Kevin Warsh: Hawk

Clearly, rate expectations are changing. That means we’re in for an interesting second half of the year.

The resurgence in both IPO activity and M&A transactions may mark the beginning of what I believe will be the strongest biotech bull market in history.

Editor’s Note: “There’s nothing like a biotech golden age.” That’s the message from Jeff Brown. And as you’ll see below, Jeff believes that golden age has finally arrived. To help readers prepare, he’s hosting a special event this Wednesday, July 1 at 8 p.m. ET. What is kicking off this new bull market? And which stocks should you own ahead of the next run higher? Jeff will answer everything on Wednesday. Reserve your seat with one click right here.

By Jeff Brown, Founder & CEO, Brownstone Research

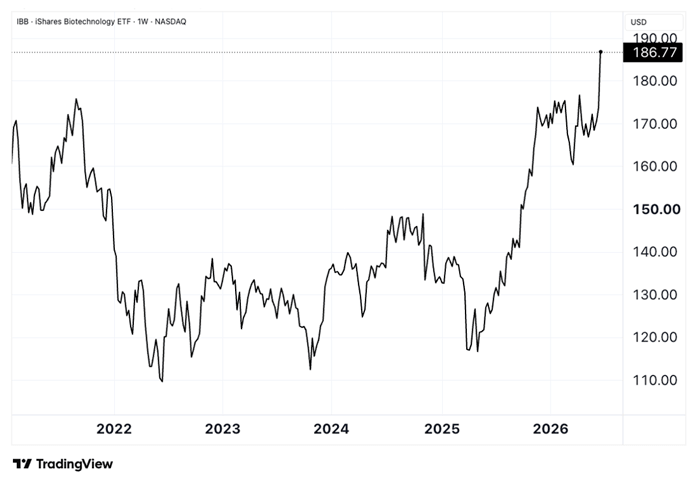

The biotech winter has finally thawed…

For years, the biotechnology markets were plagued by rising interest rates, weak investor sentiment, and limited access to capital.

As measured by the iShares Biotechnology ETF (IBB), we can clearly see the onset of winter in early 2022 as well as the apathetic price action in the years that followed.

But the chart also shows something else. The biotechnology sector has shown clear signs of recovery over the past six months.

Investors have become more willing to fund promising drug developers, while large pharmaceutical companies have increased their appetite for acquisitions.

As a result, both biotech initial public offerings (IPOs) and merger-and-acquisition (M&A) activity have accelerated, particularly among companies with late-stage clinical programs and strong scientific data.

Earlier this month, cancer-focused Parabilis Medicines (PBLS) made headlines with one of the largest biotechnology stock market debuts in years.

The company raised approximately $670 million through its initial public offering, and an additional $75 million strategic investment from Regeneron (REGN) brought the total financing to roughly $745 million.

Investor demand was so strong that the company increased the size of the offering and priced its shares above the expected range. On its first day of trading, the stock surged more than 50%, making it one of the most successful biotech IPOs of the year.

The transaction also demonstrates that the public markets are reopening for high-quality biotech companies after several years of limited IPO activity.

This year, there have been 17 healthcare-related IPOs, which raised a combined $5.5 billion with an average first three-month return of 30%.

At the same time, large pharmaceutical companies are actively pursuing acquisitions to strengthen their future growth prospects.

Many established drugmakers face looming patent expirations on blockbuster medicines and are looking to replenish their pipelines through strategic acquisitions.

This trend has fueled several significant biotech transactions, including GlaxoSmithKline’s (GSK) recently announced $10.6 billion acquisition of Nuvalent (NUVL), a company developing targeted therapies for lung cancer.

While risks remain and market conditions can change quickly, recent transactions indicate that investors and pharmaceutical companies continue to place significant value on innovation, particularly in areas with high unmet medical needs such as cancer and cardiovascular disease.

