When Stock Market Expectations Get Too High

To maintain those lofty valuations, companies can’t merely produce good results. They have to keep hitting it out of...

SpaceX’s IPO is not a warning sign. It is a signal that capital markets are wide open…

By Nick Rokke, Senior Analyst, Brownstone Research

Today’s the day…

It’s the moment many investors have been waiting for… SpaceX is expected to begin trading under the ticker SPCX.

This is no ordinary IPO. SpaceX is raising roughly $75 billion at an expected IPO price of $135 per share. That values the company at about $1.75 trillion.

That makes it the largest IPO in history. It’s more than double the size of Saudi Aramco’s record-setting offering in 2019.

That’s why I’ve heard the same question over the past month… Will the SpaceX IPO mark the top?

On the surface, the concern makes sense.

Investors worry that an IPO this large will absorb capital that would otherwise flow into existing stocks. If too much money gets diverted into new issuance, the thinking goes, the broader market could struggle.

But history tells us that isn’t how this works.

Companies don’t choose to raise capital when markets are weak. They raise money when demand is strong and when investors are willing to pay premium prices. Management teams know they can sell into strength.

And we need to keep the numbers in perspective. Yes, $75 billion is a massive raise. But relative to the roughly $71 trillion market capitalization of the S&P 500, it represents about 0.1% of the total market cap.

That is not enough to drain liquidity from the market.

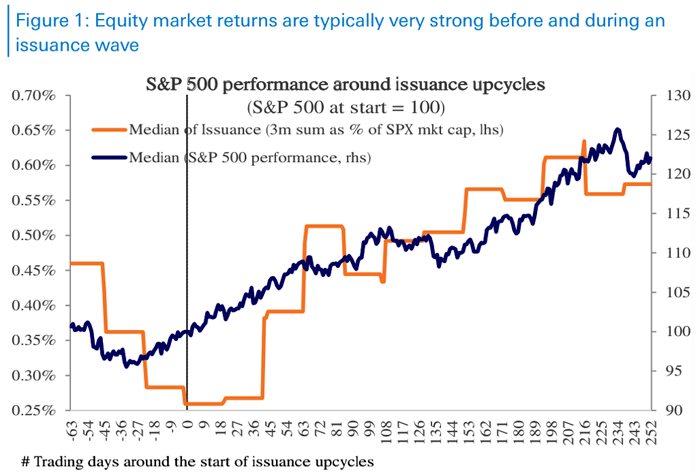

Deutsche Bank’s research team recently looked at major equity issuance waves over the past 30 years. The results were clear. The market has typically remained strong during and after these periods of heavy issuance.

The chart below shows that as the amount of issuance increases (orange line), the market rises (blue line). And it tracks it over many cycles with the beginning of the cycle at the vertical black line. The results go out 252 trading days, which is one calendar year.

Source: Bloomberg Finance LP, Dealogic, Deutsche Bank Asset Allocation

Their data showed that following a major pickup in issuance, the median equity return was roughly 8% over the next three months… and about 20% over the following 12 months.

Now, that doesn’t mean we should expect the market to go straight up.

We’re still seeing volatility tied to the escalation in Iran and renewed concerns over inflation. Those headlines can move markets in the short term.

But the demand for SpaceX shares tells us something important. As of Wednesday afternoon, the IPO was reportedly four times oversubscribed.

There is more than enough capital available to meet this issuance wave.

SpaceX’s IPO is not a warning sign. It is a signal that capital markets are wide open… investor appetite remains strong… and the biggest companies in the world are racing to fund the next phase of growth.

History says this kind of issuance doesn’t end bull markets. It usually confirms them.

By Larry Benedict, Founder, The Opportunistic Trader

“Higher for longer” may be back…

That was a hated phrase a few years ago. It entered investing consciousness after then-Fed-Chair Jerome Powell’s Jackson Hole speech in 2022.

Up until then, some were still holding out hope that the Fed’s rate-hiking regime—which took the federal funds rate from effectively zero in January 2022 to 2.33% at the time of the speech—would be short-lived.

After Powell’s speech in August 2022, that hope was over…

Here’s Powell at the time:

While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses. These are the unfortunate costs of reducing inflation. But a failure to restore price stability would mean far greater pain.

The market got the message. “Higher for longer” was born.

The Fed continued to hike its key rate, which eventually plateaued between 5.25% and 5.5% in August 2023.

From there, a decline.

