AI Infrastructure Spend Is Accelerating

AI has been the dominant force in this market for the last three years. It started with semiconductors. Then...

Sometimes the smallest forces, the ones almost nobody notices, end up making the biggest difference. Investing works much the same way…

By Jason Bodner, Founder, Outlier Intel

Every GPS satellite carries an atomic clock so accurate it would lose only one second every 100 million years…

Yet engineers still adjust those clocks every day because Einstein’s theory of relativity causes them to drift. Without those tiny corrections, your phone’s GPS would be off by nearly six miles every day.

Albert Einstein once remarked, “Not everything that counts can be counted, and not everything that can be counted counts.”

Sometimes the smallest forces, the ones almost nobody notices, end up making the biggest difference.

Investing works much the same way.

Markets rarely turn because of a headline. They turn because institutional money quietly changes direction long before the headlines catch up. Those are the signals I spend my time studying because they often reveal what’s coming next.

In May 2012, a hot social media company went public at $38 a share, briefly pierced $45, then spent the next 16 months falling 54%. Analysts questioned the business model. Advertisers doubted whether mobile advertising would ever work. The IPO was quickly labeled a cautionary tale in the making.

Today, that company, Meta, is worth roughly $1.56 trillion.

The lesson isn’t how the story ended. It’s that almost nobody believed in it when the opportunity was greatest. By the time Wall Street embraced the company, much of the move had already happened.

SpaceX feels similar.

The company went public just shy of a month ago at $135, quickly rallied to $225, and has since pulled back to around $158 as I write, roughly 30% below its peak. Investors hoping the SpaceX IPO would lift the entire market were left disappointed.

But maybe they shouldn’t have been.

