The Bigger Picture Hasn’t Changed

Sometimes the smallest forces, the ones almost nobody notices, end up making the biggest difference. Investing works much...

The people who wanted out have sold. The hedgers already hold their downside insurance. And there is simply less fear left to price in, even at lower prices…

Editor’s Note: Forbes is warning of an “IPO tsunami,” with more than 800 companies lined up to go public. But “Market Wizard” Larry Benedict warns the riskiest move is buying the stock on IPO day.

Over the last 40 years, he’s perfected a simple five-minute trade he’s used to profit on more than eight out of 10 IPO days… without buying a single share of stock.

This coming Wednesday, July 15, at 8 p.m. ET, he’s revealing exactly how to potentially pocket $321, $1,605, or even $3,210 or more on IPO days.

Click here to add your name to Larry’s guest list automatically, 100% free.

By Feruz Kurbanov, Senior Analyst, Brownstone Research

Vijay Kumar is stepping down as the acting head of the FDA’s Office of Therapeutic Products (OTP). That may not seem like a major headline at first.

Yet this office oversees the review of gene therapies, cell therapies, and other advanced medicines, making it one of the most important divisions for the future of biotechnology.

And when viewed alongside everything that has happened at the FDA over the past six months, Kumar’s departure appears to be part of a much larger transformation.

The changes at the FDA began earlier this year with the departure of Dr. Peter Marks, who had become one of the agency’s biggest supporters of gene therapy. During his leadership, the FDA worked closely with companies developing treatments for rare diseases and often showed flexibility when reviewing promising new medicines.

After he left, Dr. Vinay Prasad took on a larger leadership role and introduced a more cautious approach. He emphasized stronger clinical evidence and, whenever possible, preferred larger and more traditional clinical trials before approving new treatments.

That shift created uncertainty across the biotechnology industry. Several companies developing gene therapies, including REGENXBIO (RGNX), uniQure (QURE), and Sarepta Therapeutics (SRPT), found themselves facing unexpected regulatory questions or delays.

Some companies said the FDA’s expectations had changed compared with earlier meetings, making it harder to predict what would be required for approval. Investors naturally became concerned that the regulatory path for advanced therapies had become less predictable.

More recently, however, the picture has started to improve. The FDA has worked with several companies to clarify regulatory pathways, reopen discussions after earlier setbacks, and provide more direction on what evidence will be needed for approval. (Notably, Prasad left the FDA back in April.)

While the agency continues to expect strong scientific data, it also appears to be working toward giving companies a clearer and more consistent review process. This suggests the FDA is trying to strike a balance between maintaining high standards and helping important new treatments reach patients more efficiently.

Against this backdrop, the departure of Vijay Kumar – whom Prasad originally promoted to OTP’s acting head – looks less like an isolated event and more like another step in the FDA’s broader reorganization. The agency is preparing for a future in which many more advanced medicines will be reviewed.

Technologies such as CRISPR gene editing, cell therapies, RNA medicines, and other genetic treatments are rapidly moving through clinical development, and the FDA will need an organization that can efficiently evaluate the growing number of applications while keeping scientific standards high.

For investors, the most important question is not why Kumar is leaving but who will be chosen to replace him. The background and experience of the next leader could provide valuable clues about the FDA’s long-term direction.

Overall, the recent leadership changes should not necessarily be viewed as a negative sign for biotechnology. Instead, they may represent an agency adapting to one of the biggest scientific revolutions in modern medicine.

Although periods of change can create short-term uncertainty, a more stable and predictable regulatory system could ultimately benefit both patients and the biotechnology industry as more innovative treatments move toward commercialization.

By Ben Lilly, Senior Crypto Analyst, Brownstone Research

This is how market bottoms are born.

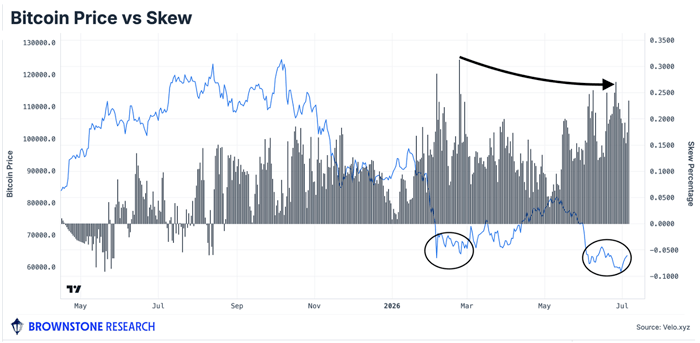

Last week was full of chaos. Stocks, commodities like gold and oil, and digital assets such as Bitcoin all experienced strong selloffs. But amid the fire sale, a signal emerged from the one place most people never look: the Bitcoin options market.

Regular readers of First Signal will remember a metric known as 25-delta skew; we first covered it last month. In short, skew measures the amount of fear in the options market.

When traders are bearish, they pay significantly more for puts. They’re willing to pay a premium because they believe that prices will turn lower, making the options more valuable. This outsized demand for puts versus calls pushes skew higher.

