The AI Standards Body That Shouldn’t Exist

Imagine if a small number of elites – with tight coordination with the U.S. government – had a chokehold...

This is one of my favorite setups as a long-term investor…

As strange as it sounds, a stock can rise 50%, 100%, or more and become cheaper at the same time.

This is one of my favorite setups as a long-term investor. It happens when a company’s profits grow faster than its share price. The price chart looks expensive, the price action shows an overextended stock, but the business becomes a better value with every upward revision to earnings.

This shows that investors remain skeptical of the company’s growth. But the disconnect of the stock getting cheaper rarely lasts for long. Eventually, reality sets in… And if the trend underlying the growth is strong enough, this setup gives investors huge future returns.

To show this, we’ll look at the forward EV / EBITDA ratio. This ratio tells us how much investors are paying for each dollar of next year’s expected EBITDA (earnings before interest, taxes, depreciation, and amortization). When the ratio falls, the stock is getting cheaper relative to its earnings power.

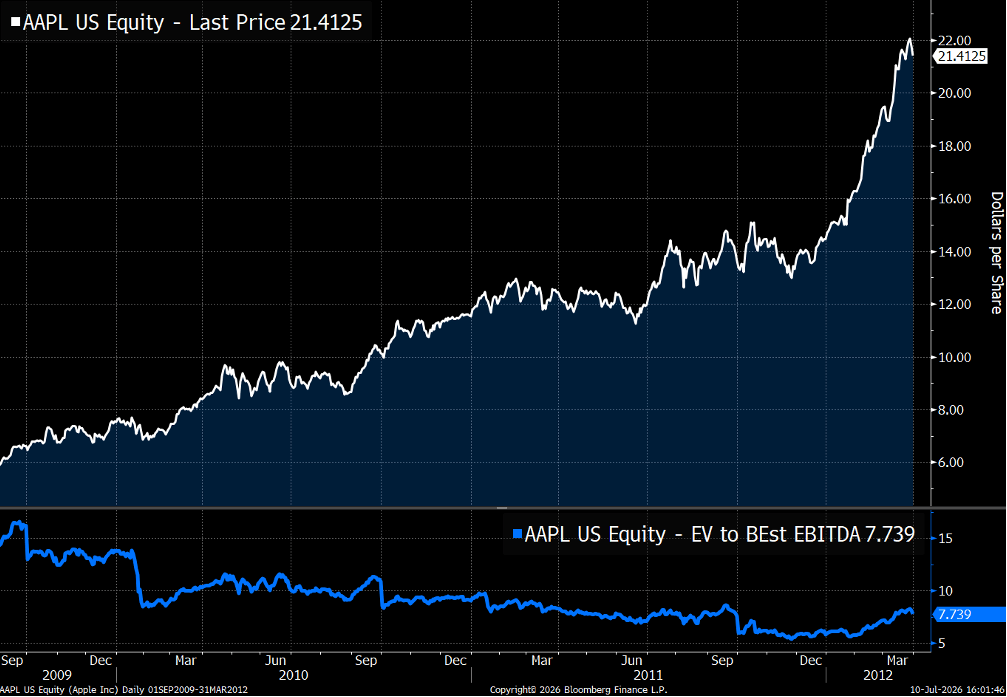

Apple (AAPL) gave us a textbook example. From September 2009 through March 2012, shares climbed from a split-adjusted $5.90 to $21.41. That was a 263% gain in just 30 months.

Yet Apple’s forward EV/EBITDA multiple fell from 14.3 to 7.7 over the same period.

Source: Bloomberg

Apple was a better value at $21 than it had been at $6.

The reason was visible in the business. Apple had released the iPhone 3GS just months earlier, and adoption was accelerating. The original iPhone sold 1.4 million units. The iPhone 3G and 3GS sold 31 million units combined. The iPhone 6 generation went on to sell 220 million units.

Most investors were focused on how far the shares had already risen. The best investors were focused on how large the smartphone market could become… and how central Apple would be to it.

In the 14 years that followed, Apple’s stock rose more than 13-fold.