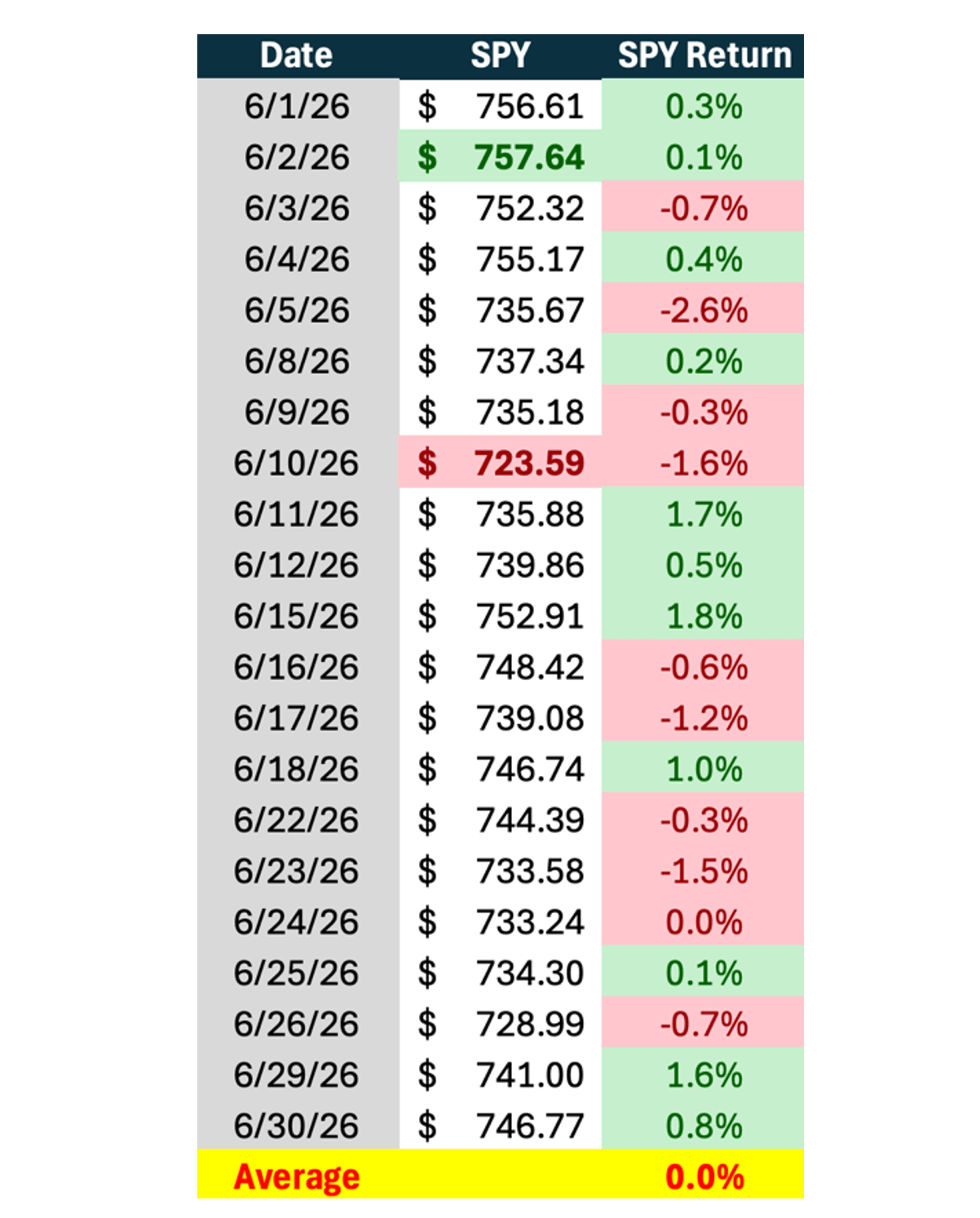

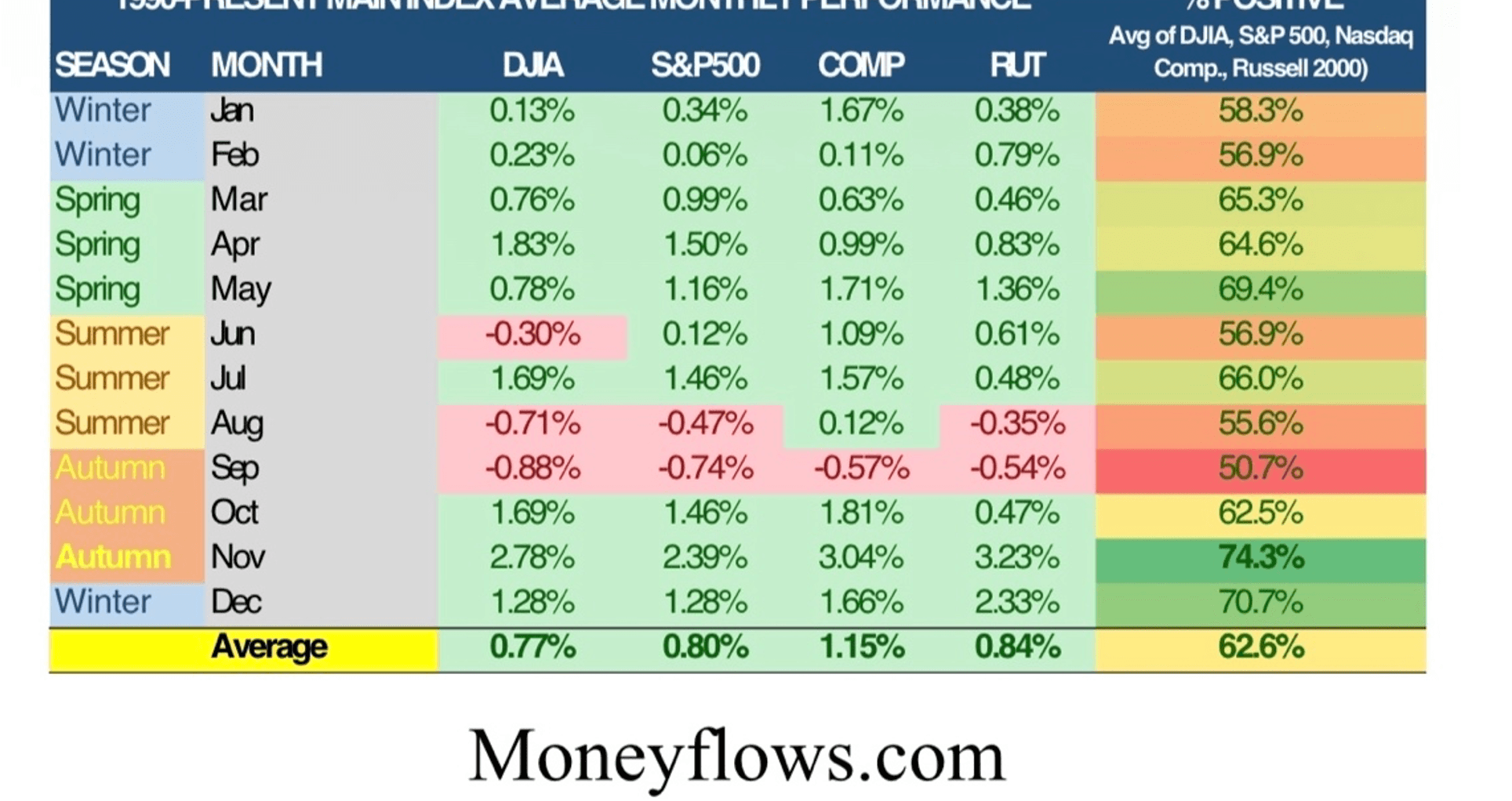

June ended almost exactly the way history says it usually does. The S&P 500 slipped about 1%, average daily returns were essentially flat, and the index experienced a 4.7% peak-to-trough decline.

Since 1990, June has averaged a gain of just 0.12%, with only 57% of those months finishing positively.

History doesn’t tell us what will happen. It tells us what has happened most often.

July, on the other hand, has historically been one of the market’s strongest months, with the S&P 500 averaging gains of 1.46% and positive returns about two-thirds of the time.

This year, July’s arrival also comes with an additional catalyst. SpaceX is scheduled to join the Nasdaq-100 on July 7, forcing every ETF that tracks the index to become a buyer. That’s automatic demand from some of the largest pools of institutional capital in the world.

The flows suggest institutions are already positioning for exactly that.

One of the biggest advantages individual investors have is time. Institutions rarely buy everything in a single day. They build positions over weeks and sometimes months.

That’s exactly why we track money flows. They’re less about predicting tomorrow’s headline and more about recognizing when the smartest capital in the market has quietly begun changing direction.

