AI’s Bitcoin Moment

We are now entering a world of permissioned AI use. And it’s fueling conversations around alternatives…

The battle between the digital asset industry and the bankers is a boxing match. And the long-awaited digital asset framework bill called CLARITY Act is the main event.

The remarks were revealing.

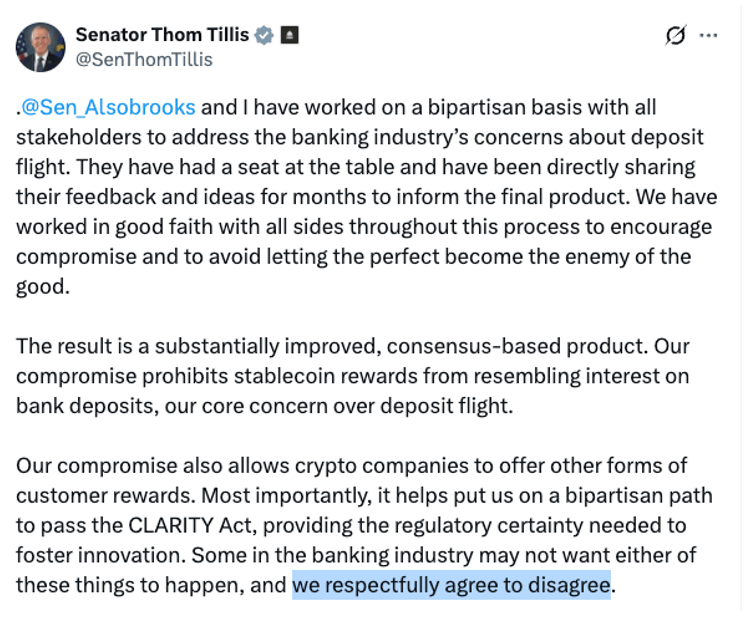

“We respectfully agree to disagree.”

This was a joint statement by Senators Thom Tillis (R-NC.) and Angela Alsobrooks (D-MD). It was directed at arguably one of the most powerful lobbying groups in Washington – Wall Street banking.

The statement was related to a topic readers might recall from April 27 in The Gloves Are Coming Off. In that essay, we said the battle between the digital asset industry and the bankers is a boxing match. And the long-awaited digital asset framework bill called CLARITY Act is the main event.

For some background, CLARITY Act is a bill that will give the digital asset industry regulatory clarity on how it can operate in the United States.

This includes a lot of nuanced items:

Regulatory uncertainty around these questions has caused many builders to withdraw their services and offerings from the United States.

And while the Securities and Exchange Commission (SEC) and Commodity Futures Trading Commission (CFTC) have been proactive in issuing guidance for the industry, the bill will codify their efforts. That would prevent future administrations from reversing it without congressional involvement.

It acts as a green light for Wall Street, blockchain developers, and investors. It would also be the starting gun for the administration’s Project Crypto initiative, which aims to move finance onchain.

And that’s why what happened on May 4 was so impactful—Tillis and Alsobrooks rang the bell.

Have a look below.

Source: X.com @SenThomTillis

The Senators were directing their comments to the banking lobbyists. Reading between the lines, it seems they see what I see. The real motivation of the banking lobbyists was never to find a compromise. It was to kick the can down the road and pray that the midterm elections deliver a more crypto-skeptic Congress.

The senators’ message was, in essence: You got your compromise. Now, we’re moving forward.

This was the biggest moment for CLARITY Act since it passed the House of Representatives on July 17, 2025, with a bipartisan vote of 294-134.

Since the passage in the House, the bill has been stuck in the Senate Banking Committee. And we finally have a markup being penciled in for the week of May 11. That’s next week.

That’s enough reason to be cautiously optimistic. But we’re also not naïve.

There are still some outstanding items that will be debated over the next week. And there is also a glaring issue that needs to be resolved.

Before we get to that major issue, let’s briefly touch on the minor concerns and what the compromise the senators describe entails.

Section 404 in the CLARITY Act is the portion of the bill that talks about paying interest or yield on stablecoins.

It’s a significant section since certain stablecoin solutions are currently paying interest via the assets that back those stablecoins. That would be U.S. Treasuries.

