Don’t Panic Sell AI

This is the market giving us a chance to buy the leaders after a forced reset.

After months of stocks tracking higher, volatility was inevitable.

Managing Editor’s Note: This week, “Market Wizard” Larry Benedict – who once went 20 straight years without a single losing year – is revealing his strategy for how you can profit over and over again from the upcoming “IPO tsunami.”

All it takes is one simple, five-minute trade on IPO day. And you can target profits like $321, $1,605, or even $3,210, over and over again, all without buying a single stock.

He’s sharing all the details on Wednesday, July 15, at 8 p.m. ET. It’s free to attend; you just have to go here to sign up with one click to add your name to the guest list.

By Jason Bodner, Founder, Outlier Intel

Something strange happens when a ship’s propeller spins faster than the water around it can keep up.

Tiny bubbles form behind the propeller, then collapse almost instantly. The sound is so loud that you would swear something inside the engine is breaking.

It isn’t. The phenomenon is called cavitation. The engine is running perfectly. In fact, it’s working so hard that the water can’t keep up.

The solution isn’t to shut the engine down. It’s simply to ease back a little and let the water catch up.

That’s what this market feels like to me.

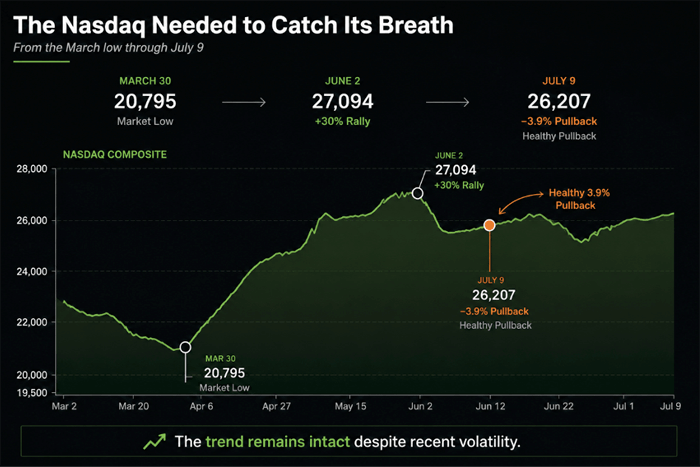

Three weeks ago, everything was working. The Nasdaq had rallied more than 30% off its March low. AI was all anyone wanted to talk about. That kind of enthusiasm was everywhere, in conversations, in comment sections, in the slow creep of overconfidence that always precedes a pause.

Then SpaceX went public, surged to $225, and for a brief moment, it felt like the perfect ending to one of the strongest rallies we’ve seen in years.

Markets don’t usually reverse because the story changes overnight. They reverse because the buying gets exhausted. Eventually, everyone who wanted to buy has already bought, and there aren’t enough new buyers left to keep pushing prices higher.

When SpaceX rolled over, many of the AI names followed.

The excitement that had been pulling new money into the market every day began to fade. Liquidity thinned out. Bid sizes got smaller. The algorithms noticed. Short sellers noticed. When buyers step back, someone always tests the market to see how much selling is left. Before long, a perfectly normal pullback starts feeding on itself. That’s exactly what happened.

What makes last week different from the headline story is what you can’t see in the indexes. The S&P 500 was roughly flat. The Nasdaq was modestly lower. Everything looked contained.

But underneath, a 33-point performance gap opened up between the names institutions were buying and the names they were selling. The April and May AI darlings – the names that led the sprint – averaged a loss of more than 10% over the past month. The names receiving institutional inflows over that same period averaged a gain of nearly 19%.

Same market. Same month. Completely different outcomes depending on which side of the flows you were on. That gap doesn’t show up in any index. It only shows up if you’re watching where the money actually went.