The Fed’s current rate sits between 3.5% and 3.75%, about 32% below the recent peak. Until recently, the market was expecting rates to continue to trend lower, especially with new Fed Chair Kevin Warsh who is under intense pressure from President Trump to cut rates.

But then, last Friday happened…

The jobs report released on that day showed 172,000 jobs added to the U.S. economy. That was more than double the expected 80,000. Unemployment remained steady at 4.3%. Recent manufacturing and services data showed that both sectors are expanding as well.

A strong economy makes it more difficult for the Fed to justify cutting interest rates. If businesses are hiring, consumers are spending, and inflation remains well above target, then policymakers have little room to move.

That’s why Wednesday’s Consumer Price Index (CPI) inflation print matters so much.

On the one hand, CPI increased 4.2% year-over-year, the largest gain since April 2023. But excluding food and energy, the core CPI increased just 2.9%. And on a month-over-month basis, core CPI slowed down, gaining only 0.2% compared to April’s 0.4%.

But the move was enough to get the market thinking that “higher for longer” could be back.

As I write, investors are pricing in a 12.3% and 32.5% chance of a quarter-point hike at the Fed’s July and September meetings, respectively. Those odds spike to nearly 70% at the Fed’s December meeting.

That shift in expectations helps explain why Treasury yields have been rising. After stretching toward the 4.58% level, 10-year yields are hovering around the 4.52% level. That’s up from approximately 4.1% at the start of the year.

Treasury yields broadly reflect the market’s expectations around future interest rates, inflation, and economic growth. If investors become convinced that rates will remain higher for longer, yields typically rise.

For now, the bond market is telling us that yields will stay higher for longer. The economy remains resilient, and inflation risks aren’t going away.

All else equal, that could be a headwind for stocks. But it could also open plenty of opportunities for nimble traders who are paying attention.