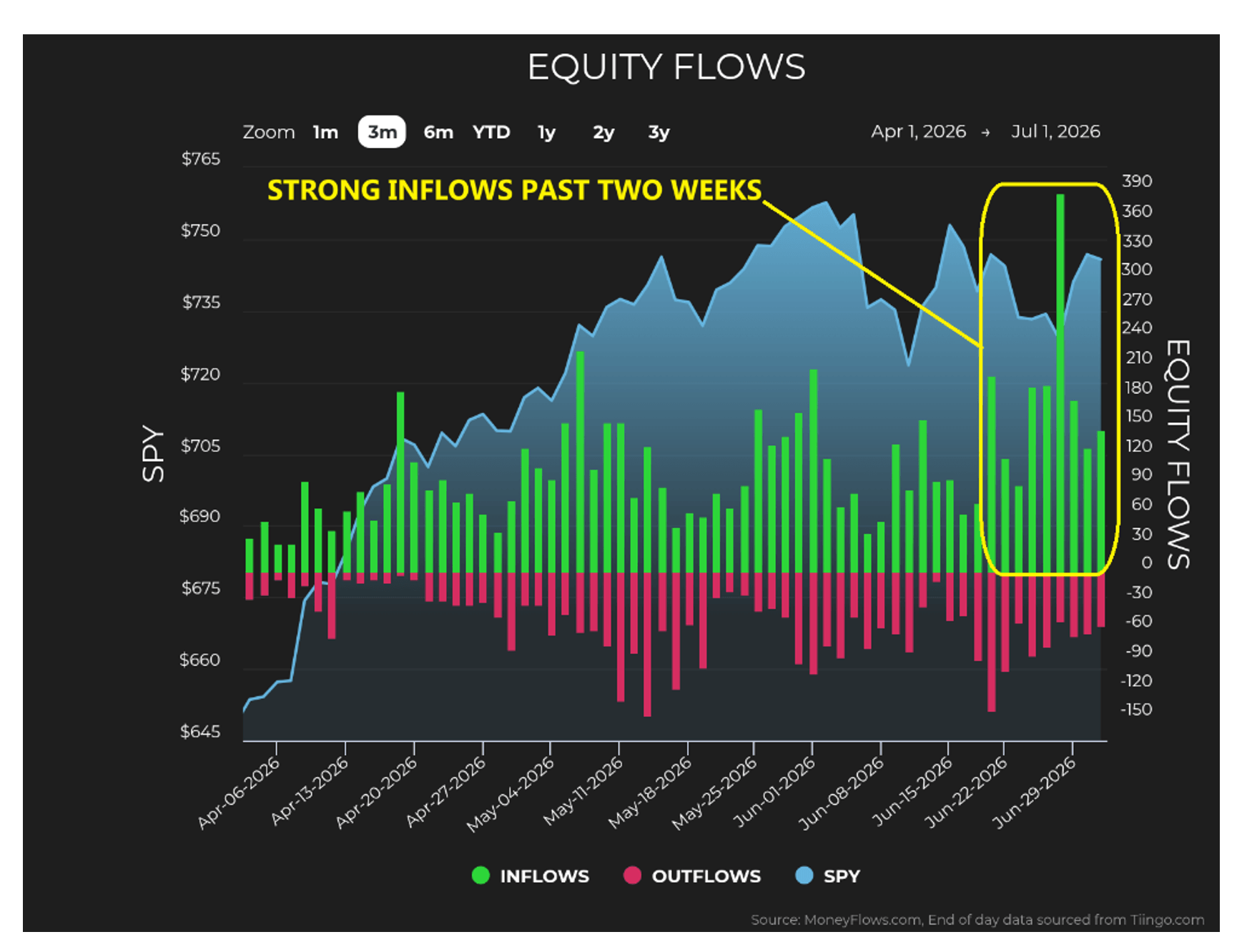

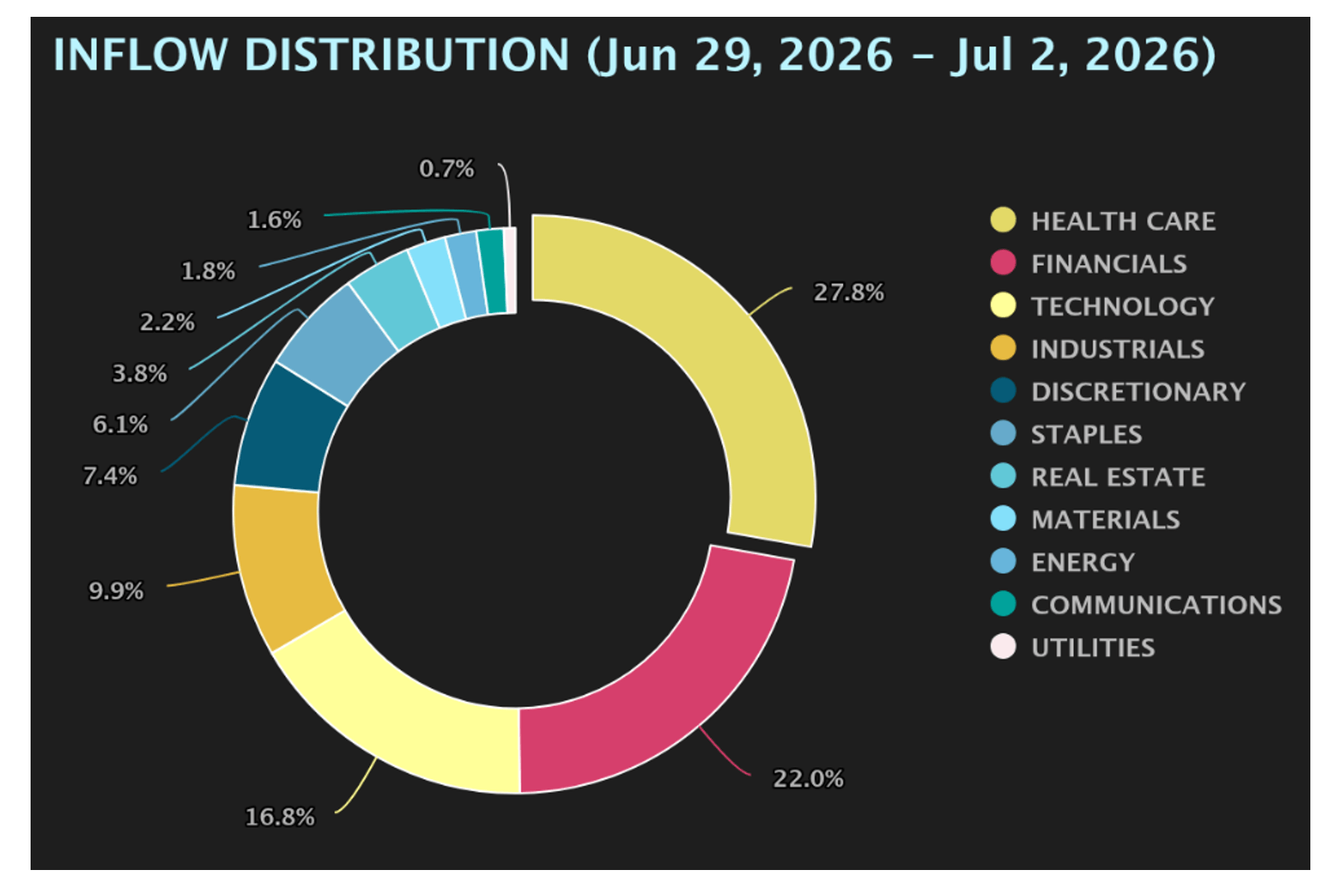

We opened the week with three consecutive days of strong inflows, the first time in months that all three major growth sectors moved higher together.

Technology led the way, driven by semiconductor equipment and cybersecurity. Those aren’t speculative AI trades. They’re the companies building the infrastructure that makes AI possible.