Short-term U.S. Treasuries have been paying around 3.7% yield this year. For comparison, Coinbase has been paying 3.5% on select USDC holdings on its exchange. Now Coinbase generates significant revenue on its relationship with USDC’s issuer, Circle, some of which likely comes from this difference in yield.

Regardless of whether the 0.2% is being earned by Coinbase or Circle, most would agree that’s fair. It’s certainly much better than what’s on offer at the banks.

The average yield paid on U.S. savings account is 0.58% according to Bankrate. Checking accounts are worse. This is why the banks are so worried about capital flight, and why they’ve been fighting tooth and nail to keep stablecoin yield out of Clarity.

The compromise in the bill will partially protect the regulatory moat that helps banks line their pockets. The section prohibits exchanges, brokers, or custodians from paying interest, yield, or rewards to U.S. customers for holding a payment stablecoin like USDC.

This sounds like it’s going to crush Coinbase’s bottom line. But here’s the fine print…

The compromise does not ban or restrict native onchain yield generated directly on public and permissionless blockchains.

Readers of Permissionless Investor have heard this more times than they can likely count… The future of finance sits on public and permissionless rails. Not on permissioned setups.

Section 404 is not just furthering this viewpoint but showcasing via regulatory setups where the industry is about to spend its time innovating.

That’s good news for onchain setups such as lending and borrowing protocol Morpho and the onchain swap exchange Aerodrome. These partners will become destinations for Coinbase users to earn yield.

Coinbase has been strengthening these partnerships in 2026. That’s likely because they knew, just as Permissionless Investor readers knew, onchain solutions will win.

That’s the direct impact of this compromise.

But the back and forth between the digital asset industry and legacy finance won’t stop with yield.

There are three areas we can expect to garner more attention in the coming weeks. One of them is Section 1960. This section acts as a safe harbor to developers of infrastructure. Put another way, developers would not necessarily be liable for how users interact with the tools.

It’s logical when you think about it.

Are automotive companies held liable—absent some manufacturing defect—for car crashes? Are boat manufacturers responsible for the illicit transport of goods on the seas?

Of course, not…

But at the end of the day, this technology is used to move funds easily, efficiently, and seamlessly. And just like traditional banks and even cash, some of those funds are bound to be illicit.

This is how you get the dishonest ‘crypto funds terrorists’ refrain.

I say “dishonest” because public blockchains are transparent and traceable. Moving funds on public blockchains is a good way for criminals to get caught. If anything, this should be more of a reason to protect developers. These tools could help catch illicit activity.

The second section that will generate attention is 505. This codifies tokenization of securities. It’s how more than $100 trillion in assets will move onchain. We can expect to hear folks who have regulatory moats in the legacy system go to battle over this. I named names in Freeing $100 Trillion in Assets.

Then, the last topic…

This topic isn’t new to readers of Chain of Thought. The president’s involvement in the digital asset industry is worth discussing. And it’s something that Democrats will dig their heels in as we approach markup.

Specifically, lawmakers will likely want to limit federal government officials from having business ties in crypto.

In most instances, that’s probably for the best…

In Trump’s Crypto Sideshow, we broke down the president’s involvement in crypto via World Liberty Financial. The whole ordeal is, at the very least, questionable.

Trump’s involvement is a subject that Democrats have rallied around. And they’re right to.

The Trump administration will likely need to make some sort of concession at the 11th hour to allow this bill to pass on the Senate floor.

Not all of these topics need to be finalized for the bill to move out of Committee and to the Senate floor. And it certainly won’t be smooth sailing.

But regulatory clarity is gaining momentum for the first time in nearly a year. In part, this is why the market has been so buoyant lately.

Over the last 30 days, Bitcoin is up 20%. ETH is up 15%. Smaller-cap tokens that are set to benefit from these developments have done even better.

Momentum begets momentum.

And if the stars align, then we’re in the early innings of the next great digital asset rally.

More to come…

Your Pulse on Crypto,

Ben Lilly

Editor, Chain of Thought

Read the latest insights from the world of high technology.

We are now entering a world of permissioned AI use. And it’s fueling conversations around alternatives…

Vitalik’s post on June 1 is worth taking seriously. It’ll likely lead to the next unicorn in DeFi.

I don’t know if we have any Anthropic executives reading this letter. But if so, I have a request.