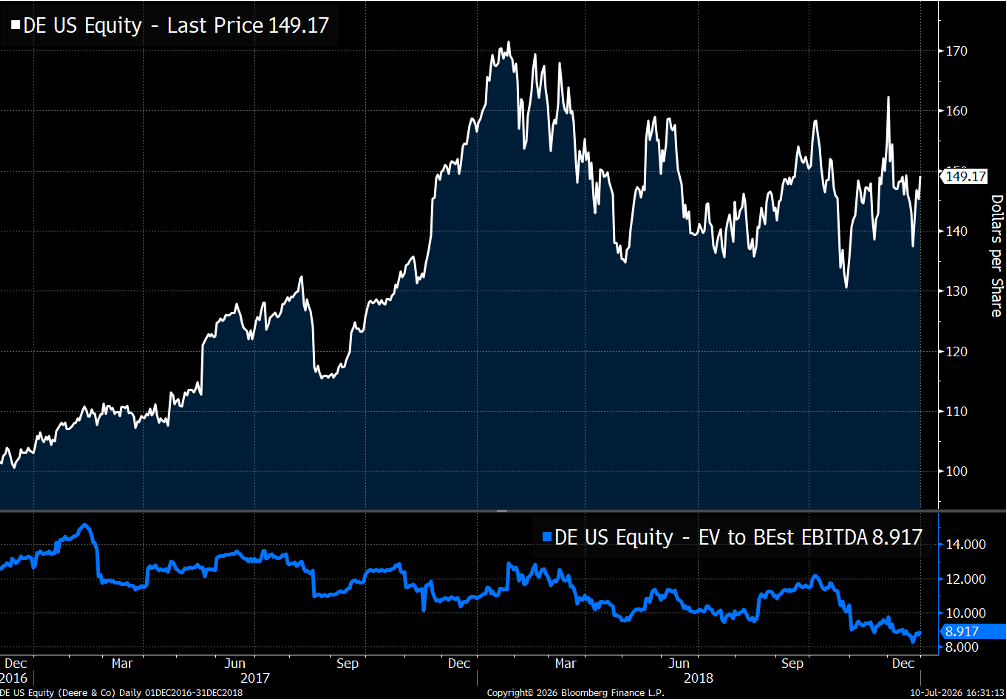

The same pattern appeared in Deere & Co. (DE). From December 2016 through the end of 2018, Deere shares gained nearly 50%. But its forward EV/EBITDA multiple dropped from 12.7 to 8.9.

Source: Bloomberg

Deere went on to rise another 300%. The market still viewed it as a cyclical farm-equipment manufacturer. In reality, Deere was becoming a precision agriculture, robotics, and data platform.

And as both Deere and Apple rose during these times, investors began to call these stocks expensive. And warned against owning them.

Today, we are seeing the same setup across many companies powering the AI infrastructure buildout. And for savvy investors, this could be a great opportunity to add these companies to your portfolio.

Every day, headlines warn that the AI infrastructure boom is approaching its limits. The concern is straightforward. Hyperscalers are spending hundreds of billions of dollars a year on data centers, GPUs, networking equipment, and power systems.

Yet the revenue generated by AI applications still appears small compared with the capital being deployed.

That gap has created fears that returns will disappoint, spending will slow, and today’s enormous order books will disappear.

Then there are the physical constraints. New data centers require electricity, land, transformers, grid connections, and water or other cooling systems. In many regions, those resources are already scarce. Permitting battles, local opposition, and rising power costs are delaying projects.

Yet week after week, the largest technology companies are responding by committing more capital – not less.

Just last week, Meta (META) said it expects to have deployed 7 gigawatts of computing capacity this year and to double that to 14 gigawatts next year. That pushed analysts’ assumptions for 2027 capital spending from $180 billion to $235 billion.

Microsoft (MSFT) and Amazon (AMZN) announced new multibillion-dollar data center projects in Texas and Missouri, respectively.

Brookfield expanded its financing framework with Bloom Energy (BE) from $5 billion to $25 billion. The capital will support rapidly deployable, on-site power systems for hyperscale data centers.

And Anthropic signed a 20-year agreement worth $19 billion with TeraWulf for access to as much as 401 megawatts of compute capacity.

New billion-dollar deals are announced every week, and yet we still have skeptics. They argue that capacity reservations may be double-counted. They question whether AI labs will earn enough to support their commitments. And they point out that many announced data centers do not yet have firm access to power.

All points sound convincing, but none of this will stop the advancement and adoption of AI. But this skepticism is giving us an opportunity….

$115 trillion is about to move into one small corner of the market. Jeff Brown has spent months tracing exactly where it's headed, and he's narrowed it to five overlooked assets he believes sit right in its path. Including one the Trump family itself already holds a six-figure position in. He calls what's coming the “Trump 90-Day Melt Up.” And if you missed Bitcoin at $240, it could be a rare second chance to be early to something historic. Jeff reveals where it all begins, completely free. Click here now, while you're still ahead of it.