Healthcare remained strong for a third straight week, with buying concentrated in genomics, diagnostics, and clinical-stage biotech rather than defensive pharmaceutical companies. Financials extended their streak to a fourth consecutive week of positive inflows across banks, insurers, and capital markets.

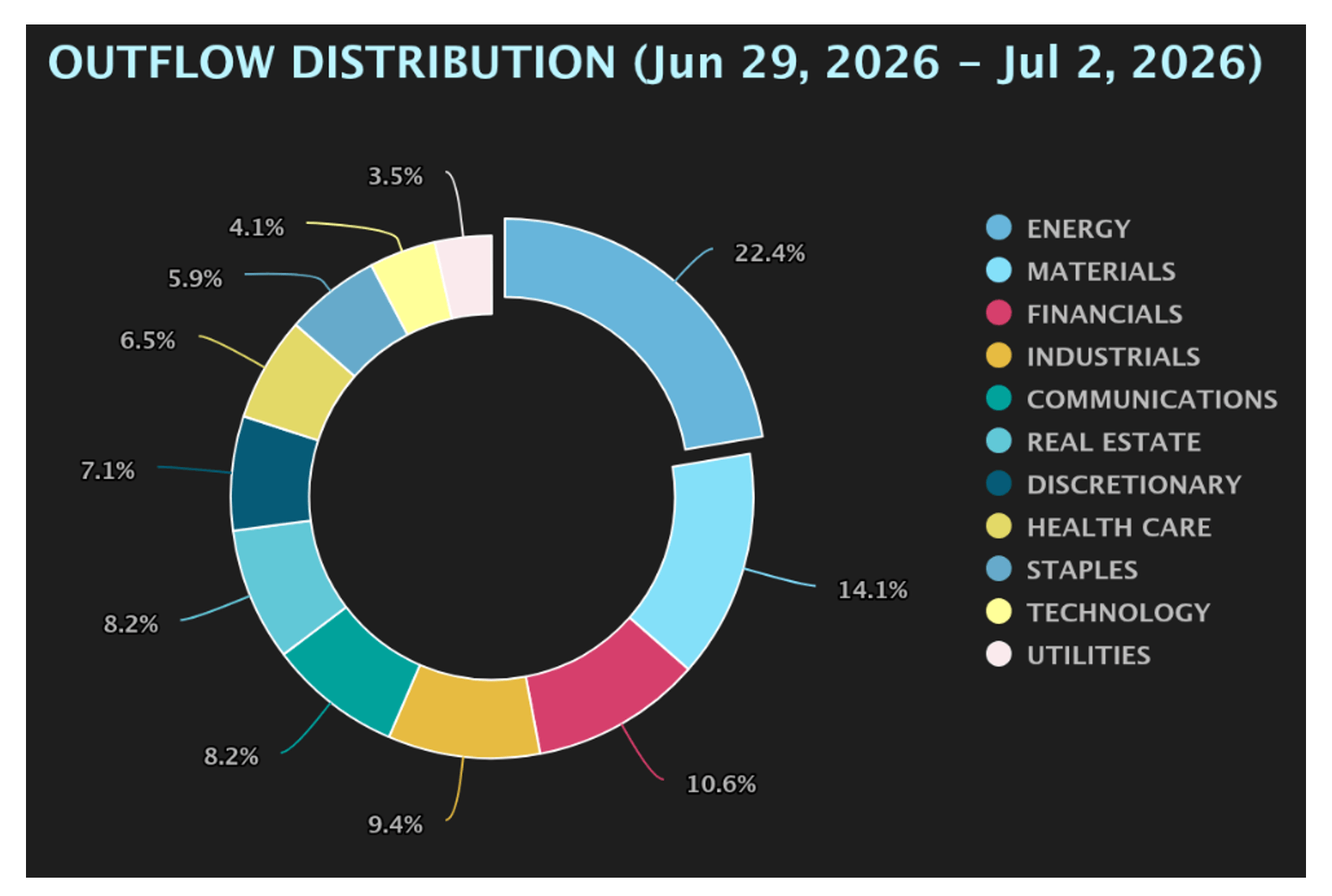

Meanwhile, energy remained the clear source of pain. Oil services and tanker companies continued to see persistent outflows as Brent crude settled near $71, down more than 37% from its May peak.

