Don’t Fall for the Semiconductor Selloff

SMH fell 6.4% in the three days following the Kimi K3 release. Here’s why you shouldn’t worry…

When investors say an industry is dead, what they often mean is that the weakest participants are dead.

Editor’s Note: Welcome to First Signal, the only publication where subscribers can access the collective expertise of our entire analyst team in one place. Every Monday, Wednesday, and Friday, we’ll share three focused insights – the stories and data you need to make the most of the trading day ahead. Expect to read new insights from Jeff Brown, Larry Benedict, Jason Bodner and our handpicked pool of analysts in the weeks ahead. And if you haven’t already, be sure to catch up on your free special report, The First Signal Forecast, right here.

By Jason Bodner, Founder, Outlier Intel

Over the past year, software stocks have been taken behind the woodshed.

Investors looked at ChatGPT, Claude, Gemini, and a growing army of AI agents and asked a reasonable question: if artificial intelligence can write code, build applications, automate workflows, and answer questions, what happens to the software companies selling those tools?

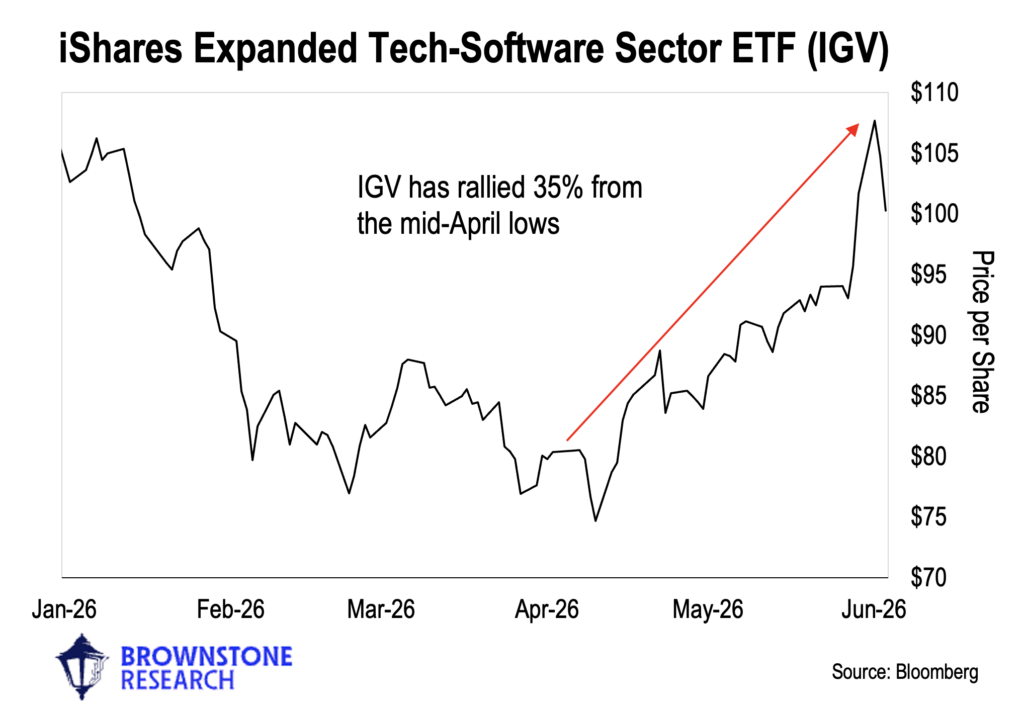

The market’s answer was swift. The iShares Expanded Tech-Software ETF (IGV) fell approximately 30% from January to mid-April.

The fear wasn’t completely irrational. Every few weeks seemed to bring another demonstration showing AI performing tasks that previously required skilled professionals.

One week AI was building websites. The next it was writing software. Then it was generating reports, creating presentations, and analyzing data.

The conclusion many investors reached was simple: if AI can do the work, software companies become less valuable.

Software was dead.

But it wasn’t.

As I write, IGV has rallied approximately 35% from its mid-April lows.

When investors say an industry is dead, what they often mean is that the weakest participants are dead.

Those are two very different things.

After the dot-com crash, investors didn’t simply abandon speculative internet companies. Many concluded the internet itself had been a bubble. Thousands of businesses disappeared, billions of dollars were lost, and countless careers were derailed.

But the internet survived.

More importantly, the strongest companies emerged stronger than ever. Amazon, Google, and a handful of other winners became some of the most valuable businesses in history.

Software may be facing its own version of that test today.