By Ben Lilly, Senior Crypto Analyst, Brownstone Research

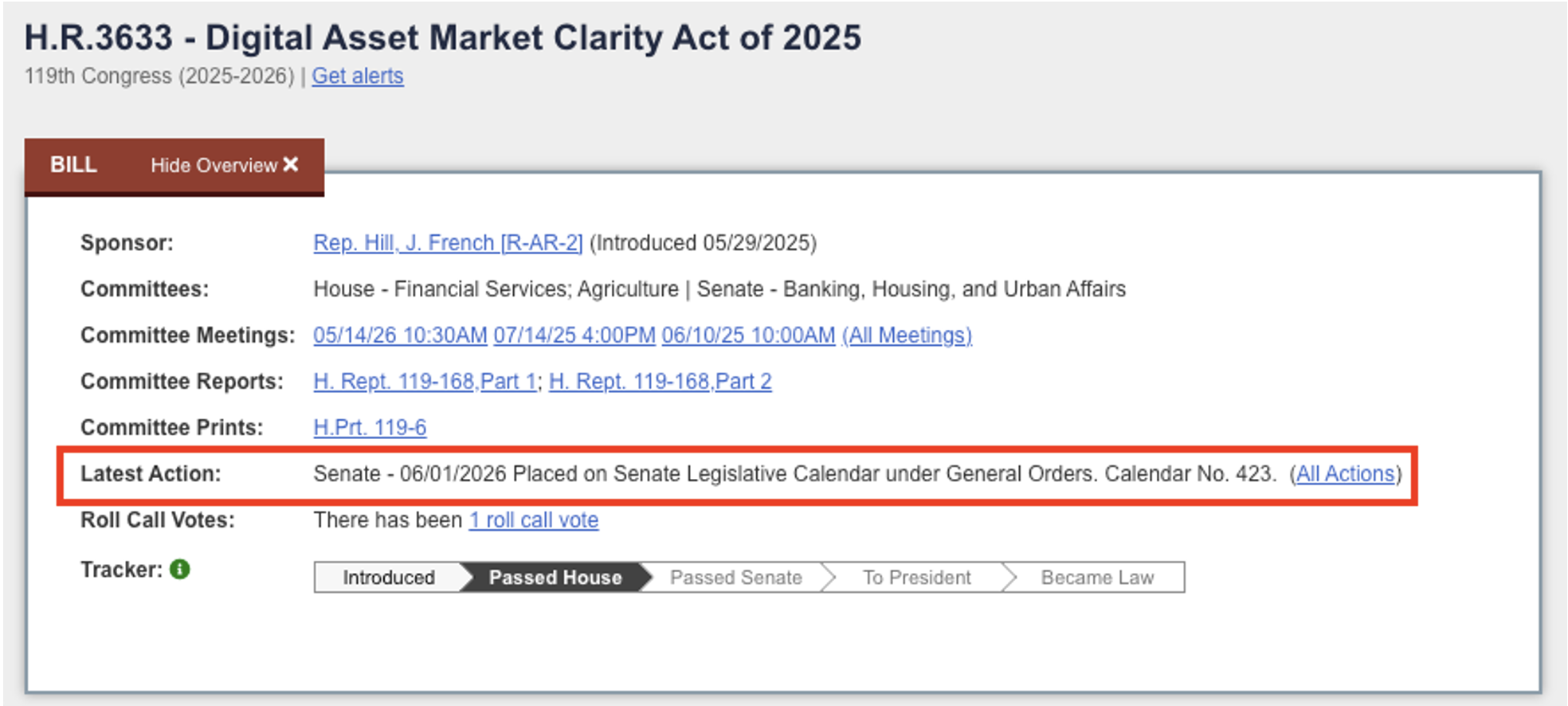

The Trump administration vowed to make America the crypto capital of the world. Later this month, the U.S. Senate will decide if that happens or not…

The latest news is that the CLARITY Act has been added to the U.S. Senate legislative calendar.

Source: congress.gov

The date has yet to be set, but the expectation is for the second half of June. This is the clearest timeline for completion we’ve gotten since the bill first passed through the House last summer. It’s also what we’ve heard from our contacts in Washington, D.C.

As a reminder, CLARITY is intended to offer a comprehensive regulatory framework for the entire digital asset industry in the United States.

What’s allowed and what’s not, what safeguards must be in place, which regulatory bodies oversee which assets—all of it will be spelled out in black and white.

This is something the industry has been clamoring for. For its entire history, digital assets have operated in a regulatory gray area. And even the most buttoned-up operators were forced to tiptoe around their own industry out of fear that an enforcement action from the Securities and Exchange Commission (SEC) would force them into legal purgatory and eventually run dry on funding.

CLARITY is meant to finally lay out the regulatory ground rules.

But between now and when the bill (hopefully) lands on the president’s desk, there are still a few obstacles…

Those close to the matter have outlined three areas needing resolution…

The first lies in the Senate Agriculture Committee, which has jurisdiction over the Commodity Futures Trading Commission (CFTC) and, therefore, commodities trading.

The issue here pertains to affiliated trading and conflict of interest rules. The administration is working directly with Senator Cory Booker (D-N.J.) to secure the bipartisan resolution.

We should expect this to be settled without much issue.

The second area that needs work is law enforcement, anti-money laundering, and national security.

This is where the Blockchain Regulatory Certainty Act (BRCA) provision of CLARITY is being hashed out. It’s the part of the bill that gives developers safe harbor, meaning just because you write code doesn’t mean you’re a money transmitter or criminal.

This has been a major point of contention over the years. But this too is likely to move forward without much issue, especially as the White House hosts many in law enforcement this week to assuage concerns.

Then there’s the third area that needs work.

Democrats are dug in, and not without reason, over the president’s involvement in some crypto-related projects.

Specifically, they’re singling out the president’s ties to World Liberty Financial. Without getting into the weeds, some of the recent actions from World Liberty Financial were questionable. And it raises the specter of inappropriate involvement in the industry for public officials.

In all likelihood, the administration will need to make some kind of concession here. There’s virtually no path through the Senate without one.

And time is of the essence.

That’s because the Senate is coming up against the looming August recess, and June has competing priorities, with the first two weeks of the month already booked with other legislative issues.

Once we get past August, midterms will suck the air out of the room. And pushing big legislation like the CLARITY Act will likely get tabled until the new year.

The crypto-watching world is keeping a close eye on CLARITY. That includes the team at Brownstone Research.

The path is far from clear. But if the remaining obstacles can be overcome, the digital asset industry will have something it’s been lacking for over a decade—a regulatory green light for sustainable growth.

Read the latest insights from the world of high technology.

To maintain those lofty valuations, companies can’t merely produce good results. They have to keep hitting it out of...

SMH fell 6.4% in the three days following the Kimi K3 release. Here’s why you shouldn’t worry…

This chart is a tried-and-true gauge of crypto’s risk appetite…