The resurgence in both IPO activity and M&A transactions may mark the beginning of what I believe will be the strongest biotech bull market in history. And I’d like readers to be ready for it…

That’s why, on Wednesday, I’m hosting a special event where I’ll lay out my full thesis for the new biotech bull market as well as the small biotech companies I believe have explosive potential.

We’re calling the event simply The Biotech Moment, and I think it’d be worth your while to attend.

You can reserve your seat with one click right here.

By Jason Bodner, Founder, Outlier Intel

In 1892, a German surgeon named Julius Wolff made a fascinating discovery…

Bones aren’t a static structure, they are alive. When subjected to stress, tiny, microscopic fractures form. But instead of just healing, the bones rebuild denser and stronger than before.

Orthopedic surgeons still call it Wolff’s Law: Bones that never face stress become weak. Bones that do become stronger.

The technology sector just experienced its own version of Wolff’s Law.

From the March low to the June 2 peak, the Nasdaq Composite rallied more than 30% in roughly 60 trading sessions.

Markets don’t move in straight lines forever. Every strong advance eventually needs a pause. Gains get digested, and some enthusiasm gets shaken out.

That’s healthy and necessary. Last week, that’s exactly what happened.

The Nasdaq Composite pulled back roughly -6.4% from its recent high, while the Nasdaq 100 slipped about -4%.

Right on cue came the fear and explanations. AI enthusiasm is fading. Valuations are stretched. Inflation remains stubborn. The Strait of Hormuz, which looked settled two weeks ago, is back in the headlines after a cargo ship was struck near Oman, briefly sending Brent crude back above $80.

Every correction comes with a brand-new reason why this time is different.

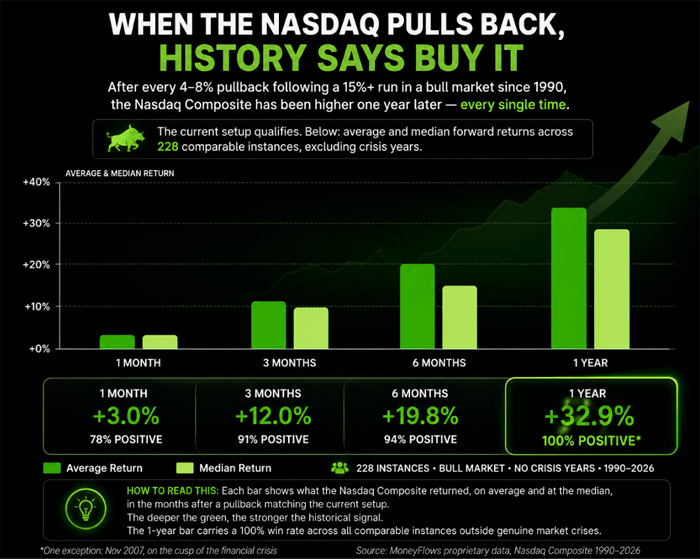

The data disagrees.

Looking at similar setups, since 1990, the Nasdaq has experienced 228 pullbacks between 4.5% and 8% after previously rallying at least 15%, excluding genuine crisis periods. Last week’s setup fits that pattern almost perfectly.

What followed those moments is worth sitting with…

One month later, the Nasdaq was higher 78% of the time, averaging about 3%. Three months later, positive 91% of the time, averaging roughly 12%. Six months out, the win rate climbed to 94%, with average gains approaching 20%.

And one year later?

Across all 228 instances, the Nasdaq finished higher every single time, averaging nearly a 33% return.

Not 90%. Not 95%. One hundred percent.

This is not a guarantee. It’s a historical baseline. And there’s one more historical lens worth adding here.

2026 is a midterm election year. Midterm years have the worst reputation in the four-year presidential cycle, averaging just 5.8% total returns since 1926 and punishing intra-year drawdowns averaging 16%. The first nine months tend to be choppy, frustrating, and full of reasons to give up.

Sound familiar?

But here’s what the crowd consistently misses. Once election uncertainty recedes in the fourth quarter, midterm years historically snap back hard.

