cryptocurrencies like ETH and BTC. It allows an array of stablecoins like USDC, which is backed by cash and U.S. Treasuries, USDe, a stablecoin backed by trade strategies and wrapped U.S. Treasury products.

Morpho even accepts more exotic forms such as apyUSD, a stablecoin we covered in Michael Saylor’s Financial Alchemy that is backed by publicly traded company Strategy’s STRC preferred stock with dividends. It also accepts foreign stablecoin currencies that track the Japanese yen and euro.

Then there’s ACRED, a diversified credit fund issued by Apollo Global Management. There are also fixed-income assets issued by Pendle Finance. Even exchange-traded funds (ETFs) issued by Ondo Finance are accepted as collateral.

This is a credit system that is not walled off to the 1% or only limited to certain assets like your home.

We’re talking about the entire financial system backing what is about to be an even bigger credit system. And it’s happening just as the largest private companies in the world IPO to public markets.

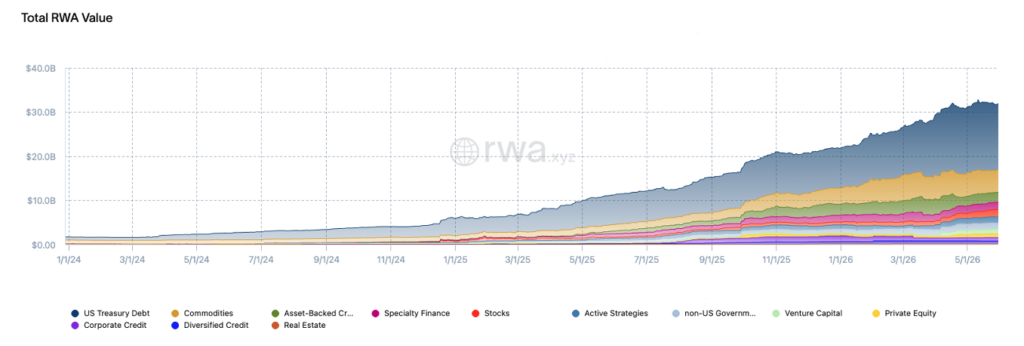

Today there is about $31 billion in real-world assets tokenized on blockchains. And more than $300 billion worth in stablecoins.

Source: rwa.xyz

By decade’s end, this figure will reach several trillion dollars. And that’s without legislation like the CLARITY Act accelerating this trend.

If the bill passes in the coming weeks to months, we should expect the $1 trillion market to be realized in 2027, which will kick off a wave of opportunities within the digital asset industry.

This is no pipe dream…

We covered how asset issuers are already building inroads into decentralized finance systems.

If Congress gives them the green light via CLARITY in the coming months, these inroads will buzz with new assets coming online.

This multi-year market expansion is building momentum now.

And the best is yet to come.

Your Pulse on Crypto,

Ben Lilly

Editor, Chain of Thought

Read the latest insights from the world of high technology.

The CLARITY Act text went public Wednesday afternoon, and responses have roughly fallen into three camps…

After sitting in the Senate for more than a year, the CLARITY Act is getting ready for a vote…

U.S. debt is about to be the currency used by everyday individuals across the globe.