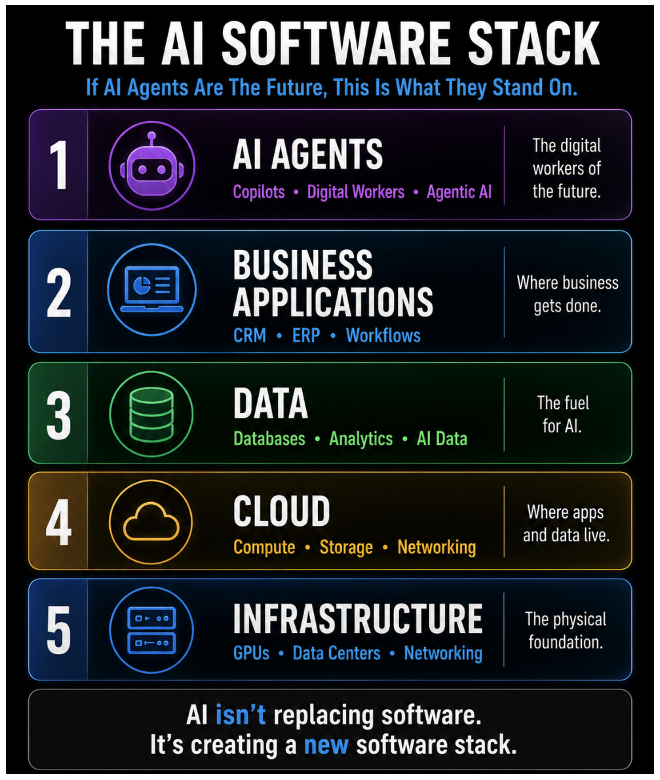

The reality is that AI still needs software. And the easiest way to understand what’s happening is to think in layers.

At the top are AI agents, the digital workers grabbing all the headlines. Beneath them sit the business applications where actual work gets done. Below that is the data layer, because AI without data is useless.

Underneath sits the cloud infrastructure that stores, processes, and delivers information. And beneath everything is the physical infrastructure: the data centers, GPUs, networking equipment, and power systems that make the entire stack possible.

In other words, AI isn’t eliminating the software ecosystem.

It’s creating a new one.

An AI agent doesn’t magically appear and start creating value.

It needs data. It needs workflows. It needs security. It needs cloud infrastructure. It needs systems that connect departments, customers, employees, and information.

Those functions aren’t disappearing.

They’re being augmented.

The software companies that merely stored information may struggle. The software companies that help organizations make decisions, automate processes, and orchestrate work could become more valuable than ever.

If history is any guide, the biggest winners of the next decade may emerge from the very industries investors are most eager to write off today.

By Jeff Brown, Founder, Brownstone Research

During NVIDIA’s earnings call, CEO Jensen Huang said: “Demand has gone parabolic.”

We can’t argue with that.

Consensus expectations already call for NVIDIA to double revenue over the next two years. That sounds aggressive.

But given what we are seeing from the hyperscalers —Amazon (AMZN), Google (GOOG), Meta Platforms (META), Microsoft (MSFT), and Oracle (ORCL) —I believe those forecasts will continue moving higher.