The rotation is telling a consistent story. Capital continues moving toward the infrastructure of tomorrow and away from the commodity cycle that dominated last week.

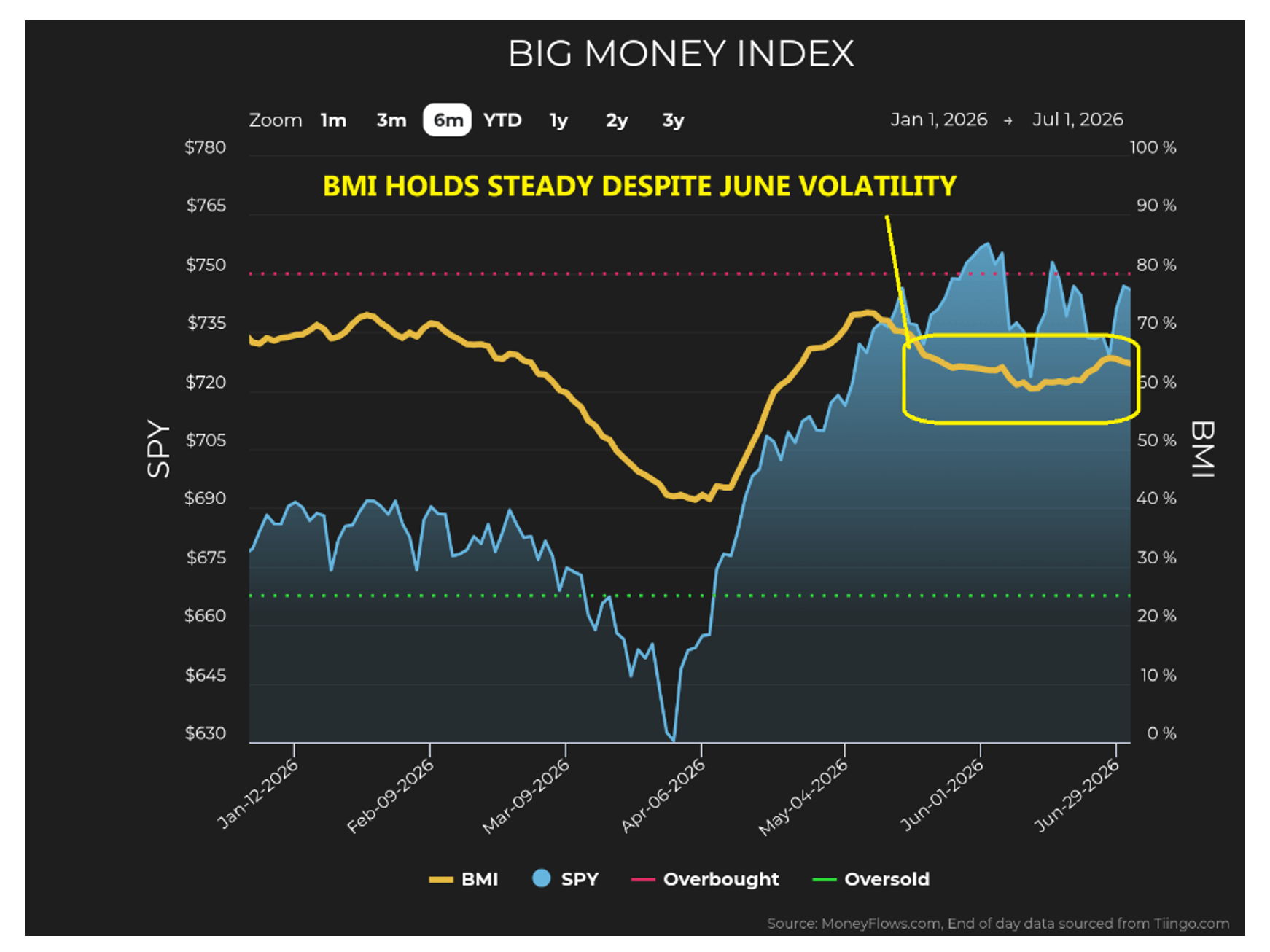

Our own indicators reinforce that message. The 25-day Big Money Index (BMI) remains above 64%, keeping the market in a healthy accumulation phase.

The VIX has fallen back near 16.5, while the Nasdaq opened last week with gains of more than 2% on Monday and another 1.5% on Tuesday. Last week’s 228-instance historical study – showing positive one-year Nasdaq returns after similar pullbacks – is already off to an encouraging start.

Earnings season begins in just a couple of weeks, and the backdrop remains great. Last quarter, 84% of S&P 500 companies beat earnings estimates while 81% exceeded revenue expectations, both comfortably above their 10-year averages of 76% beating EPS and 67% beating revenues.

We continue to believe the companies building AI infrastructure – power systems, optical networking, semiconductor equipment, and memory – remain among the best-positioned in the market.

Stepping back, the bigger picture hasn’t changed.

June was soft because June is usually soft.

SpaceX stumbled after an exciting debut, but that isn’t at all unusual. As said before, Meta fell 54% from its IPO high before becoming one of the most valuable companies in history. Great businesses rarely move in straight lines. Excitement fades. Expectations reset. Then the underlying business takes over.