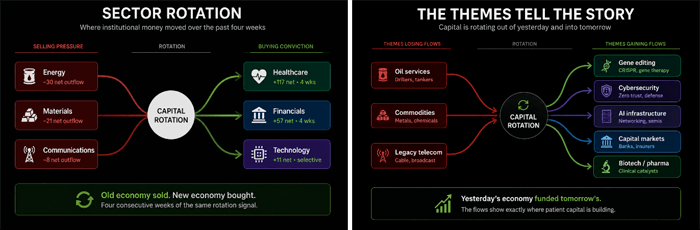

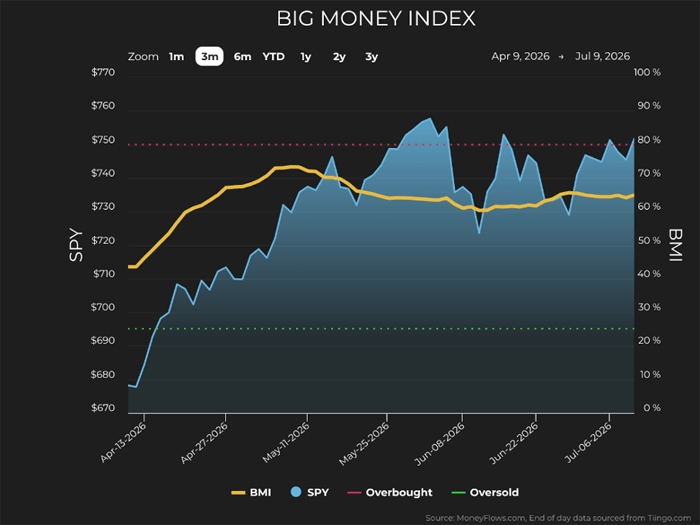

Moneyflows

The Big Money Index (BMI) held between 64% and 65% all week. The CBOE Volatility Index (VIX) fell to 15.8 – its lowest reading in over a month. That isn’t what a market falling apart looks like. It looks like money quietly changing seats.

Healthcare saw inflows for a fourth straight week, led almost entirely by gene therapy and gene editing companies. Healthcare inflow names averaged a gain of 28% over the past month, nearly 38 points better than the AI names being sold.

Financials posted a fourth consecutive week of buying. Within technology, cybersecurity and networking stocks continued attracting institutional money while the mega-cap names faded. The correction happened in prices, not in the market itself.

The healthcare flows especially caught my attention. Institutional investors don’t usually pile into the same niche of the market for four consecutive weeks without a reason. This wasn’t money hiding in defensive names. It was flowing into gene therapy and gene editing companies, two of the most innovative areas in medicine today.

CRISPR technology – first described by Jennifer Doudna and Emmanuelle Charpentier in 2012 – allows scientists to edit DNA with remarkable precision.

What sounded like science fiction just a decade ago is now becoming commercial reality across rare diseases, cancer treatments, and inherited genetic disorders. The direction is clear, and the pace is accelerating. When institutional investors quietly build positions in that theme week after week, it’s worth paying attention.

Cybersecurity tells a similar story. Every company rushing to adopt AI is also creating new security risks. AI doesn’t just create opportunities. It creates new ways for bad actors to attack businesses. As companies spend billions deploying AI, they’re also going to spend billions protecting it. Those companies aren’t grabbing headlines, but they’ve been showing up consistently in our flow data for weeks.

History also gives us perspective and an honest dose of caution.

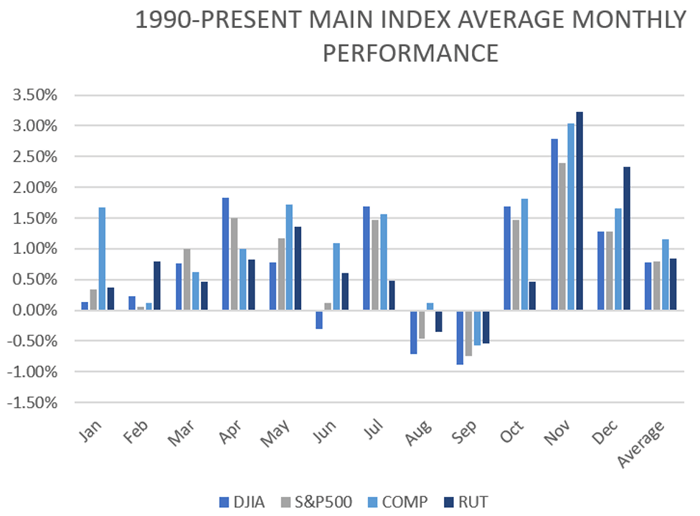

July has traditionally been one of the strongest months of the year, averaging gains of about 1.5% with positive returns roughly two-thirds of the time.

