AI Infrastructure Spend Is Accelerating

AI has been the dominant force in this market for the last three years. It started with semiconductors. Then it moved into data centers. Then networking. Then power. Then memory. And now the gains are spreading across the entire AI infrastructure stack…

Written by

34 Large-Cap Stocks Have Doubled – Here’s What They Tell Us…

By Nick Rokke, Senior Analyst, Brownstone Research

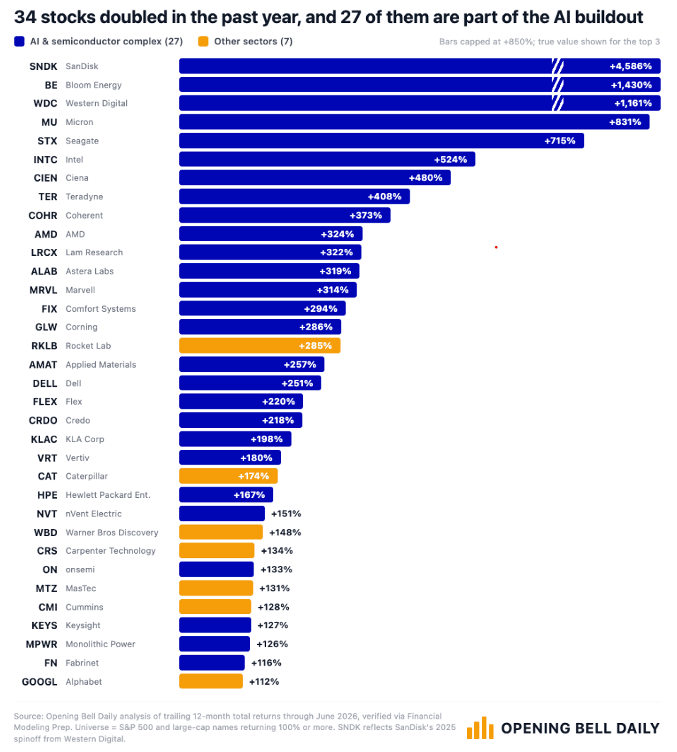

Thirty-four stocks in the S&P 500 have doubled over the last 12 months.

That’s not normal. According to Morningstar data, that’s more than double the annual average.

But I’m not here to tell you the market is strong. We all know that. The important part is what nearly all of these stocks have in common…

Of the 34 stocks that have doubled, 28 of them are directly tied to one technology trend. That trend is, of course, artificial intelligence (AI).

AI has been the dominant force in this market for the last three years. It started with semiconductors. Then it moved into data centers. Then networking. Then power. Then memory.

And now the gains are spreading across the entire AI infrastructure stack.

Some of these names should be familiar to Near Future Report subscribers. We’ve been involved in five of them over the last year.

And frankly, the 28 number may be too low.

For some reason, the team putting together this list did not classify Alphabet (GOOGL), the parent company of Google, as an AI stock.

We are counting it.

Google owns one of the leading AI labs in the world. It controls Gemini. It owns DeepMind. It has one of the largest cloud computing platforms. And it is embedding AI across search, productivity software, advertising, and infrastructure.

Then there are less obvious beneficiaries.

Caterpillar (CAT) is not an AI company in the traditional sense. It makes earthmoving equipment. But the AI infrastructure buildout requires land, construction, power, cooling, and heavy equipment.

MasTec (MTZ) and Cummins (CMI) are also not classic AI names. But they are tied to the data center, electrical, and power buildout that AI requires.

Carpenter Technology (CRS) has exposure to advanced materials and specialty alloys used across high-performance industrial and semiconductor applications.

So, really, 32 of the 34 stocks that have doubled are connected to AI.

This also tells us that the stock market is not just the Magnificent Seven stocks anymore.

In past years, market bears loved to argue that the indexes were being propped up by a handful of mega-cap technology companies. Microsoft. Apple. Amazon. Meta. NVIDIA. Tesla. Google.

That criticism had some merit. But it does not describe today’s market.

Alphabet was the only Magnificent Seven stock to make this list. The biggest gains are happening elsewhere. And that makes sense.

Companies like Microsoft, Amazon, and Meta are spending tens of billions of dollars to fund the AI buildout. They are building data centers, buying GPUs, securing power, and racing to integrate AI across their platforms.

That spending is enormous.

That spending has created opportunities elsewhere. And the biggest opportunity this past year has been in memory. SanDisk, Western Digital, Micron, and Seagate are all at the top of the list with the highest returns.

AI models require massive amounts of memory. Training consumes memory. Inference consumes memory. Agentic AI consumes even more memory because these systems are always working, always accessing data, and always generating tokens.

The more useful AI becomes, the more memory it needs. That has turned a once-cyclical industry into one of the most important bottlenecks in the AI economy.

Sometimes investing is complicated… This is not one of those times.

The AI infrastructure buildout is the largest technology investment cycle we have ever seen.

Companies and governments are pouring more than a trillion dollars a year into chips, data centers, power, cooling, networking, storage, and software to prepare for AI.

And that spending is accelerating. It has to.

We are moving closer to artificial general intelligence (AGI). The models are getting larger. The use cases are becoming more practical. Enterprises are moving from experimentation to deployment.

The world is not building less AI infrastructure next year. It is building more.

Don’t overthink this. Stick with the trend.

The Fed Just Killed the Phillips Curve

By Joe Withrow, Senior Analyst, Brownstone Research

Kevin Warsh was confirmed as the new Federal Reserve (Fed) Chairman on May 13. He replaced Jerome Powell, who had served as acting Fed Chair since February 2018.