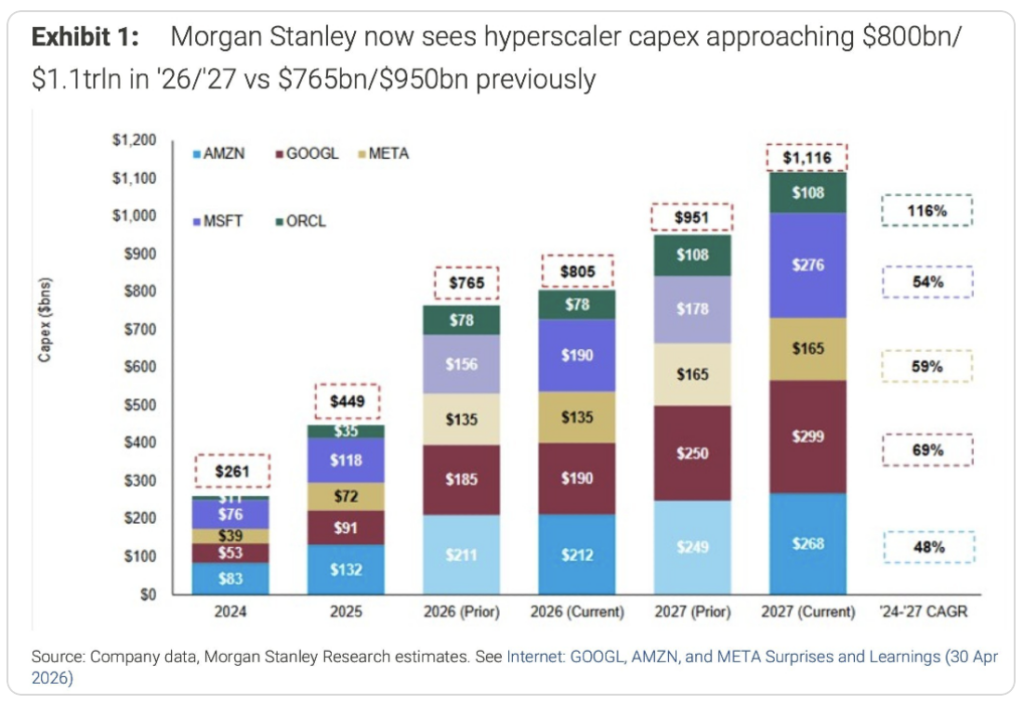

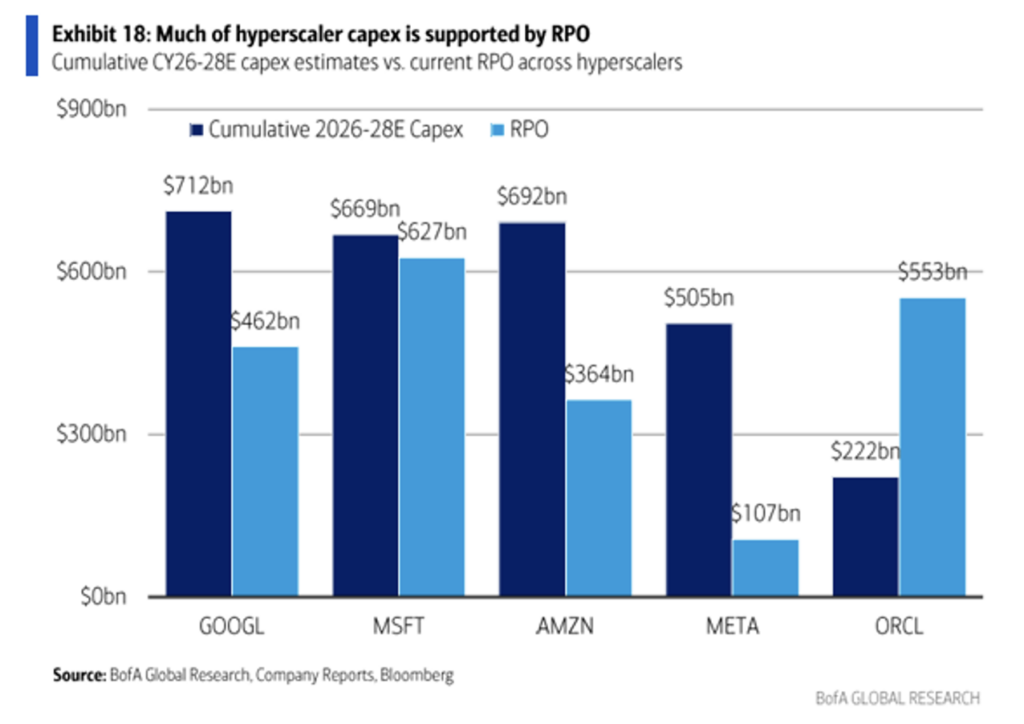

Morgan Stanley recently revised its forecasts for AI infrastructure spend in 2026 and 2027, raising its 2027 hyperscaler capital expenditure estimate by $165 billion compared with its prior forecast. That new estimate is also roughly $350 billion above where consensus expectations were at the beginning of the year.

The two middle bars in the chart below show the 2026 prior forecast and current forecast. And the two bars on the right do the same for 2027.

And what really matters is not just that the numbers are going up. It’s that they are going up because the demand is already there.

These companies are not spending hundreds of billions of dollars on speculative future demand. They are building because customers are already committing to buy the capacity.

The next chart shows cumulative hyperscaler capital expenditures from 2026 through 2028 in the dark blue bars. The light blue bars show remaining performance obligations (RPO). This represents revenue customers have already committed to spend in the future.

As we can see, the hyperscalers have substantial RPO to justify this buildout. Meta is the exception because it uses much of its compute internally to support its own advertising systems and consumer applications. But for the other hyperscalers, the picture is clear. Future customer commitments already support a massive portion of the infrastructure spending.

They are building in response to overwhelming demand for AI.