August and September are a different story.

Since 1990, August has been slightly negative on average, while September has been the weakest month on the calendar, averaging a loss of nearly 0.75%. During midterm election years, that seasonal softness has often been more pronounced, with the majority of the year’s volatility typically arriving before October.

But here’s the part most investors miss…

The fourth quarter of midterm years has been consistently strong, averaging 7% gains with an 88% positive rate since 1926. And since 1950, the S&P 500 has averaged a 36% one-year forward return off its midterm year lows.

The calendar has a way of rewarding patience.

Moneyflows

That doesn’t mean history always repeats. But even healthy bull markets pause. Pullbacks shake out the fast money, reset expectations, and create opportunities for investors willing to stay in their seats.

I think we are there today.

The excitement got ahead of itself. Prices corrected. Investors who bought out of fear of missing out decided they didn’t want to play anymore. It happens in every bull market.

What hasn’t changed are the long-term themes. AI infrastructure is still being built. Companies continue spending heavily on power, networking, cooling, and semiconductors. Gene editing is attracting institutional money. Cybersecurity remains one of the strongest areas of technology. Financials continue to see steady accumulation.

The loud money left. The patient money stayed.

As William Gibson once wrote, the future is already here. It’s just not evenly distributed. The headlines are still focused on yesterday’s winners and yesterday’s pullback. Meanwhile, institutional money is already positioning for what’s next.

Follow the flows.

By Jeff Brown, Editor, Brownstone Research

The biotechnology industry continues to gain momentum as two of the world’s largest pharmaceutical companies announced major acquisitions on the same day last week. The pace at which these M&A transactions are happening right now is impressive.

First, Novartis (NVS) announced last week that it will acquire British biotechnology company Myricx Bio in a deal worth up to $1.5 billion, including $1.1 billion paid upfront and as much as $400 million in future milestone payments. Myricx Bio’s acquisition gives the company access to a promising new antibody-drug conjugate (ADC) technology for cancer treatment.

On the same day, Vertex Pharmaceuticals (VRTX) announced that it will acquire Crinetics Pharmaceuticals (CRNX) in a deal worth approximately $10 billion…

That’s one of the largest biotechnology acquisitions of 2026.

The acquisition gives Vertex a commercial-stage rare disease company with an approved treatment for acromegaly, a rare hormonal disorder, along with several promising late-stage medicines that could reach the market over the next few years.

Together, these transactions send a clear message: large pharmaceutical companies are once again aggressively acquiring biotechnology innovation.

Although the two companies operate in different therapeutic areas, both acquisitions are driven by the same goal – building the next generation of blockbuster medicines.

Novartis is strengthening its leadership in oncology by acquiring a new ADC platform that could produce multiple future cancer therapies. Vertex, meanwhile, is expanding beyond its highly successful cystic fibrosis franchise by adding treatments for rare endocrine diseases.

Rather than relying on one or two successful products, both companies are investing today to ensure they have multiple growth engines for the next decade.

These acquisitions also highlight an important shift in how large pharmaceutical companies are making investment decisions. In recent years, many drugmakers have been cautious with acquisitions, preferring to wait for late-stage clinical data before committing billions of dollars.

Today, that strategy appears to be changing. Novartis was willing to pay more than $1 billion upfront for Myricx even though its technology is still in the preclinical stage, while Vertex paid a 100% premium for Crinetics because it already has an approved medicine and several advanced clinical programs.

In both cases, the companies decided it was better to secure valuable assets now rather than risk losing them to acquisitions by competitors later.

For biotechnology companies, these deals represent much more than individual acquisitions. They demonstrate that breakthrough science is once again commanding premium valuations.

During the biotech downturn, many innovative companies struggled to raise capital, biotech IPO activity slowed dramatically, and merger activity became much less frequent. Over the past several months, however, the environment has improved considerably. Along with recent acquisitions by AbbVie, GSK, Eli Lilly, Gilead Sciences, and others, the Novartis and Vertex transactions tell us that pharmaceutical companies are once again actively competing for the industry’s best technologies.

This renewed M&A activity has also restored confidence across the biotechnology capital markets.

Every acquisition returns capital to venture investors, institutional shareholders, and company founders. Much of that money is then reinvested into new biotechnology startups and small caps, helping finance the next generation of scientific discoveries.