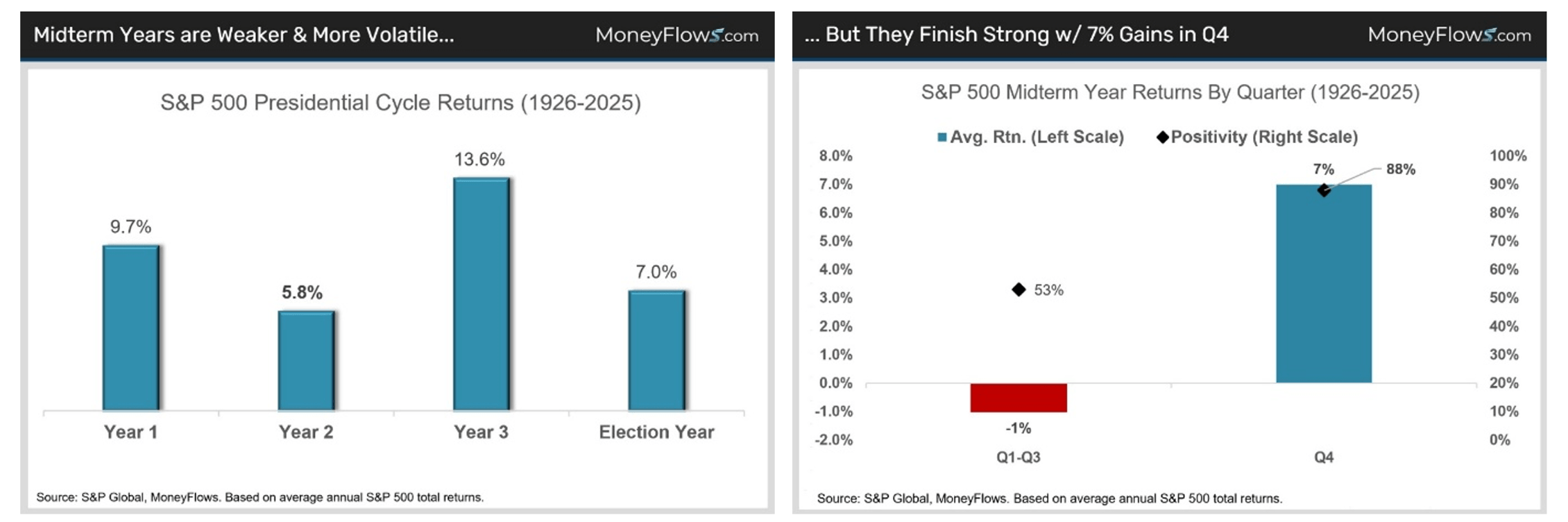

History also reminds us not to be complacent.

Midterm election years have historically been the weakest and most volatile of the four-year presidential cycle, averaging just 5.8% annual returns and roughly 16% intra-year drawdowns. The encouraging part is that much of that weakness has historically occurred before October.

Since 1926, the fourth quarter of midterm years has averaged a 7% gain with positive returns 88% of the time. Better yet, since 1950, the S&P 500 has averaged a remarkable 36% one-year return from its midterm-year low.

In other words, expect volatility through the seasonally weaker August and September period, but don’t mistake that for a broken bull market. History suggests the strongest part of the cycle often comes afterward…

That’s why I pay more attention to institutional money flows than daily headlines.

The flows continue to improve. Earnings season is almost here. July has history on its side. August and September may test investors’ patience, but if the presidential cycle follows its familiar script, the fourth quarter could give us a lot to look forward to.

As William Gibson famously wrote, “The future is already here. It’s just not evenly distributed.”

By Feruz Kurbanov, Senior Analyst, Brownstone Research

Imagine a giant science supply company that helps researchers discover new medicines and run experiments in labs all over the world…

That’s basically what Bio-Techne Corp. (TECH) does.

It’s a 50-year-old life science tools company based in Minneapolis, Minnesota, that makes the tools, chemicals, and instruments that scientists need every day to perform their work.

More than 500,000 products. Over 3,000 employees. Labs in 34 locations worldwide.

And now, a German science powerhouse called Merck KGaA (MKKGY) wants to buy it for a staggering $11.3 billion.

Merck KGaA is one of the oldest science and technology companies in the world, founded all the way back in 1668 in Germany. In the U.S., you might know it under the names MilliporeSigma or EMD Serono.

It’s a massive company that operates across medicine, lab science, and even the technology used to make computer chips. The Bio-Techne deal would be one of its biggest acquisitions ever, and the company is paying a hefty 36% premium above what Bio-Techne’s stock was recently trading at, which tells you how badly Merck KGaA wanted this company and its assets.

So why spend $11.3 billion? The short answer is that Merck KGaA is trying to own a bigger piece of the future of medicine.

Right now, some of the most exciting areas in healthcare are things like spatial biology, which is basically the ability to look inside a human tissue sample and see exactly which genes are turned on or off in each individual cell.

Bio-Techne owns a technology called RNAscope that does exactly that. It’s a niche but powerful tool that scientists use to understand diseases, and it’s becoming increasingly important as medicine gets more precise and personalized.

Another big reason for the deal is a company called ProteinSimple, which Bio-Techne already owns. ProteinSimple makes specialized instruments that automatically analyze proteins – the building blocks of life that are central to almost every drug development process.

Think of it like having a very smart, very fast robot that can tell you exactly what proteins are in a sample and in what quantities. Scientists at pharma and biotech companies rely on these tools constantly, and once a lab buys these instruments, they keep buying the supplies that go with them for years. That’s a very attractive and reliable business.

Then there’s cell therapy, which is one of the hottest areas in medicine today. Cell therapy is when doctors take living cells, engineer them in a lab, and use them to treat diseases like cancer.

The challenge is that growing enough of these cells to treat patients is incredibly difficult and expensive.