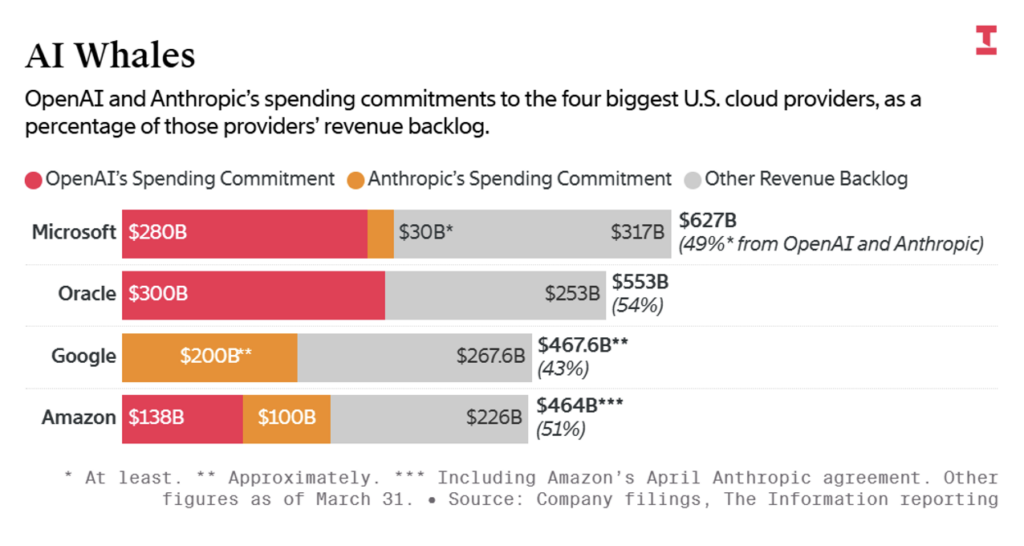

And the biggest clients of those computational resources are the major AI labs, OpenAI and Anthropic. As of the end of April, OpenAI and Anthropic combined make up nearly half of the future revenue of Google, Microsoft, Amazon, and Oracle.

Yes, that represents a significant level of customer concentration. But that is exactly what makes this so important. These hyperscalers are not reckless.

They have visibility into demand that most investors will never see. They know which customers are consuming compute. They know which models are scaling. They know which AI companies are likely to need more capacity in the future.

In other words, the hyperscalers are effectively underwriting the next phase of AI growth.

By Nick Rokke, Senior Analyst, Brownstone Research

On Monday evening at Computex, NVIDIA CEO Jensen Huang answered the question AI skeptics have been asking for the last three years: When does AI actually become useful?

According to Huang, the answer is “right now.”

The first phase of AI was about chatbots. We typed in a prompt. The model responded. It was impressive… but still mostly passive.

Then came reasoning models. These systems could think through more complex problems, break tasks into steps, and help with deeper research.

Now we’re entering the next phase: autonomous AI agents.

These agents don’t just respond. They act. They write code, search databases, generate reports, manage workflows, and interact with other software tools. And unlike human workers, they don’t stop at 5 p.m.

That’s the inflection point.

AI has moved beyond experimentation. It is now mature enough to be deployed widely for practical, revenue-generating work.

This is why tokens matter so much.

Tokens are like the fundamental building blocks for an AI model. They’re what allows the model to break down text, understand the user’s intent, and take an appropriate action. The more tokens an AI has available to it, the more useful it can be.

Tokens have mostly been used as a technical measurement. But with agentic AI coming online, tokens are revenue. And if tokens are revenue, then compute becomes the factory floor of the AI economy.

The more compute a company can access, the more tokens it can generate. The more tokens it can generate, the more revenue it can produce.

That is why NVIDIA’s customers don’t really want to buy computers anymore. As Huang put it, they want to build “AI factories.” These factories turn electricity, chips, networking, and software into intelligence.

And as these AI factories get larger, the architecture inside them changes.

That brings us to Marvell (MRVL).

At Computex, Huang appeared alongside Marvell CEO Matt Murphy and said Marvell could become “the next trillion-dollar company.” His reasoning was clear: Marvell’s networking and connectivity technology is becoming essential to the future of AI data centers.

Most investors still think this race is only about GPUs. It isn’t.

GPUs are the engines. But those engines need to communicate across servers, racks, campuses, and eventually geographically distributed data centers. The larger the AI model, the more important connectivity becomes.

That’s Marvell’s specialty.

As compute performance increases, the bottleneck shifts to moving data faster, with lower latency, less power, and greater efficiency across the entire AI factory. NVIDIA knows this. That’s why it invested $2 billion in Marvell as part of a strategic partnership around NVLink Fusion, custom XPUs, scale-up networking, and silicon photonics.

The market responded by sending MRVL shares 40% higher in the days following the announcement.

As AI moves from chatbots to always-on agents, compute demand will explode. But the next wave of winners won’t be limited to the companies making GPUs. The next fortunes will be made in the infrastructure that lets millions of accelerators function like one giant computer.

That’s why Huang is focused on Marvell.

None of this should be a surprise to subscribers of The Near Future Report. We bought Marvell a year ago for this exact reason. Now our subscribers are up 173% on this position… And if Jensen is right about his prediction, this could become a 10-bagger for us.

Read the latest insights from the world of high technology.

SMH fell 6.4% in the three days following the Kimi K3 release. Here’s why you shouldn’t worry…

This chart is a tried-and-true gauge of crypto’s risk appetite…

The selling in technology and semiconductor names over the past several weeks has been violent. That type of behavior...