At the same time, successful acquisitions encourage investors to support biotechnology IPOs and follow-on financings because they can once again see clear paths to value creation. Healthy acquisition activity and healthy capital markets reinforce one another, creating a positive cycle that benefits the entire industry.

Perhaps the most encouraging aspect of these transactions is that they span very different areas of biotechnology.

Novartis is investing in next-generation cancer technology, while Vertex is expanding into rare endocrine diseases. Earlier this year, other major acquisitions focused on autoimmune diseases, precision oncology, antibody-drug conjugates, and metabolic disorders.

This is a clear indication that pharmaceutical companies are not chasing a single trend. Instead, they are searching broadly for the most innovative science wherever it can be found. That is often one of the strongest signs that confidence has returned to the sector.

Taken together, these acquisitions strengthen the view that biotechnology has entered a new phase after several challenging years. Financing conditions are improving, IPO activity has begun to recover, and large pharmaceutical companies are once again deploying billions of dollars to acquire innovative businesses.

While no single acquisition guarantees a lasting recovery, the growing number of strategic deals suggests this is becoming a durable trend rather than a temporary rebound.

For investors, this may prove to be one of the most important developments in biotechnology today.

When industry leaders such as Novartis and Vertex begin spending billions of dollars to secure future innovation, they are signaling confidence in the long-term value of scientific breakthroughs.

History has shown that strong merger activity often marks the beginning of new investment cycles. If the current pace continues – and I am confident it will – 2026 may ultimately be remembered as the year biotechnology entered a new era…

One driven by accelerating innovation, improving capital markets, and renewed competition to own the next generation of breakthrough medicines.

By Nick Rokke, Senior Analyst, Brownstone Research

As I wrote last week, we’re seeing the market’s momentum leaders finally pulling back over the past couple of weeks. Frankly, after leading stocks higher for months, volatility was inevitable. And we’ve seen plenty of it over the last couple of weeks.

There have been big up days. Big down days. And sharp intraday swings across many of the same semiconductor names that led the market higher during the quarter.

That can feel unsettling. But we need to wait out the volatility in our AI infrastructure holdings.

What we saw late in June was not a breakdown in the artificial intelligence thesis. It was a Wall Street mechanical issue.

Many large funds rebalance at the end of each quarter. When a sector like semiconductors rises this much, this fast, those funds suddenly become overweight in the group. Their investment mandates and risk models force them to trim winners and buy underperformers.

That means selling the top performers… And the more the winners have risen, the more they have to sell.

It has nothing to do with demand, opportunity, or the businesses themselves.

It is forced selling that is caused by each institutional fund’s investment mandate, basically the rules that were established when they raised capital.

We believe that this is a temporary Wall Street quirk that will work itself out. The important point is that nothing has changed about the underlying trend.

The AI infrastructure buildout is not slowing down. If anything, it continues to accelerate. The companies supplying the chips, memory, networking, storage, power systems, and servers behind this buildout are still reporting elevated demand and expanding profits.

Recent earnings reports made that clear.

Nearly every major AI semiconductor company that reported this past quarter beat Wall Street expectations and raised forward guidance.

That is not what the end of a cycle looks like. That’s what happens when Wall Street is still underestimating the magnitude of the buildout.

The AI trade is far from over. In a true bubble, prices run far ahead of fundamentals. That’s not what we’re seeing here.

Just look at NVIDIA. Shares are up about 28% over the past year, yet NVIDIA’s forward EV/EBTIDA ratio has been basically cut in half.

The most important company in artificial intelligence has continued growing so quickly that its valuation multiple has compressed even as the stock moved higher.

That is not bubble behavior.

This is one of my favorite setups to see in the market. When stocks rise but get cheaper, it often means the price will go much higher than anyone thinks. We just have to hang on through the volatility.

We are not at the end of the AI infrastructure cycle. And we are nowhere close to dot-com-style bubble valuations.

Stay the course…

Read the latest insights from the world of high technology.

This is the market giving us a chance to buy the leaders after a forced reset.

The people who wanted out have sold. The hedgers already hold their downside insurance. And there is simply less...

Sometimes the smallest forces, the ones almost nobody notices, end up making the biggest difference. Investing works much...