In every Fed Chair’s inaugural press conference, the market tries to get a feel for the person’s views – are they hawkish or dovish?

The term hawkish refers to a preference for tighter monetary policy. That typically involves higher interest rates, reduced money supply, or a more aggressive stance against inflation—even if it risks slower economic growth or higher unemployment.

And the term dovish refers to a preference for looser, more accommodative monetary policy. It typically involves lower interest rates, increased money supply, or greater tolerance for inflation. The doves believe this will stimulate borrowing and spending throughout the economy.

So as he approached his first press conference a few weeks ago, the market wanted to know – is the new guy hawkish or dovish?

Well, it turns out that may have been the wrong question. In his first press conference as Fed Chair, Warsh made it clear that he is operating outside of the conventional framework entirely.

Along with nixing the idea of “forward guidance” and refusing to place an interest rate projection on the Fed’s “dot plot,” Warsh explicitly rejected the Phillips Curve.

The Phillips Curve is the doctrine that says there is an inverse relationship between unemployment and inflation. When unemployment is low, inflation tends to rise. And when unemployment is high, inflation tends to fall.

The implication is that a central bank cannot have sustained low unemployment and low inflation simultaneously. Instead, it must enact policy to find a happy medium between them.

The rationale underpinning the Phillips Curve is that economic growth and rising wages also cause inflation. Thus, the Fed must raise interest rates to stifle inflation when the economy “runs hot.” But by doing so, the Fed also curtails economic growth.

That’s been the operating framework of Fed policy for 50 years now. But not any longer…

Warsh called the Phillips Curve a “cruel choice”, and he declared it to be false. He argued that strong growth, robust employment, and low prices are each possible through productivity-led expansion.

This is why Warsh rejected the Fed’s previous practice of forward guidance as “Fed prophecy.” And he called on investors to focus on real economic data rather than words coming from a central planner’s mouth.

What we’re witnessing here is the outright repudiation of neo-classical Keynesian economics, which has been the dominant school of thought at the Fed and across Academia for over five decades now. I don’t think the markets realize just how big a deal this is yet.

For investors, there are three takeaways here.

First, the interest rate outlook here in the U.S. will be driven largely by market forces going forward. Warsh made it clear that he is not going to raise or cut rates based on the old Keynesian model.

This will create volatility at first as the market is forced to recalibrate its expectations. But it should lead to a more efficient market over time.

Second, the rejection of the Phillips Curve signals an end to the era of financial engineering as a means of growth. We can expect to see a renewed focus on the real economy going forward. Manufacturing, energy infrastructure, critical minerals — each will be structurally prioritized in the months and years ahead.

And finally, third, the idea that the Fed must cut interest rates to spark economic growth is going away.

Of course, lower rates are generally more conducive to economic growth… but they aren’t a prerequisite. Warsh made that abundantly clear.

So now we’re starting to see what Warsh meant when he promised “regime change” at the Fed. It’s not just about whether the Fed should cut rates or raise them. It’s about casting off the old Keynesian models and returning to classical supply-side economics.

As a result, the era of financial engineering will give way to a focus on investment in real assets and real productive activity.

More Volatility Ahead?

By Larry Benedict, Founder, Opportunistic Trader

In your update last week, we discussed the recent change in tone from the Fed. New Chair Kevin Warsh put inflation very firmly back on the agenda, adopting a more hawkish stance than his predecessor, Jerome Powell.

That certainly flies in the face of what the market was expecting at the start of the year. After three successive rate cuts in the back end of 2025, investors were factoring in at least another cut and possibly two by year’s end.

But the potential of a rate rise, coupled with stocks already stretched at sky-high valuations, has weighed on the market. While the massive hype building up to the SpaceX (SPCX) provided something of a distraction, the market’s mood has suddenly turned more sober…

After its post-IPO surge, SPCX has dropped back to around the same level as its first day of trading. And the much-anticipated OpenAI IPO – widely expected to list in the coming months – is now reported to be on hold, most likely until next year.

Plus, some of the AI highflyers – like Palantir (PLTR) and Oracle (ORCL) – have come back to Earth after spectacular runs. Investors have become more circumspect about which AI stories they’ll buy into.

However, the other thing I’m watching closely is the algo trading that drove much of the rally these past couple of years…

One of the defining features of this rally has been the growing influence of momentum-based algos. Unlike discretionary traders who weigh up valuations, earnings, or economic data, these models are basically designed to follow price.

When stocks are rising, they tend to buy in and/or add to winning positions, thereby reinforcing the trend and helping drive markets higher. But momentum works both ways…

If enough selling pressure begins to build, those same algorithms can quickly switch from buyers to sellers. And rather than cushioning any selloff, they can amplify it as trend signals deteriorate and positions are unwound.

That’s why markets can sometimes transition from a calm, orderly rally to a sharp bout of volatility in a surprisingly short period of time. When momentum breaks down, the very strategies that fueled the rally can end up accelerating the decline.

That could set off a period of heightened volatility. And with premiums correspondingly picking up, that’s laying the foundations for a potentially lucrative second half of the year.

I think folks could be in for a real surprise at just how quickly things may change…

More stories like this

Read the latest insights from the world of high technology.

-

-

The Biotech Winter Finally Thaws

The resurgence in both IPO activity and M&A transactions may mark the beginning of what I believe will be...

-

Kevin Warsh: Hawk

Clearly, rate expectations are changing. That means we’re in for an interesting second half of the year.