What’s notable here is that Bitcoin made a new year-to-date low last week when it briefly slipped below $58,000. But put skew did not match the price action. We saw a lower low in price but a lower high in fear.

As the chart below shows, the last high for skew was around the 30% range. Bitcoin was near $60,000 at the time. Then last week, skew briefly touched the 25% level before dropping back below 20% to close out the week. Meanwhile, Bitcoin’s price broke down below $60,000.

This is known as a bullish divergence. It tells us sellers are getting exhausted. The people who wanted out have sold. The hedgers already hold their downside insurance. And there is simply less fear left to price in, even at lower prices. The downside trade is getting crowded.

It also tells us that savvy money, professional traders, and institutions are taking advantage of this overheated skew to sell pricey put protection to the market.

The price action is backing up this view. After last week’s skew spike, Bitcoin’s bounce off the low was sharp and fast, with it immediately trading over 10% higher into the weekly close. That is a textbook reaction after a bullish divergence. It’s the mark of seller exhaustion and fresh money soaking up supply.

The timing could not be better. As we covered recently in Friday’s Chain of Thought, crypto’s biggest catalyst – The CLARITY Act – may finally get its verdict in July. As a reminder, this long-awaited bill will give the digital asset industry regulatory clarity on how it can operate in the United States.

Over the holiday weekend, the Major County Sheriffs of America (MSCA) dropped its opposition and moved to neutral on a key law enforcement provision. And then the National Organization of Black Law Enforcement Executives (NOBLE) went ahead and endorsed the bill. Two organizations shifted their stance just before the final text is set to drop this week. As a result, the odds for CLARITY to pass have started to trend higher.

Congress is set to return from its break on July 13, so we’ll see if it can also reach an agreement on the crucial ethics provision.

As always, we will be watching closely.

By Larry Benedict, Founder, The Opportunistic Trader

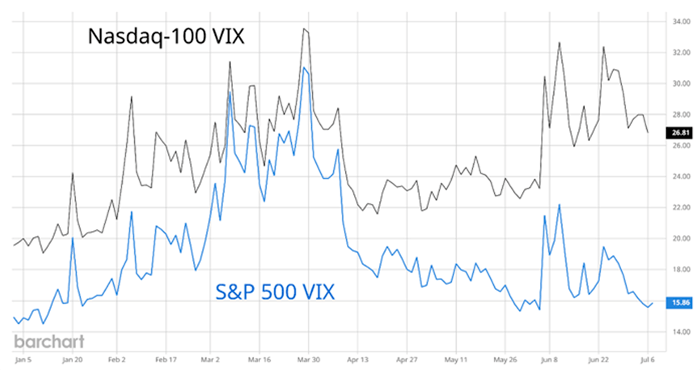

One of the more intriguing aspects of the market right now is how little volatility we’re seeing in the S&P 500 despite growing risks.

The CBOE Volatility Index (VIX), which reports expected volatility in the S&P, has recently been tracking at the 15-16 level. Some call it Wall Street’s “fear gauge” because the VIX usually jumps higher when the S&P 500 pulls back. Conversely, the VIX tends to be the lowest when stock prices are steadily grinding higher.

In comparison, the Nasdaq-100 has its own measure of expected volatility. As you can imagine, volatility trends across the S&P 500 and Nasdaq-100 tend to mimic each other. But lately, a divergence is opening up. Take a look at the chart below that plots implied volatility across both indexes.

Volatility measures across the S&P and Nasdaq tracked closely to start the year. But starting in April, Nasdaq volatility started trending higher.

Even though the Nasdaq-100 has rallied toward record highs, implied volatility is now trading at the same level as in late March, back when the Nasdaq fell into a correction. That shows a major disconnect between the price action in the Nasdaq and volatility expectations.

It also raises the question of why the S&P’s VIX is so low. To me, that level of complacency is difficult to reconcile with the broader macroeconomic outlook. Investors seem convinced that the biggest challenges are now behind us.

But geopolitical tensions in the Middle East remain unresolved. While the Iran war may have faded from being a front-page story, those risks haven’t disappeared. Energy markets, shipping routes, and the global supply chain remain vulnerable. It’s hard to have great confidence that any peace deal will last over the long term.

Closer to home, the Federal Reserve under Kevin Warsh has adopted a noticeably more hawkish stance on inflation. A growing number of Fed officials think a rate hike could be in the cards if inflation concerns persist.

That’s being reflected in bond yields. Ten-year Treasury yields have climbed back to the 4.5% level, suggesting that investors increasingly expect rates to stay higher for longer. Clearly, a rate cut is off the table for now.

That has implications for equity valuations that are already overstretched – in particular, the valuations of stocks priced for exponentially high growth. The major indexes are increasingly carried by just a handful of these stocks. When a market’s leadership becomes overconcentrated, it leaves us vulnerable to a sell-off if sentiment suddenly changes.

The market may be underestimating the potential for volatility in the second half of this year. The good news is that that’s the exact type of environment where we can start generating serious income.

Read the latest insights from the world of high technology.

Sometimes the smallest forces, the ones almost nobody notices, end up making the biggest difference. Investing works much...

AI has been the dominant force in this market for the last three years. It started with semiconductors. Then...