Since 1926, the S&P 500 has averaged a 7% gain in Q4 of midterm years alone, with an 88% positivity rate. And since 1950, the market has averaged a 36% one-year forward return off its midterm year lows.

Wolff’s Law says stressed bones only grow back stronger. History says the same about bull market pullbacks.

Bend, don’t break.

By Larry Benedict, Founder, Opportunistic Trader

With all the excitement around American stocks, few investors have noticed something nearly unprecedented happening with the Japanese yen…

In sum: Relative to the dollar, the yen is the weakest it’s been in 40 years. And it could be a major problem for the country’s economy.

Japan is a huge importer of commodities—in particular, oil and other fossil fuels. For that reason, it’s particularly susceptible to inflation when the price of those commodities surges.

We’ve witnessed that with the conflict in the Middle East choking off vital supplies. In a nutshell, the weaker the yen becomes, the higher the cost of those raw inputs and the more inflation ramps up.

To protect the yen, the Bank of Japan (BoJ) has previously staged interventions by buying the yen and selling the USD (and/or other currencies).

The BoJ is very adept at this. It strikes with sufficient volume at vulnerable price levels to set off a sizable correction, like we saw in April.

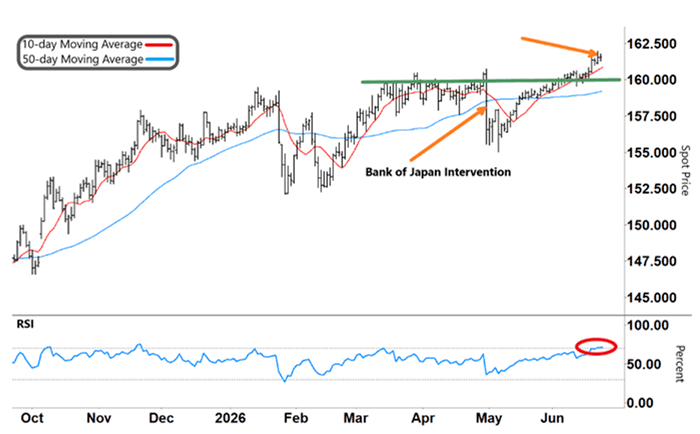

While it’s not a hard line, the 160 area (horizontal green line on the chart below) has attracted the attention of Japanese authorities.

Source: e-signal

As you can see, the BoJ’s intervention—the first since July 2024—caused a sharp reversal in USD/JPY.

In short, it seemed to work. The yen strengthened…for a bit. But what the chart also shows is that USD/JPY has only gone higher from there. It’s now at the highest level since 1986.

Nevertheless, this up move looks overstretched, and could be due for a pullback.

As you can see, the peak on Monday coincided with the Relative Strength Index (RSI) heading into overbought territory (red circle). Plus, the USD/JPY is pushing towards 162—the upper end of the BoJ’s prospective intervention level.

Beyond the price action, there are other factors to consider…

New Fed Chair Kevin Warsh took a more hawkish tone at last week’s meeting. He’s put managing inflation at the top of the agenda.

Nine policymakers now anticipate a rate increase by year’s end. Meanwhile, eight others think rates will remain unchanged, and one still predicts a cut. (Warsh refrained from making a projection.)

My take is that Warsh clearly wants to keep inflation under control, but he’ll also be reluctant to raise rates unless forced to by economic data. Once the markets process that nuance, it might take some of the recent heat out of the USD.

On the flipside, the BoJ recently raised rates to 1.0%, and now it is considering moving rates higher again. While it’s still a relatively low rate compared to the U.S., it’s a significant shift for a country that had negative rates up until March 2024. If those rates continue to tick higher, it will gradually pull in more global investors, adding support to the yen.

USD/JPY may be at multidecade highs, but perhaps not for long.

Read the latest insights from the world of high technology.

Clearly, rate expectations are changing. That means we’re in for an interesting second half of the year.

The market isn't waiting for diplomats to finalize every detail.

Second-quarter reporting season begins in earnest in mid-July…