CLARITY Text Just Dropped… Here’s Where Everybody Sits

The CLARITY Act text went public Wednesday afternoon, and responses have roughly fallen into three camps…

It won’t be smooth sailing. In fact, the Bitcoin market could get downright nutty soon.

Whatever else you want to say about Michael Saylor…you’d have to say he’s one heck of an alchemist.

Saylor is the CEO of Strategy (MSTR), a former software company turned Bitcoin treasury firm.

Strategy’s strategy is simple—raise capital to buy Bitcoin.

That’s it.

That company has been good at doing that. It has more than 800,000 BTC held to date.

How Saylor and Strategy has done that is also relatively straightforward. It’s primarily through an equity offering.

Strategy offers new shares of MSTR stock in the open market. The proceeds from these sales go towards buying Bitcoin.

In the years before spot ETFs, gaining exposure to Bitcoin in a traditional brokerage was difficult. Strategy was a stock that solved that problem.

Over time, Strategy has diversified its financing…

In addition to equity offerings, it began issuing convertible notes. This is debt that can be converted into stock. Once again, Strategy uses the funds to buy Bitcoin.

The interesting part here is that the capital is borrowed at low or even zero interest. That’s due to the convertibility feature. In a rising Bitcoin or stock environment, this means the creditor can convert to MSTR shares and collect a possible premium. So, the creditor forgoes all or most of the interest.

These two methods have helped Strategy become the largest corporate Bitcoin treasury to date.

But Saylor has one more trick—He recently rolled out preferred stock offerings.

The offering we wanted to focus in on today is STRC or “stretch”. It’s an instrument that pays variable yield around 8-11.5%.

STRC has no maturity date. We can think of it like a bond that never expires. Like a bond, its “par” price is $100. If the price of STRC rises above $100, the yield payment is cut. And if the price drops below $100, the yield payment rises.

This helps keep the STRC instrument near its $100 price point.

These STRC shares are offered to the market continuously. Which gives Strategy a constant capital raising solution. The upshot is that the product doesn’t dilute MSTR shareholders the way new equity would.

The downside is it’s sure to raise some eyebrows…

After all, Bitcoin has no cash flow. It has no dividends.

So, where’s the yield come from?

The answer via SEC filing:

We expect to fund any dividends paid in cash on the STRC Stock primarily through additional capital raising activities, including, but not limited to, at-the-market offerings of our class A common stock and our junior preferred securities.

Let me translate: The yield is paid by new buyers.

It’s tempting to call this a pyramid scheme. It certainly sounds like a pyramid scheme.

But there is some nuance…

For starters, Strategy lays this all out transparently via a prospectus, 8-K filings, and its own website. There are no false promises.

Strategy was, and still is, an analytics company that derives some revenue through existing SaaS contracts. In Q4 2025, it generated $59.6 million in product licenses and subscription services. Which means some of the old business is helping keep the operation sound.

What’s more, Strategy does hold underlying assets—about $62.5 billion worth. It’s not just hot air.

And finally, Strategy holds enough cash reserves to cover dividend payments for 2.5 years. It’s a buffer that Strategy intends to use during market disruption or a price crash.

For these reasons, STRC is above board in the SEC’s eyes.

And the funding mechanism does help Strategy pursue its main goal – buy Bitcoin. So there isn’t anything deceptive taking place here.

The real alchemy is what happens when Bitcoin’s price rises…

STRC holders get their yield payments. Investors keep purchasing STRC, which gives Strategy more capital to buy Bitcoin. This increases the amount of Bitcoin backing for each MSTR share. In turn, this boosts the price of MSTR faster than Bitcoin’s rise in price. And then, Strategy can go back to the well of issuing more MSTR shares in the market.

It’s a flywheel, one that ramps up during bull markets.

But what goes up, must come down. And that’s my worry here.

