IPOs Are a Boom for Crypto

The trend of tokenized stocks coming onchain is not some pie-in-the-sky imagining of the future…

Be excited. The stage is set for one of the biggest bull runs in digital assets.

America’s Federal Reserve has a new boss…

Kevin Warsh was confirmed by the Senate last week. He’s set to be sworn in by the president today. By the time you read this, it might have already happened. Warsh will have his hands full.

That’s because the Middle East conflict—and the impact it’s having on inflation—is now a concern for the U.S. Federal Reserve.

We know this thanks to the April 28-29 Federal Open Market Committee (FOMC) minutes, which were dropped earlier this week.

The FOMC meetings are where Fed officials decide what to do with the fed funds rate—higher, lower, or unchanged. Rates held steady in April.

No real surprise there.

But buried in the minutes released on May 20 was a line that ruffled some feathers:

A majority of participants highlighted, however, that some policy firming would likely become appropriate if inflation were to continue to run persistently above 2 percent.

Translation: If inflation gets warmer, the Fed is open to hiking rates.

On the surface, it suggests that the Middle East conflict is beginning to cause unexpected concerns. That’s because oil prices are high. As I write, WTI Crude is about $96 a barrel. Brent Crude is north of $100. Rising oil prices mean rising fuel prices (gasoline, diesel, jet fuel, etc.). And rising fuel prices mean rising transportation costs…which means every consumer item that’s shipped (which is all of them) gets a little more expensive.

That’s inflation. All else equal, inflation means the Fed gets hawkish.

But rate hikes are not the real takeaway.

Reading further down, the FOMC minutes also had this:

Several participants indicated that, in a scenario in which the conflict was resolved soon, rate reductions would be warranted later this year.

For the time being, we should expect the current Federal Reserve trajectory to continue as Kevin Warsh begins his reign. And if anything, the debate is just on the timing of cuts.

Which forces us to wonder here at Chain of Thought—how will this impact digital assets and crypto?

The answer is going to surprise you…

Lending on public and permissionless blockchains differs quite a bit from the traditional economy.

Aave is the largest lending protocol in the industry. It holds more than $14 billion in assets across 21 chains. It has more than $10 billion in active loans.

For context, total assets locked in decentralized finance (DeFi) stand at $82 billion. That means Aave is nearly 20% of all of DeFi.

Its protocol works via overcollateralized loans. Meaning anybody can post assets (i.e., ETH, USDC) as collateral, and borrow against it.

The borrowed capital originates from lenders. These lenders range from retail to market makers as the protocol is permissionless – anybody can take part.

The borrowers then pay interest on the loan.

This is where the model breaks free from the traditional financial system.

When we take out a traditional mortgage, the bank holds our house as collateral. And the mortgage is then determined based upon yield markets that feed off the U.S. Federal Reserve’s interest rate.

In part, that’s why investors care what Powell, and soon Warsh, say and do. Their words can move markets.

But that’s not the case in DeFi.

Rates are set independently of the Federal Reserve.

Instead, rates are set based upon how much money is available to borrow relative to how much is being borrowed.

It’s simple supply and demand.

If there are a lot of loans being taken out relative to the supply of dollars, then rates rise. It’s algorithmic.

There’s no marble-floored room of governors debating. It’s a direct feedback system that keeps the amount of credit created onchain in check.

This means the credit market is not fully dependent upon what happens to interest rates at the Federal Reserve.

Which is why we often see borrowing rates on public blockchains drop below the federal funds rate – the interest rate set by the Fed.

For DeFi lending, only two questions matter:

When do rates tend to rise?

And how much supply exists?

Rates and market volatility go hand in hand.

It’s a true “flight to liquidity” effect. When prices in crypto begin to whipsaw in either direction, the lending market sees the effect. And rates start to climb.

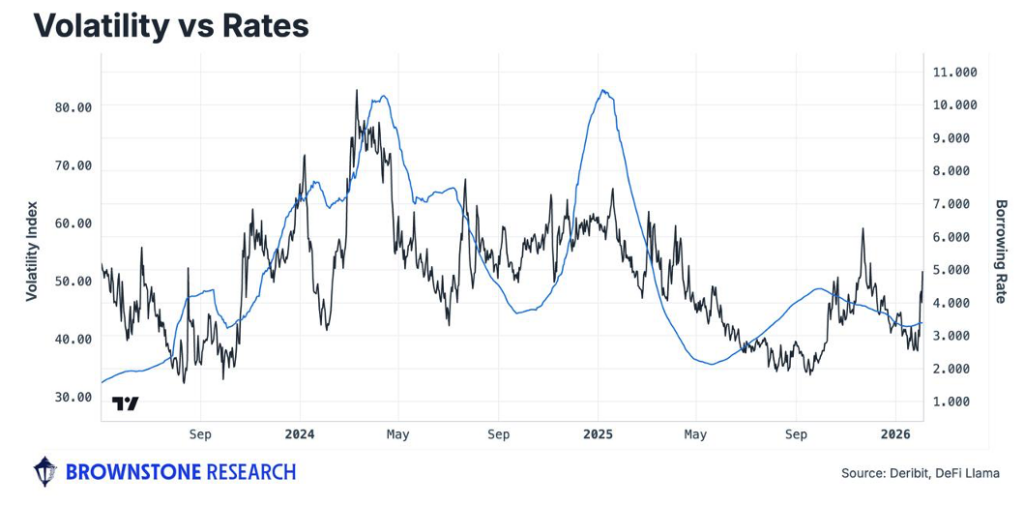

We can see this most easily by pulling up the Bitcoin volatility index (black) against the lending rate on Aave for the USDC stablecoin (blue).

It’s a clear trend. Volatility rises; rates rise. When the market is calm, rates drop onchain.

In fact, in 2024, a period that saw the price of Bitcoin rise from $42,000 to $100,000, volatility was climbing… Along with rates.

Traders and investors were looking for dollars to borrow.

And when the rates got too high, the digital asset market calmed down.

Here we see that rates tend to peak when the price of Bitcoin—and, by extension, the entire crypto market—tops out.

This is a relationship most analysts are not aware of. The “legs” of the market are often a direct result of the availability of liquidity and the cost associated with that liquidity. Essentially, it’s how hot prices can get. As liquidity gets more expensive, markets tend to be capped.

That’s what the chart above is showing.

This matters because the amount of stablecoins in circulation is posting all-time highs at more than $320 billion.

That’s remarkable.

And it’s a direct result of regulators putting more guidance into the market. First, it was the stablecoin bill called the GENIUS Act. Now, the CLARITY Act is gaining momentum as it approaches the Senate floor next month.

Any bullish sentiment that hits the digital asset market can now run further and hotter than ever before. It has less to do with the Fed, more about liquidity. And we have more than ever before sloshing around crypto.

Be excited. The stage is set for one of the biggest bull runs in digital assets.

Your Pulse on Crypto,

Ben Lilly

Editor, Chain of Thought

Read the latest insights from the world of high technology.

The trend of tokenized stocks coming onchain is not some pie-in-the-sky imagining of the future…

Whoever controls the information controls the market. Here’s how the CLARITY Act could upend Wall Street’s control…