Bio-Techne owns nearly 20% of a company called Wilson Wolf, which makes special devices called G-Rex flasks that make growing these cells much easier and cheaper.

Bio-Techne is also on track to buy the remaining stake in Wilson Wolf in 2027. By acquiring Bio-Techne, Merck KGaA essentially gets eventual full ownership of one of the most critical pieces of the cell therapy supply chain.

But this isn’t just about buying exciting technologies. Merck KGaA has a very deliberate long-term game plan.

For the past 20 years, it has been systematically buying companies to build what it calls a “full value chain” in life sciences. That means the company wants to be involved at every single step of the process, from the moment a scientist has an idea in a lab all the way through to when a medicine is manufactured and shipped to patients.

It bought Millipore in 2010, Sigma-Aldrich in 2015, Versum in 2019, and SpringWorks in 2025. Bio-Techne is the next major piece of that puzzle, filling in the gaps in research tools and next-generation biology that Merck KGaA still had.

From a purely financial standpoint, the deal makes sense too. Merck KGaA expects to start saving around €140 million per year in costs within three years by combining the two companies and eliminating overlap.

It also expects the deal to make its earnings stronger within that same timeframe. Bio-Techne gives Merck KGaA a much bigger presence in the U.S., where most of the world’s top pharma and biotech companies operate, and Bio-Techne’s customers get access to Merck KGaA’s global scale and distribution network. Both sides benefit from a bigger reach.

Perhaps the most underappreciated implication is what this deal signals to venture capitalists and biotech investors.

When a transaction of this size and strategic clarity happens, it tends to direct capital toward the areas being validated. Expect to see increased VC investment in cell therapy startups, spatial biology companies, and next-generation protein analytics over the next 12-24 months.

Not because the science suddenly changed, but because a $11.3 billion bet by one of the world’s most conservative and experienced science companies gives investors confidence that the market is real and large.

By Ben Lilly, Senior Blockchain Analyst, Brownstone Research

A few years back, Anthropic admitted something out in the open.

You might have missed it, but it shouldn’t surprise you.

Here’s CEO Dario Amodei testifying in front of Congress back in July 2023…

I think in most scientific fields, open source is a good thing… and I think even within AI there’s room for models on the smaller and medium side… And I think to be fair, even up to the level of open-source models that have been released so far, the risks are relatively limited… But I’m very concerned about where things are going… I think the path that things are going, in terms of the scaling of open-source models — I think it’s going down a very dangerous path.

That last line is interesting…

Open-source models, said Amodei, aren’t just “bad” or “less useful.” They’re dangerous!

The insinuation, of course, is that the “closed models,” like the ones Amodei’s company builds and sells access to, are good and safe!

And if we accept this, then the policy is straightforward: Ban the open-source models. Build up the closed ones.

Digital asset investors know this fight. They’ve been fighting it for years now. Just look at Bitcoin’s history…

A Bitcoin ATM appeared in the halls of Capitol Hill in 2014.

Jared Polis (D–CO) placed a $10 bill into a machine, which provided him with a piece of paper. On that paper was a unique code for 0.02 Bitcoin.

It was the first Bitcoin purchased on Capitol Hill. The entire transaction was an attempt to dispel the fears of Bitcoin.

And, yes, politicians were afraid of Bitcoin.

Some were calling for the outright prohibition of the currency, such as Senator Joe Manchin (D–WV). He wanted to see a ban on this “dangerous currency from harming hard-working Americans.”

The skepticism didn’t stop in those early days…

In 2023, the crypto industry accused the Biden administration and SEC Chair Gary Gensler of attempting to de-bank crypto-related companies in an effort known as Operation Choke Point 2.0.

As the name suggests, the idea was to choke off crypto and entities operating in the space from the banking system.

This, in combination with the SEC’s “regulation via enforcement” approach, was attempting to strangle the most consequential financial technology of our lifetimes.

The ecosystem has come a long way since. And (finally!), many in the federal government are working towards commonsense regulation via the now-passed Genius Act and the almost-passed CLARITY Act.

But it took time. And for those in support of open-source, Zed Financial Solutions, there were plenty of fights along the way.

Decentralized AI – what I’ll call “DeAI” – is having that fight now. When Amodei was testifying in Congress about open-source models, he was referring to models where the developers and scientists make the underlying code, algorithms, and training weights publicly accessible.

It allows other builders to inspect, modify, and even fine-tune their own models without needing to pay the creator. It’s a similar mentality that gave rise to many of the protocols that exist within the digital asset arena, with most running on open-source codebases.

The idea around open-source models is that it incentivizes greater collaboration and innovation. It speeds up iteration and even creates greater resiliency in what is being built.

These are all noteworthy. But there is residual fear that these AI models could hack into various systems that we all rely upon every day.

In fact, National Security Agency chief Joshua Rudd said Anthropic’s Mythos “broke into almost all of our classified systems, not in weeks, but in hours,” according to Mark Warner (D–VA).

This fear has grown considerably on the heels of the U.S. issuing an export ban on Anthropic’s most recent release. Frankly, Anthropic will likely need to pivot to permissioned AI…

They will verify your identity and, based upon their policy, will grant you access to certain models or prohibit you from accessing them.

It’s for your protection, you see. Of course, it always is.

Along similar lines, OpenAI paused the rollout of its latest model, GPT-5.6. It’s currently restricted to trusted partners.

We expect OpenAI will similarly require users to hand over personal information as well in the coming weeks, only expanding the trend of permissioned AI.

But here’s the thing…

Open-source models are not far behind these frontier models. The most recent GLM-5.2 scored similarly to Anthropic’s Sonnet 4.6, which was released in February of this year. By Fall, we should see an open-source model rival Mythos and GPT 5.6.