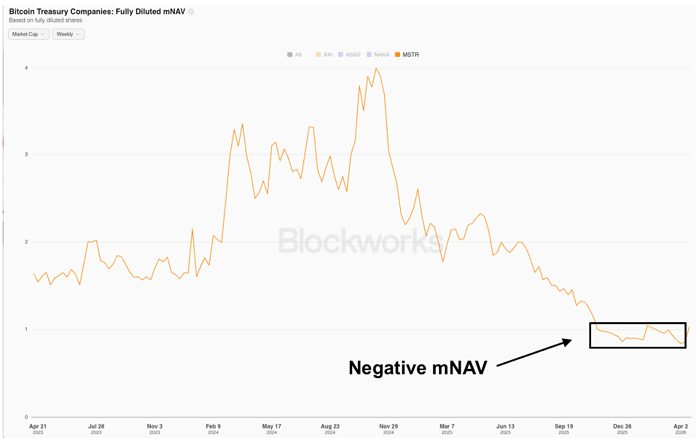

Strategy was already realizing something called negative mNAV. The “M” stands for market cap. The “NAV” is net asset value. The metric is expressed as a ratio.

And a negative mNAV happens when the market capitalization is less than the amount of assets in reserve. Said another way: The value of the company is less than the Bitcoin it holds.

And this metric has been in negative territory since November 20.

Source: Blockworks

A negative mNAV is scary for one reason: It suggests investors don’t want the assets that are represented by the shares.

Typically, Strategy would respond to this negative mNAV by selling Bitcoin to repurchase MSTR on the open market. This would reduce the assets being held and drive up the price of the shares, bringing this ratio closer to one.

But that’s a slippery slope.

Selling creates a fear that could hurt the exact asset giving Strategy its value. That’s because Strategy holds about 815,000 BTC valued at approximately $62.5 billion. It’s the largest holder. And if they start selling, the market will get spooked.

That’s what makes the STRC product so interesting…

It’s solving the mNAV issue.

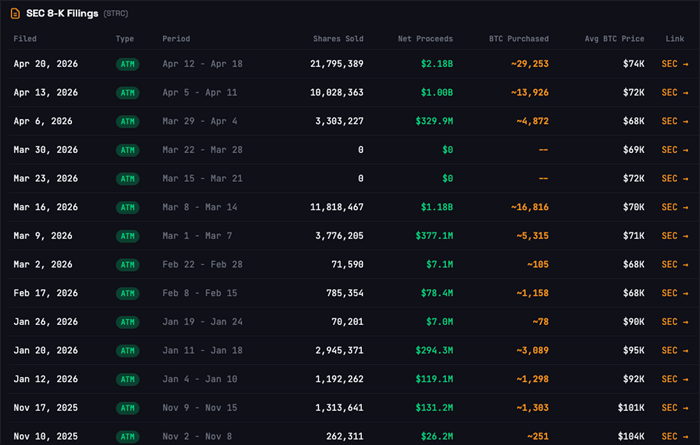

Strategy climbed out of its negative mNAV setup last week because the market is buying STRC in droves.

There’s been $8.25 billion raised through STRC sales to date.

To be more specific…After the initial sale back in July, sales were slow.

From November 10, 2025 to March 2, 2026 there was about $94 million being purchased per week.

On the surface that might seem like a lot…

But when compared to the last three weeks, the average weekly proceeds have risen to $1.17 billion. A 12.4x jump in sales.

Source: https://strc.live/ticker/strc

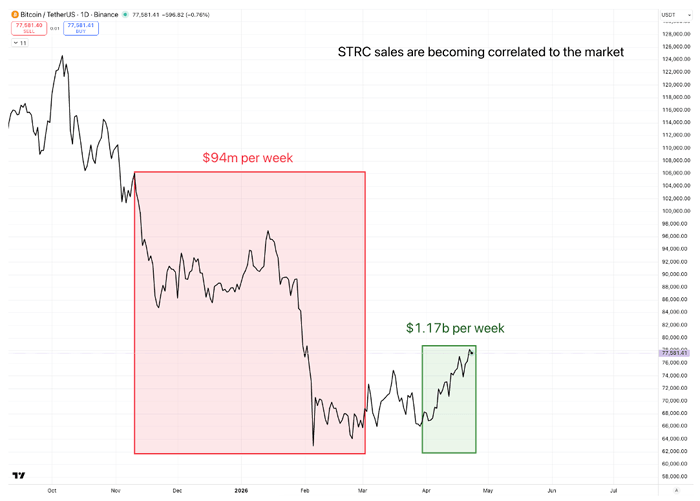

The sales have not only helped solve Strategy’s mNAV issue of late…

It’s turning on the financing flywheel we mentioned earlier.

That’s because these proceeds lead to Bitcoin purchases, which pushes the market higher along with it, which also boosts MSTR prices as well.