When OpenAI goes public, millions of emotional investors will rush to buy shares at any price. "Market Wizard" Larry Benedict says that's exactly what Wall Street insiders are counting on... because IPO days are a rigged game. His IPO profit trick? Don’t buy the stock. All you have to do is place ONE five-minute trade on IPO morning to potentially collect $321, $1,605, or even $3,210 (or more) the same day, whether the IPO soars or sinks. Larry shares his 5-Minute IPO Profits strategy HERE for free.

The market’s skepticism is now showing up in valuations. That is creating the setup I described at the beginning: share prices are rising, but the stocks are getting cheaper.

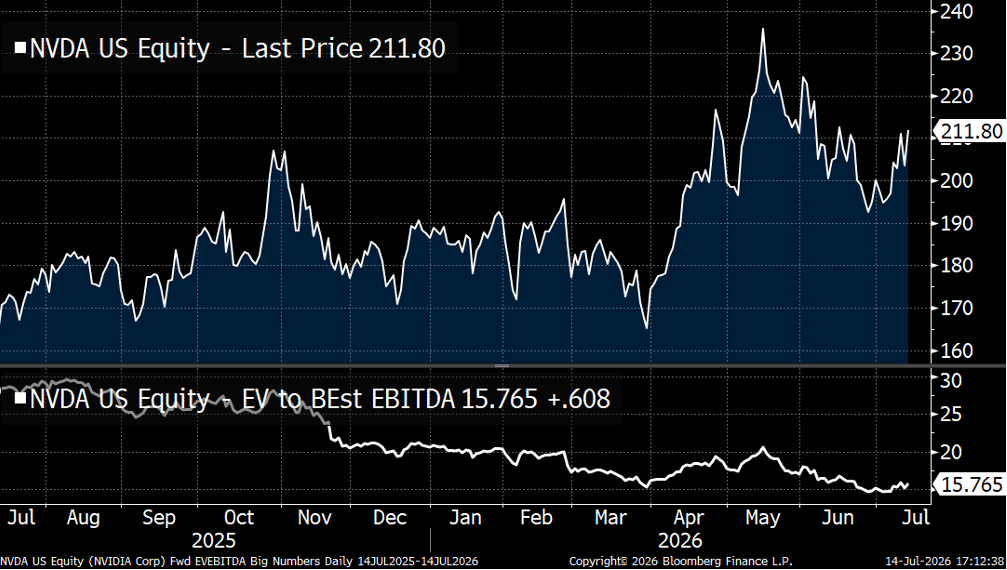

Start with Nvidia (NVDA). Over the past year, Nvidia shares rose 28%. Yet its forward EV/EBITDA multiple fell nearly 50%, to about 15.8 times.

That is a compelling valuation for a company expected to double EBITDA this year and grow it another 50% next year. Wall Street sees a stock that has already run. The numbers show a business that is still outrunning the stock.

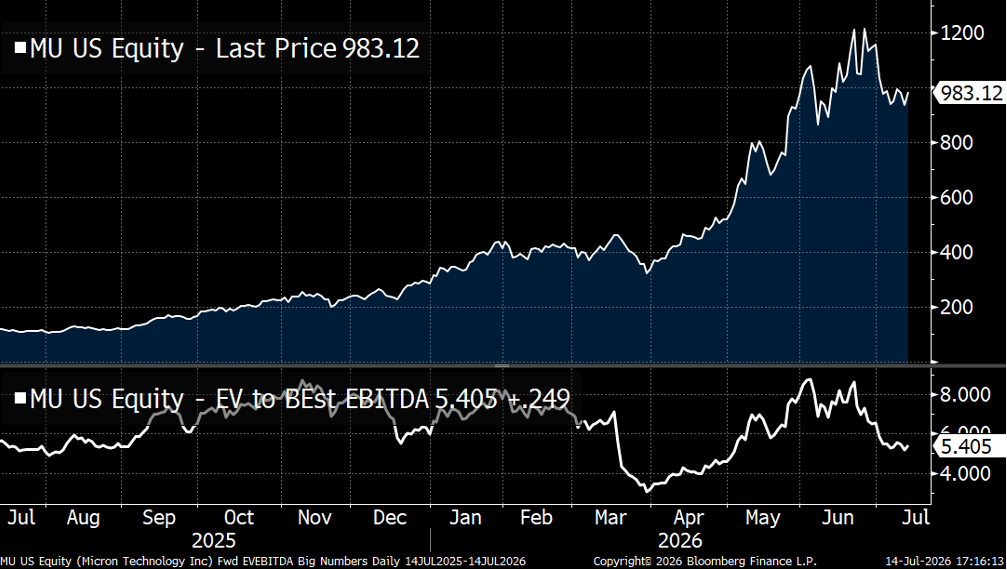

Then there is Micron (MU). Near Future Report subscribers are up 730% on Micron over the past year. Yet the company’s forward EV/EBITDA multiple is roughly unchanged at about 5.4 times.