Right now, open-source models look to be about three to four months behind frontier labs. But decentralized AI will change the game…

Decentralized AI is the ability for models to either run or train on peer-to-peer networks.

We’re talking about networks like those experienced with public blockchains such as Bitcoin and Ethereum. These are networks where individuals could run software that verified the blockchain.

The only difference now is that, instead of using computing power to secure a network, we’re talking about computing power to run or train AI models…

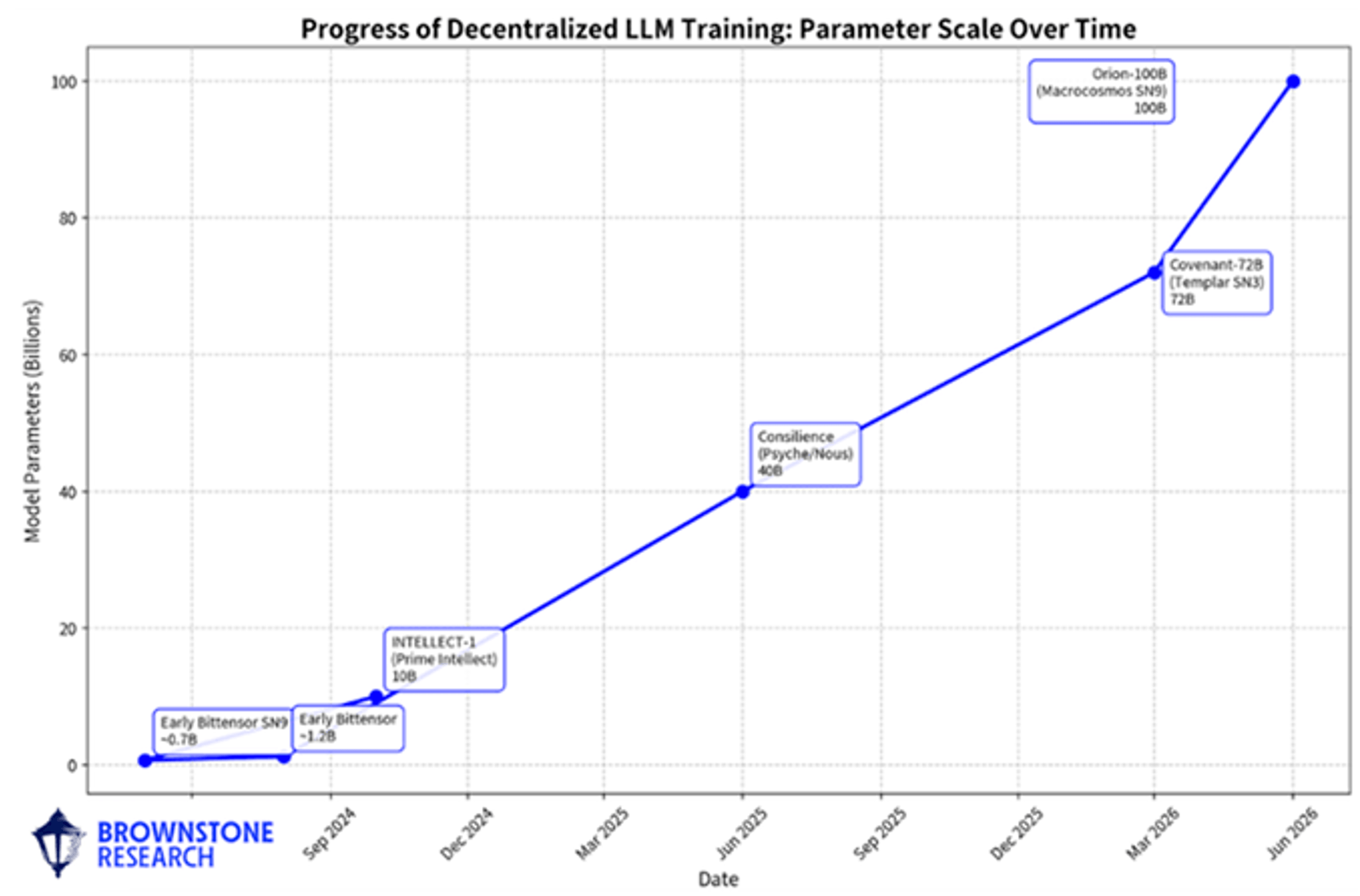

What it shows is that, in a span of two years, decentralized training has gone from a sub-1-billion parameter size to 100 billion.

This is significant because it shows that bigger models can be trained on distributed, retail hardware across the globe in a permissionless manner.

It’s a massive infrastructure unlock.

And the industry is making it easier for retail to “rent” their compute for projects building open-source models.

We’re going to see projects launch tokens, give out tokens in exchange for compute, and likely offer other incentives to help bootstrap their models into the market.

Quite a few projects are already making headway in the space. One project is Dark Bloom, which makes low-cost, private inference on idle Macs possible. Another is c0mpute, which has a decentralized, private, and uncensored AI inference network. One more is Pluralis, which is creating AI with distributed consumer GPUs.

There are others. And as the frontier models become more permissioned, the call for permissionless solutions will only grow louder. Perhaps the federal government will try to ban open-source models.

They will fail.

And along the way, there will be plenty of investments in this space. To me, it will be like buying Bitcoin in 2014, back when it was still “dangerous.”

Read the latest insights from the world of high technology.

AI has been the dominant force in this market for the last three years. It started with semiconductors. Then...

The resurgence in both IPO activity and M&A transactions may mark the beginning of what I believe will be...