Source: Tradingview, strc.live

We might not like how the sausage is made when it comes to Strategy.

I’m certainly not an advocate of it…

But the numbers are what they are: The biggest buyer of Bitcoin now has the means and the motivation to juice the Bitcoin market.

And as we mentioned in our previous essay The Bitcoin Regime Change Has Already Started, the structure of the market is improving.

Of course, it won’t be smooth sailing.

In fact, the Bitcoin market could get downright nutty soon.

And here’s why…

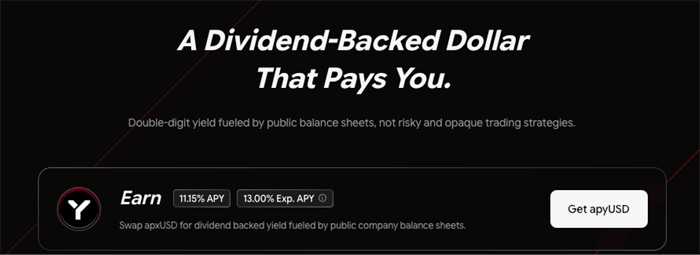

APYX is a project issuing a stablecoin called apxUSD.

It’s not a traditional fiat-backed stablecoin like USDC or USDT.

Instead, it’s backed by dividend-bearing real-world assets.

The asset in this case is Strategy’s STRC. Meaning 100 apxUSD are essentially backed by 1 STRC share.

But if you hold apxUSD, you do not receive yield. The token is primarily meant to act as a liquidity token in secondary markets and be used in various decentralized finance protocols.

The real use case is when somebody locks their apxUSD to the protocol. They earn the yield being derived from STRC. And since not all stablecoins are locked to the protocol, it means the yield payout is greater.

Think of it like this…

Imagine 100 apxUSD in circulation. Also imagine that 1 STRC produces $10 of yield over the course of year. But if only 50 apxUSD tokens are locked to the protocol, then those 50 tokens are earning the $10, which results in 20% annual percentage yield (APY) on the tokens staked.

This setup has resulted in APYX minting $185 million worth of stablecoins, producing an expected APY on locked tokens of 13%.

Source: app.apyx.fi

The rabbit hole goes way deeper when it comes to money markets onchain. That’s because users can leverage these instruments, lock in fixed rates on the asset, borrow against them, and more.

We won’t explore how some users are generating higher yield. The risk involved is beyond what most investors should be willing to stomach.

The point is that DeFi is becoming a source of demand for Strategy.

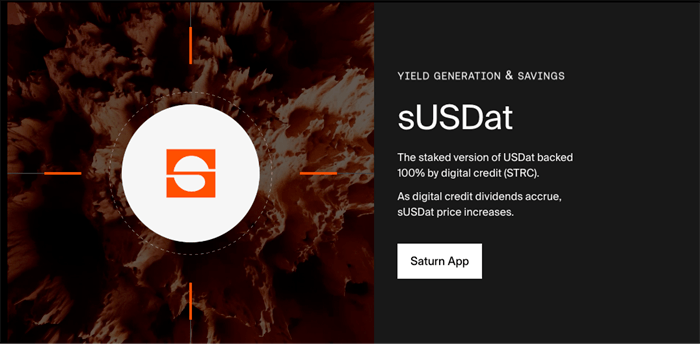

In fact, there’s another protocol called Saturn that has a similar setup as APYX, which is responsible for about $33 million STRC.

Source: Saturn.credit

This is real demand for an asset that sits on traditional markets.

We need to be aware of this trend. Because if the market continues its momentum, these numbers can grow…fast.

To be clear, all this will probably end poorly for Saylor over the long term. His financial alchemy reeks of hubris. And hubris always ends the same way.

But at least in the short- to medium-term, Strategy’s flywheel has the potential to make this next bull run truly unique. It will blend traditional markets with onchain markets in truly novel ways.

Buckle up.

Your Pulse on Crypto,

Ben Lilly

Editor, Chain of Thought

Read the latest insights from the world of high technology.

The CLARITY Act text went public Wednesday afternoon, and responses have roughly fallen into three camps…

After sitting in the Senate for more than a year, the CLARITY Act is getting ready for a vote…

U.S. debt is about to be the currency used by everyday individuals across the globe.