That is a ridiculously low multiple for a company experiencing this level of demand, pricing power, and margin expansion.

Now some analysts say we shouldn’t use forward earnings in analysis like this because they are only “guesses.” And not known. But remember, Micron’s DRAM is sold out through 2027, and that’s 71% of their business. Micron’s forward earnings are known.

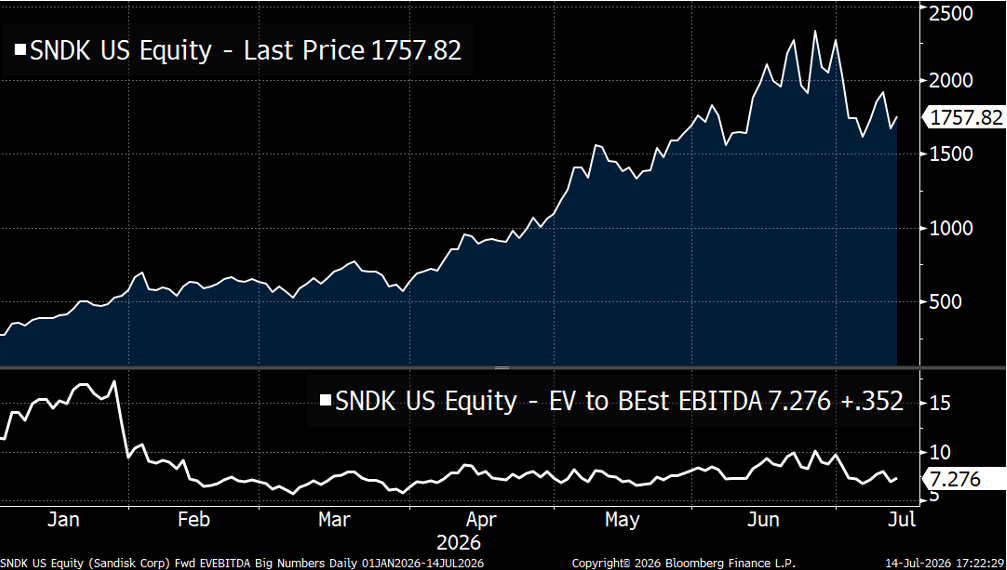

Another memory company, Sandisk (SNDK), shows the same pattern. Its shares have quadrupled so far this year, while its forward valuation has been cut roughly in half to about 7.3 times.

Look only at the price chart, and Sandisk appears expensive. Look at the earnings multiple, and the stock is cheaper than it was before the rally.

These are some of the most visible beneficiaries of the AI buildout. Yet relative to expected operating profits, they are cheaper than they were before the latest leg of the rally.

The market is making a basic mistake. It is treating a rising price as proof of overvaluation. But price alone tells us nothing about value.

A rising stock can be cheap. A falling stock can be expensive.

The question to ask is, “Are the company’s earnings rising faster than the price?”

AI infrastructure is not a normal product cycle. Artificial intelligence will completely change how we work and how we spend our leisure time in the future.

And along with this revolutionary technology comes a multiyear – likely multi-decade –buildout of a new global computing stack. This includes semiconductors, memory, networking, power, cooling, land, and data centers. All of which are bottlenecks to the advancement of AI at this point.

The companies controlling those bottlenecks can compound revenue and profits for years.

That does not mean every AI stock is attractive. It means the best businesses should be judged against their future cash generation, not the distance they have traveled on a chart.

So when someone says AI is in a bubble simply because the stocks are up, just nod and smile. Then look at earnings.

Right now, in several of the most important AI names, earnings are rising faster than share prices.

This is an opportunity for investors to make outsized returns in the coming months and years.

Regards,

Nick Rokke

Senior Analyst, Brownstone Research

Read the latest insights from the world of high technology.

Imagine if a small number of elites – with tight coordination with the U.S. government – had a chokehold...

We have spent the last two years focused on the obvious AI constraints: semiconductors, high-bandwidth memory, networking equipment, and...